Asia Frontier Capital (AFC) - December 2014 Newsletter |

|||||||||||||||||||||||||

In this IssueAFC Asia AFC Vietnam AFC Asia AFC Vietnam Fund

|

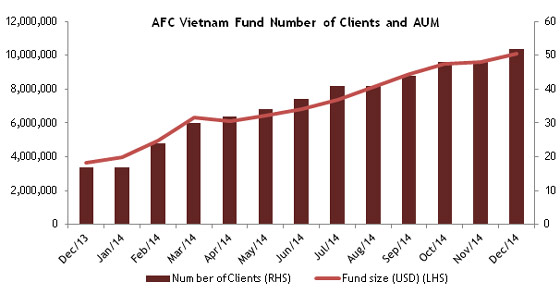

"Opportunity is missed by most people because In December 2014, the AFC Asia Frontier Fund returned –0.6% and the AFC Vietnam Fund returned +0.6%, bringing the 2014 annual return for our funds to +23.2% and +32.5% respectively. The MSCI Frontier Markets Index (-4.1 %), MSCI Emerging Markets Index (-3.6%) and MSCI World Index (-1.7%) all dropped this month while the MSCI Frontier Markets Asia Index (+2.6%) saw a bounce to recover from its -3.9% drop in November. The AFC Vietnam Fund has now passed its one year track record with another outperformance of both the Ho Chi Minh - VN Index (-3.7%) and Hanoi VH Index (-5.2%) in December. The AFC Asia Frontier Fund has now grown to USD 14 million AUM and the AFC Vietnam Fund has reached to USD 10 million. In USD terms, the AFC Asia Frontier Fund and AFC Vietnam Fund have now returned +38.0% and +35.6% respectively since inception in March 2012 and December 2013. For our Swiss investors, the CHF return for the funds since inception is +47.2% and +50.2%. If your base currency was EUR, the returns for the AFC Asia Frontier Fund since inception is similar to the CHF return, whilst the EUR share class launched in Jan 2014 returned +21.6% since then. The EUR based returns for the AFC Vietnam Fund stand at +52.8% since inception. December was certainly an eventful time for global markets, with oil prices continuing to be depressed and uncertainty around this issue causing volatility in global markets, with intra-month market drops of up to -10% before equally sharp recoveries. As mentioned in last month’s manager comment, the oil price has not had a large negative impact on AFC’s funds due to the diversified nature of our holdings, which are primarily non energy-related stocks. The low correlation between stock markets in our country universe also provides a natural buffer to global market volatility and our fund has historically outperformed during global market downturns. Additionally, within our universe some of our markets are net importers of oil and some of our markets are net exporters of oil. Net-net the markets that we invest in benefit overall from lower energy prices. Energy inputs and transportation costs have become lower for businesses and lower expenditures by individuals on oil-related products should boost the availability of disposable income and support domestic consumption in frontier markets. As our funds primarily invest in consumer, healthcare, industrial and material stocks, the AFC Asia Frontier Fund and AFC Vietnam Fund should continue to benefit from lower oil prices in 2015. In a slight departure from our usual format, this month’s newsletter will not include a country and travel report in favor of an annual overview of our markets and our fund performance in 2014. The annual reviews are found below the manager comments and will highlight some of the key events for our funds over the past year and provide some insights for our markets looking into 2015. AFC NewsAFC in the Media Upcoming AFC TravelIf you will be in any of the locations listed below and have an interest in meeting with our team, please contact our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager Comment

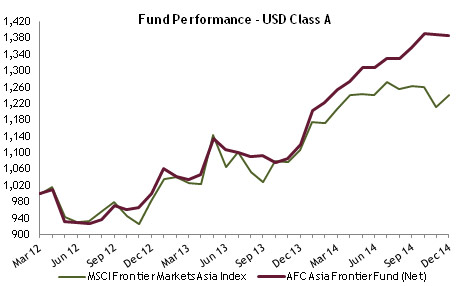

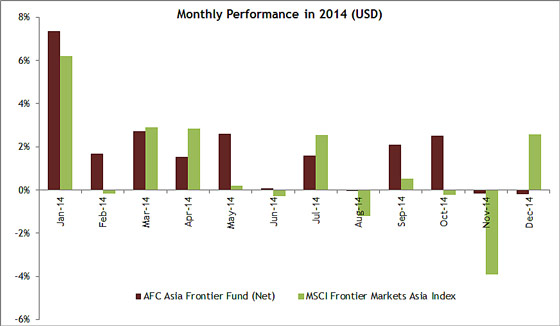

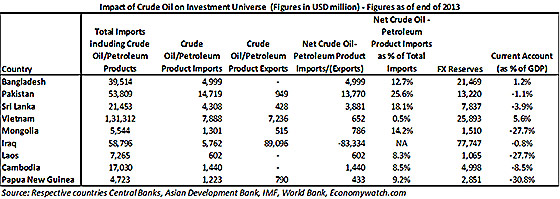

AFC Asia Frontier Fund (AAFF) USD A-shares returned -0.62% in December 2014, outperforming the MSCI Frontier Index (-4.1%) and MSCI World Index (-1.7%) while underperforming the MSCI Frontier Markets Asia Index (+2.6%). The fund ended flat for the month as some of the key markets saw a mixed picture. Though the markets in Bangladesh, Pakistan, and Sri Lanka all ended positive for the month, the fund’s return in these markets was impacted by corrections in top holdings within the respective countries. In Bangladesh, two of the fund’s larger holdings in the healthcare and consumer sector corrected between 3-10% while larger Bangladeshi index weights such as Grameen Phone and Lafarge Surma Cement, which the fund does not hold, rallied between 13-14%, leading to an underperformance for the month in Bangladesh. In Pakistan, similar to last month, a combination of textile and cement stocks provided positive returns, but this was negated by a correction in a healthcare, consumer staple, and energy company, all three of which are top holdings within Pakistan. In Sri Lanka, most of the fund’s consumer holdings did better than the market during the month, but performance was impacted by a correction in our largest Sri Lankan holding, an infrastructure company. We believe this correction was primarily due to the political uncertainty over this month’s Presidential elections, as infrastructure projects are awarded by governments and any possible future political changes often lead to uncertainty in such companies. The fund’s Vietnamese holdings did better than the Ho Chi Minh VN Index and Hanoi VH Index as a pipe company and the fund’s small cap holdings within the beer and industrial sectors did well. Furthermore, the fund does not own any energy stocks in Vietnam, which are heavily weighted in both the VN and VH indexes. With Brent Crude falling by another 19% in December, oil & gas stocks were amongst the biggest losers in Vietnam, which led to a steep correction once again for the Vietnamese market. Overall, it was a month in which we saw both positive and negative movements within our top holdings which led to a flat performance. Having said that, most of the larger holdings which saw a correction during the month have been amongst the top performers for the fund in 2014 and have substantially contributed to the outperformance of the relative benchmark. As mentioned in last month’s comment, lower crude prices are a significant benefit for a large part of our universe as countries such as Bangladesh, Pakistan, Sri Lanka, and Mongolia are net crude oil importers. Lower prices will not only lead to lower inflation but will also help these countries manage their current account deficits and relax pressure on foreign reserves, especially for Pakistan and Mongolia. With respect to Vietnam, which is a crude oil exporter but a refined petroleum product importer, the net impact on its current account should be neutral but consumers can benefit from lower inflation. With lower crude prices leading to lower inflation and petroleum prices in most markets, consumers and consumption-related stocks should benefit, and the fund is well positioned in this space, having a majority of its holdings within the consumer staple, consumer discretionary and healthcare sector. Lower inflation should also make monetary policy easier to manage for the central banks and therefore possible rate cuts in some markets could lead to further upside in interest rate sensitive sectors such as materials and industrial companies where the fund also has exposure. In December, we added to existing positions in Bangladesh, Cambodia, Iraq, Laos, Mongolia, Myanmar, Pakistan, Papua New Guinea, Sri Lanka and Vietnam. We sold the entire position of a Pakistani textile producer and partially sold one stock holding in Papua New Guinea. As of 31st December 2014, the portfolio was invested in 116 shares, 1 closed-end fund (with 21.0% discount to NAV), 1 GDR (with 62.9% discount), and held 9.7% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.3%) and a pharmaceutical company in Pakistan (3.6%). The countries with the largest asset allocation include Vietnam (22.8%), Pakistan (19.6%), and Bangladesh (13.1%). The sectors with the largest allocation of assets are consumer goods (40.7%) and materials (13.6%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 14.25 x, the weighted average P/B ratio was 1.65 x and the dividend yield was 4.15%. AFC Vietnam Fund - Manager Comment

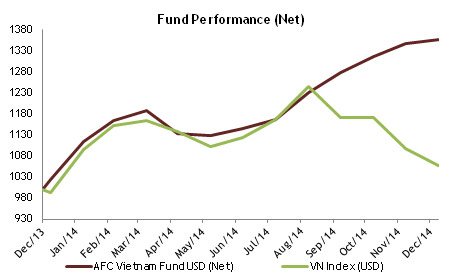

To read this month’s fund update in German please click here. In December 2014, the AFC Vietnam Fund returned +0.6%, bringing the total YTD return to +32.5%. Undeterred by the recovery of international stock markets - such as the USA, Europe and China - the Vietnamese market declined further without an obvious reason and finished the month with a loss of -3.7% in Ho Chi Minh and -5.1% in Hanoi. Nevertheless, we remain of the opinion that a turnaround of the market is imminent and we therefore started to add, for about 10% of our total portfolio, some heavily weighted index names. These latest additions were of course also affected by the recent sell off, but the overall portfolio performed well for a USD return of +35.6% since inception on 23rd December 2013. This represents a return since inception of +50.2% for CHF-based investors and +52.8% for EUR-based investors. The still relatively young AFC Vietnam Fund has been on an upward trajectory and the Vietnamese market has experienced a few excessive price movements, as one would expect from frontier markets. One of the reasons for this is that a handful of index shares are heavily influenced by foreigners due to capital inflows and outflows depending on the market situation. However, foreigners still only make up around 10% of the total volume in Vietnam, and on the Hanoi exchange the figure is well below 10%. Hence, the majority of the share trading volume is dominated by local investors which can often trigger erratic price movements as some participants are highly speculative. It is therefore not surprising to observe that in times of crisis or even when relatively small events occur, the stock market can fall or rise 10% to 20% in a very short time period. In December the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (5.1%) - a manufacturer of electrical and telecom equipment, Thuan An Wood Processing JSC (2.5%) – a household furniture manufacturer, FLC Group JSC (2.5%) – a real estate development company, SPM Corp (2.4%) – a pharmaceutical company and Foreign Trade Forwarding and Transport (2.2%) – a logistics company. As of 31st December 2014 the portfolio was invested in 71 shares and held 2.1% in cash. The sectors with the largest allocation of assets were consumer goods (35.0%) and industrials (22.6%). The fund’s weighted average trailing P/E ratio was 7.36x, the weighted average P/B ratio was 1.10x and the average dividend yield was 6.06%. AFC Asia Frontier Fund – 2014 Annual Review2014 Performance 2014 was a strong year for the AFC Asia Frontier Fund (AAFF) as a young team came together to establish a platform for future growth. This was not only reflected in the fund’s performance, but also in our focus on making on-the-ground visits to countries, meeting more companies, talking to people in our markets, and tracking developments in our investment universe on a pro-active basis. Strong fund performance comes from the right stock selection, but that would not be possible without the aforementioned points. Good performance during the year also saw an increase in our assets under management and we are committed to give our best for investors going forward. In terms of performance, AAFF returned +23.2% net of fees and outperformed our closest benchmark, the MSCI Frontier Markets Asia Index, which was up +12.2% in 2014. The MSCI Frontier Markets Asia Index consists of stocks from Bangladesh, Pakistan, Sri Lanka, and Vietnam, and we believe that this is our closest benchmark, as these four countries make up 68% of AFC’s fund as of December 2014 and historically these four countries have been a majority of the portfolio.

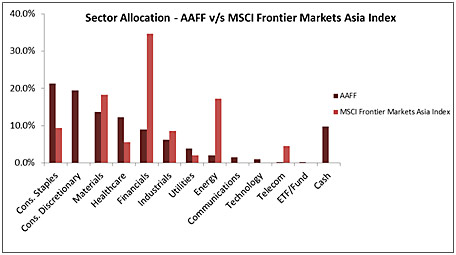

The other major index within the frontier markets space is the MSCI Frontier Markets Index, which was up 2.9% for the year and consists of global frontier countries, including the likes of Kuwait and Nigeria. This index lost a large part of its return in the last quarter of 2014 as Kuwait and Nigeria, both crude oil exporters, account for close to 40% of the index and both countries were negatively affected by slumping crude prices. Breaking down 2014 performance country wise, on a gross return basis, the leading return contributors within fund were Pakistan, Vietnam, Bangladesh, and Sri Lanka, in that order. The countries which were a drag on performance and had a negative return contribution were Mongolia, Iraq, Myanmar (Singapore listed plays on Myanmar), Papua New Guinea, and Cambodia in that order. The negative contributors did not have a very significant impact on fund performance, as the fund is not heavily concentrated in any one country which provides a balance when a few countries impact performance negatively. The reason that these countries were negative contributors is because most of these countries are dependent on commodity exports, which are being impacted by lower commodity prices. Iraq also had to contend with the additional challenge of the ISIS conflict which impacted the country’s economy. Our approach of diversifying our investments and not having a concentrated position in any one country reflects our top down approach to managing risk, which has proved successful thus far. The fund manages risk by diversifying assets across countries, but performance has purely been generated by stock selection. Within our top performing countries, it is specific stock ideas which led to outperformance of the respective markets. Elaborating further on this, the stocks which we overweighted for the fund are the ones which delivered positive performance and this reflects the point made earlier that it is stock selection that generated our strong returns in 2014. The top five return-generating stock ideas in 2014 were (in order of contribution to gross return): a pharmaceutical company from Pakistan, a consumer beverage company from Pakistan, a tobacco company from Pakistan, a pharmaceutical company from Bangladesh, and a consumer-focused conglomerate from Sri Lanka. All of these five companies were part of our top 20 holdings during the year except for the Pakistani tobacco company, which we exited and booked profit on in the beginning of 2Q2014. Not surprisingly, the stocks which did not perform well for the fund were energy/commodity related or were part of a country that was negatively impacted by lower commodity prices or certain events (i.e. Iraq). The bottom five return contributors (in order of contribution to gross return) were a consumer beverage company from Iraq, a Myanmar focused energy play listed in Singapore, a concrete company from Mongolia, an energy company from Pakistan, and a junior mining company focused on Mongolia. An observation which we would also like to bring up is that the best performing stocks in 2014 were from sectors which the fund is over weight on i.e. consumer staples, consumer discretionary, and healthcare. This ties in with our belief that the fund universe has favourable demographics in the form of a young population, rising GDP/capita, increasing literacy levels, and further country reform which will be beneficial for the populations of these countries and will have a positive impact on consumption. Another observation to discuss is the difference between the fund’s holdings and that of its closest benchmark, the MSCI Frontier Markets Asia Index. This index is primarily made up of large cap. names across the four markets of Bangladesh, Pakistan, Sri Lanka, and Vietnam. As mentioned earlier, the fund’s performance has been generated by stock selection as we are not benchmark-constrained, and this allows us to look at ideas which are not necessarily the large cap names for those respective countries but at the same time are well established companies, can provide longer term returns, and are fundamentally sound. A majority of the top performers for the fund in 2014 are not part of the relevant benchmark. The fund’s sector focus is significantly different from that of its benchmark, as the majority of the investments are made in the consumer staples, consumer discretionary, and healthcare sector. The table below shows the fund’s sector weight against that of its benchmark. This ability to try and find ideas outside of the benchmark has enabled us to find companies on which there is not much research coverage, which we believe to be an advantage. To add to that, even the larger names within our universe are still under-researched compared to many emerging market peers, providing an opportunity to find both value and growth ideas.

Overall, the fund’s 2014 performance was satisfying and the team undertook research trips, found new ideas, and managed macro events on a proactive basis. We believe that going forward it is this pro-active approach of meeting more companies, doing more research trips, and keeping our ears to the ground which will keep the fund in good stead. A lesson from 2014 was “Don’t Panic”. Macro events, both locally and globally, will continue to happen but our idea is to invest in companies which can benefit from a longer term trend and not from a few poor quarters. If we believe that these companies will be around for the next decade and even beyond, then any panic situation should be used to buy good companies. Our View for 2015 On a macro basis, the biggest event over the past few months which can have an impact on our key markets is the drop in the price of crude oil. Brent crude oil prices were down 46% in 2014 and have also started 2015 on a weak note. If weak prices continue for the better part of the year, this will have an impact on a majority of the fund’s portfolio. As mentioned in the November 2014 newsletter, markets such as Bangladesh, Pakistan, Sri Lanka, and Mongolia are net importers of crude oil, as it accounts for 14-26% of these countries’ total imports. Lower crude prices will be beneficial for these countries’ current account deficits and foreign exchange reserves and will help central banks manage monetary policy as inflation has already dropped across key markets of the fund. One net energy exporter within the fund universe is Iraq, which will see a negative impact on government revenues but has built up sizeable foreign reserves of USD 70 billion+ which should help the government manage the situation in the near term. Our largest country by holding, Vietnam, also depends to some extent on crude oil exports (~5% of exports) but it also imports refined petroleum products as there is a lack of refining capacity in the economy. The drop in crude prices should have a relatively neutral impact on the economy. More importantly, lower crude prices have led to lower inflation and fuel prices in Vietnam and this will be beneficial to the economy on a micro/company level.

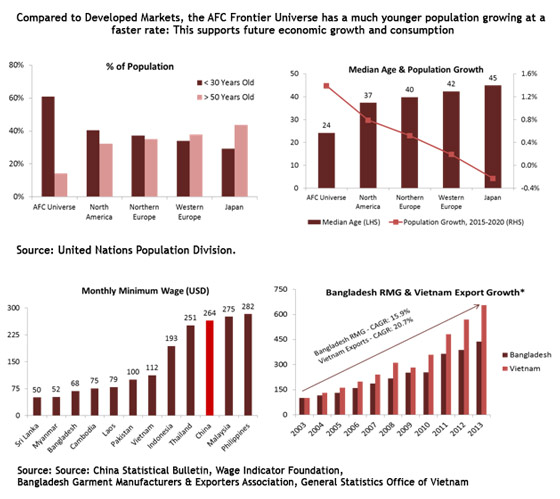

Lower crude prices can be a positive for the portfolio both on a macro and company specific basis as the fund is well positioned in the consumer and cyclical sector. Having said that, the fund could look to increase its exposure to consumer staples, consumer discretionary, and cyclical companies to take advantage of this trend of lower crude and commodity prices. Outlook for Key Markets Bangladesh Cambodia Iraq Laos Maldives Mongolia Myanmar Pakistan Papua New Guinea Sri Lanka Though there could be short term uncertainty over the new government, the outlook remains positive for Sri Lanka. The country continues to develop from the end of the war in 2009, is pushing further infrastructure development, and, like its South Asian neighbours, will benefit from lower crude prices in 2015. Tourism is a sector which holds lot of potential as Sri Lanka still only gets about 1.6 million tourists compared to other emerging Asian destinations like Vietnam and Cambodia which get about 7.6 million and 4 million tourists respectively. As the tourism infrastructure in the country develops, we would not be surprised to see tourist inflows reach the levels of its peers. We think consumer, infrastructure, and tourism companies are attractive in Sri Lanka. Vietnam Summary In conclusion, Asian frontier markets continue to be under-researched by the investor community relative to their emerging market peers and this will continue to provide opportunities to find new ideas and further explore existing investment theses. Besides being under-researched, Asian frontier markets offer a sound macro story in terms of favourable demographics, rising income levels, greater literacy, labour force growth, natural resources, and country-specific political and social reform which provides a platform for future growth. Another trend which can drive future growth in Asian Frontier economies is low cost wages in countries such as Bangladesh and Vietnam which are driving more manufacturing activity to these markets as wage levels increase in China. This trend will can further help reform infrastructure and generate employment leading to rising income and economic growth.

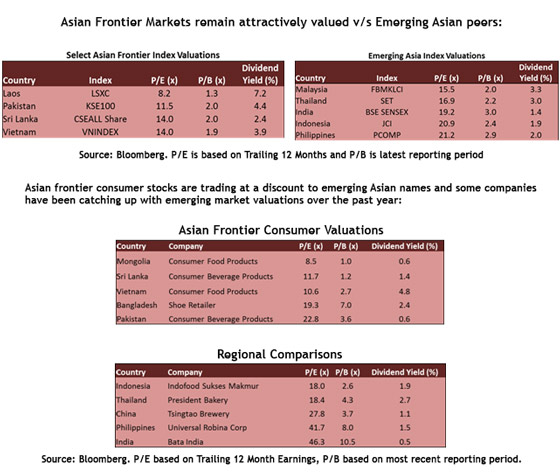

Valuation wise, Asian frontier markets continue to offer value on both a stock specific and overall market basis. We continue to hold certain consumer as well as non-consumer related companies which trade at a discount to emerging market peers, even though multiples for some consumer related companies have gone up over the past year. We are also watching our companies whose P/E multiples are expanding to make sure that expansion in multiples is being backed up by earnings growth or expected to be backed up by earning growth.

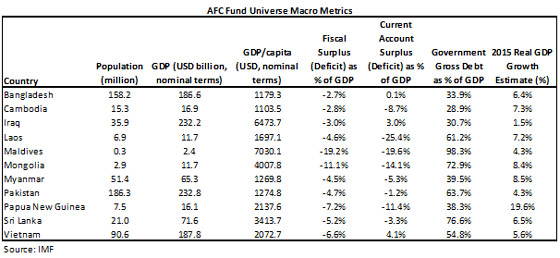

To wrap up, we will continue to take advantage of this favourable trend impacting our country universe as well as continue to invest in new ideas that have the ability to provide returns to investors. Given the nature of these markets, there could be short term bottlenecks at times, but we believe in taking a longer term view in investing in these markets. Below is a quick look at key macro metrics based on IMF estimates. Given the drop in crude oil prices, we expect these will change with respect to the 2015 growth outlook once IMF releases its next global economy outlook report in April 2015.

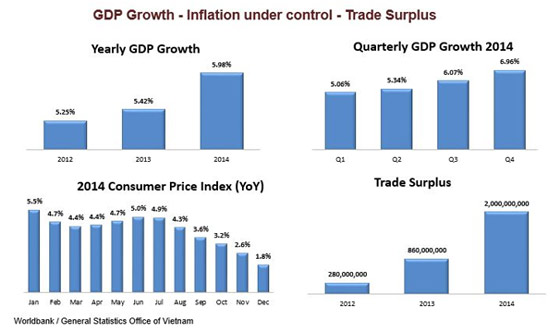

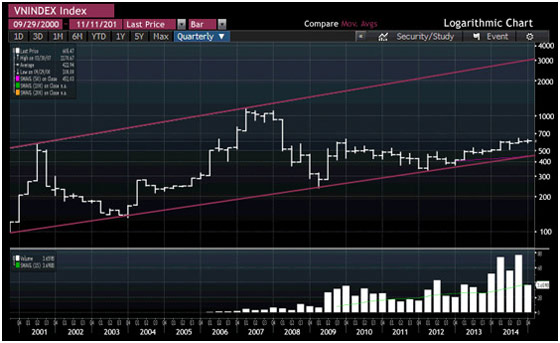

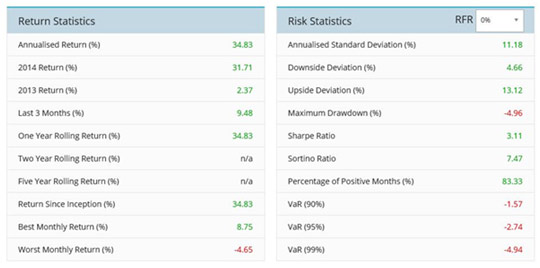

AFC Vietnam Fund – 2014 Annual ReviewLet it never be said that 2014 was an uneventful year for Vietnam. From diplomatic disputes with China to the equitization of state owned companies to a huge market rally that ended with a significant correction at the end of the year. Despite this tumultuous time, it is with great pleasure that we announce that the AFC Vietnam Fund was the most successful Vietnam Fund vehicle in the world in 2014 in its very first year of operation. The AFC Vietnam Fund has now returned +35.6% since inception on December 23, 2013 which represents a gain of +50.2% for CHF based investors and +52.8% for EUR based investors. Looking back to when the fund launched at the end of 2013, we were just at the beginning of an economic recovery in Vietnam, with a stable currency and the first attempts to implement a solution to the non-performing loan issue which was a result of the crisis between 2007 and 2012. Inflation was expected to stabilize at around 7%, allowing the export industry an even trade balance and the currency to remain relatively stable. At the time the consensus estimates of the financial analyst community was that earnings growth should be around 12%, and the stock market was expected to achieve a 25% to 30% overall return. Back in the present, we now see that the only correct forecast was that the currency remained steady to depreciate only around 1% against the USD. Against most other major currencies, including the EUR and the CHF, the VND significantly strengthened in 2014. Inflation has been revised lower, month by month and should be at a yearly average of around 4%, due to the collapse in the oil price. The trade balance, thanks to strong industrial and agricultural exports, should also be positive by more than one per cent of GDP. The banking sector is also recovering slowly as there was a much faster than anticipated recovery in the real estate sector which is stimulating the sector. Equally gratifying was the strength of the service sector which contributed to almost half of the economic growth - a very positive signal indeed for a developing country. On the negative side, the earnings growth of 3% to 4% was significantly weaker than the 12% forecast at the beginning of the year. With an improvement of the economic situation, most market participants would have expected much higher gains in 2014. Earnings revisions, territorial disputes with China in the South China Sea, Ukraine, Russia and the fall in oil prices are the key words, describing the weak stock market performance since the end of March. The moderate increase amounted to +9.0% in 2014 for Ho Chi Minh (+7.9% in USD terms and +6.2% since fund inception).

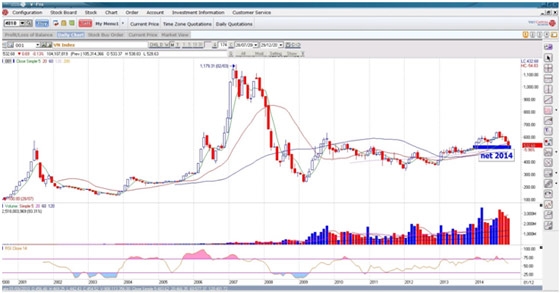

Given all these events, we are quite satisfied with the AFC Vietnam Fund’s performance during the past year. Our strategy of capturing the revaluation of undervalued small- and mid-cap stocks, has worked out perfectly well. As you can see from the blue bar (net 2014) in the chart above there was a minimal market increase for the whole year 2014. You could almost describe it as a very boring year, compared to the annual change since the stock market began 15 years ago.

There were 2 key events in 2014 which rocked the market. The first one was the oil rig incident on the Parcel Islands between China and Vietnam. This ongoing territorial dispute in the South China Sea doesn’t seem like it will be solved very soon but we don’t think that it is in either of the party’s interest to escalate this situation to a broader conflict. The other incident was the recent decline in oil prices, but we are of the opinion that declining oil prices are helping rather than hurting Vietnam’s economy, especially given the current shortage of refining capacity. The recent market correction is providing great buying opportunities and overall we remain very positive for this year. Negotiations for the TPP and EU free trade agreements are at advanced stages and their signing in the coming weeks or months could provide a nice catalyst for a flourishing stock market. Economic fundamentals still look attractive with record low December 2014 inflation of 1.8% (year on year), mainly due to the sharp fall in oil prices, and an economic growth this year which should continue to accelerate above 6 per cent.

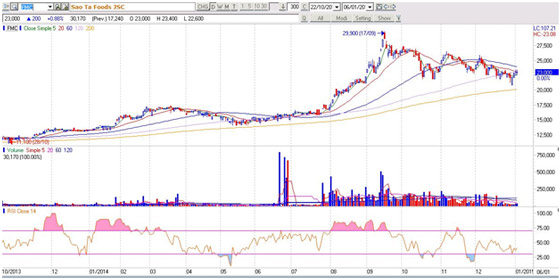

During the course of the year we experienced quite a few sector rotations within the Vietnamese equity universe. One of the industries we were invested early and that increasingly came into focus was the fish / seafood sector, which was completely neglected in 2013. Sao Ta Foods, which is one of our holdings, is a typical example of such a "discovery".

With strong earnings improvements over the past two years and an earnings valuation of around 8x, this stock more than doubled in the first nine months of 2014. In such circumstances, where positive news get the overhand and lead to exaggerations, we reduced our position. But since the fundamentals of the company are still intact, we took advantage of the recent correction and added to our position again. With macroeconomics mostly improving over the past year and a very stable outlook for 2015, we see even a higher potential for Vietnam now than 12 months ago. The correction over the last few months should be seen as the first cycle of a new bull market which has still years to go.

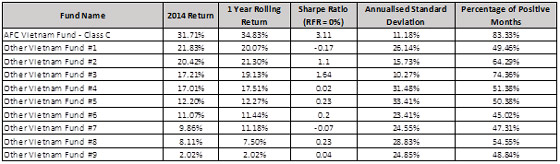

Looking forward for investors deciding how to play the Vietnamese bull market there are several options available but we, of course, believe strongly that well positioned active managers will outperform passive strategies in the coming years. Looking at the alternatives to our fund there is a general misconception by some investors that exchange traded funds (ETF) are always passive and track an index. In recent years there has been a growth in the number of active ETFs; however, in Vietnam the situation is very unique. ETFs typically have large assets under management and are all passively managed. They all face the problem that they can only invest in liquid stocks or large caps where the foreign investor limit is not yet full. This issue restricts their investment universe to only a few stocks and hence limits their diversification level. ETFs suffered from this constrain the last couple of years, where the Ho Chi Minh index went up 20% in 2013 and 9% in 2014, ETFs have hardly moved during that time. It is also worth mentioning the strengths of investing in an open-end fund versus some of the other structures. A key difference between a closed-end and an open-end fund is that the number of outstanding shares of an open-end fund can vary, whereas shares of a closed-end fund are fixed in number. An open-end fund will issue new shares, or repurchase old shares, as needed to meet investor demand, depending on whether money is being added to the fund or shares are being redeemed. The per share price is determined by the net value of all assets (NAV) held by the fund, divided by the number of shares. The per share price of a closed-end fund however, is determined by the level of demand and offer and it therefore can either have a premium or a discount to NAV. For example in Vietnam, where closed end funds typically trade at a deep discount to NAV, open-end funds are by far the most popular among typical investors. With an open-end fund, you can participate in the markets and have a great deal of flexibility regarding how and when you purchase shares. Also, you are never required to purchase shares at a premium or sell at a discount. Open-end fund managers have the flexibility to switch into cash in times of uncertainty or change their strategy to overweight more defensive stocks. Looking back at 2014 here’s how the closed and open ended funds investing in Vietnam stacked up:

When speaking to investors we often hear positive remarks about our high average dividend yield (6.1%) which is certainly attractive, but given that we are a value investor, our aim is to achieve long-term capital appreciation for investors by capturing value in growth companies; especially in the small to medium-sized company segment. In other words, the high dividend yields are rather the result of selecting undervalued companies with good earnings than using dividend yield as investment criteria. At the moment we still have a strong focus on smaller to medium sized companies since we believe that is where currently value is, given they are often undervalued and hence have a great potential to re-price. Currently, small caps trade at around 50 per cent discount to large caps. We already see this valuation gap narrowing for some time and we believe that over the next few years small caps will trade from currently “undervalued” to “neutral” and eventually to “overvalued” when retail investors are jumping to the bandwagon later in this rally. We see that happening all over the world throughout the history of stock markets and we definitely think that the Vietnamese mentality perfectly fits that thought. During that time of revaluation we will slowly but surely switch to large caps which tend to be the better bet during the latter part of a bull market.

There are several factors why we believe that the Vietnamese stock market remains attractive. Given the current low inflation, we believe that the SBV (State Bank of Vietnam) will have further room to cut interest rates. The impact on lower interest rates is not to underestimate, a 1% cut in loan rates would trigger the GDP to increase by almost 0.5%. We mentioned before that Vietnam is expected to sign the TPP and the EU FTA, but there are also some other very important FTA’s (Free Trade Agreements) soon ready to be signed, such as ASEAN (AFTA), ASEAN-China (ACFTA), Viet Nam-Customs Union of Russia, Belarus, and Kazakhstan Free Trade Agreement and ASEAN-Korea (AKFTA) which all will help the economy to flourish. In principle we do agree with the view of the World Bank and the Asian Development Bank which both raised their forecasts for Vietnam’s economic growth in 2015 end of last year. Our views stem mainly from improved consumer confidence and more favorable economic conditions and a sustained macroeconomic stability and last but not least the progressive expansion in the country’s, foreign invested, manufacturing exports sector.

Source: Asian Briefing The recent strength of the US Dollar and the very stable exchange rate of the Vietnamese Dong certainly brought up some discussion about disadvantages for the Vietnamese export industry and a possible devaluation. But with a history and bad experience of high inflation and a weak currency just a few years ago the government is committed now to a relatively stable currency which is also lowering input prices and give foreign investors – which are the main reason for the recent improvement of the economy – a stable environment for long term decisions on investing in the country. Main competitors in the region like China, Thailand, or Cambodia also have currencies which were relatively stable to the US Dollar and countries with weak currencies like Japan are not really playing on the same field of production. Furthermore, investments in the infrastructure sector, for example, are gaining on value in their home currency for these countries. In closing, we see 2015 holding great opportunity for Vietnam and look forward to continuing to build on our performance in the coming year. If you are currently invested in Vietnam through ETFs or other passive strategies, we would encourage you to rethink this approach for 2015 and consider joining the AFC Vietnam Fund for another year of boutique fund returns. |

||||||||||||||||||||||||

|

I hope you enjoyed reading this month’s newsletter. Best wishes for the New Year to all our readers from the whole AFC Team. Thomas Hugger |

|||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||