Asia Frontier Capital (AFC) - September 2014 Newsletter |

||||||||||

In this IssueAFC Asia AFC Vietnam Fund

|

"Don't lower your expectations to meet your performance. Raise In September 2014 the AFC Asia Frontier Fund returned +2.1% and AFC Vietnam Fund returned +3.9%, bringing the YTD total for our funds to +21.1% and +25.0% respectively. The MSCI Frontier Markets Asia Index (+0.5%), MSCI Frontier Index (+0.4%) and the MSCI World Index (-2.9%) all had a less enthusiastic month in comparison, but the biggest move was from the MSCI Emerging Markets Index, which dropped a staggering -7.6% in September. Looking a little closer to home, there was some excitement near our head office starting at the end of September with protests overtaking Hong Kong as part of the “Occupy Central” movement. Whilst this has caused some minor inconveniences in our daily commute it has not impacted the daily operations at our head office or our funds. New capital has continued to flow into both of our funds and we would like to welcome on board our new investors who have joined us this month and existing investors who have increased their allocations. AFC Asia Frontier Fund: USD 10 Million Milestone Special Offer Winner Announcement – No Fees for 12 months -!With this month’s new investments the AFC Asia Frontier Fund has now pushed beyond one of our first AUM milestones to reach close to USD 11 million. And now for the results of our draw - the winner is… Mr. E.B. who is based in Ireland.

The draw was done by Mr. Dominic Cham (right) from our fund administrator Amicorp Fund Services, Hong Kong at 3pm on the 7th October 2014. If you have any questions regarding the results of the draw or the subscription process please be in touch with Stephen Friel at AFC NewsAFC on New Fund Platform - Generali The AFC Asia Frontier Fund has now been included on the Generali fund platform (http://www.generali.com/generalicom/) to complement our inclusion on the Royal Skandia fund platform (http://www.skandiainternational.com/en). This month we have again received several enquiries from clients regarding other fund platforms and we are in discussions with several other parties. The majority of platform providers indicated that they are able to begin their internal due diligence process on our funds when they receive a request from their existing clients. If you would like assistance investing via your existing fund account please be in touch directly with them to enquire. We are also happy to help expedite this process on your behalf and encourage you to be in contact with our Marketing Director Stephen Friel AFC in the Press

Upcoming AFC TravelIf you will be in any of the locations listed below and have an interest in meeting with our team, please contact our Marketing Director Stephen Friel at

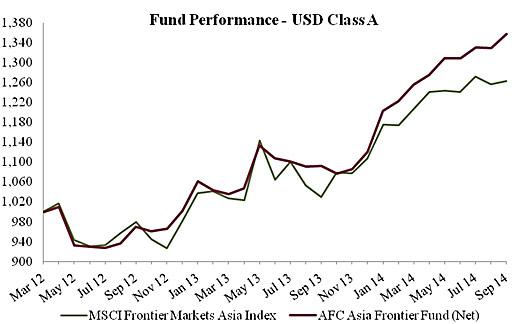

AFC Asia Frontier Fund - Manager CommentAFC Asia Frontier Fund (AAFF) USD A-shares were up +2.1% in September 2014, outperforming the MSCI Frontier Markets Asia Index (+0.5%), the MSCI Frontier Markets Index (+0.4%) and the MSCI World Index (-2.9%).

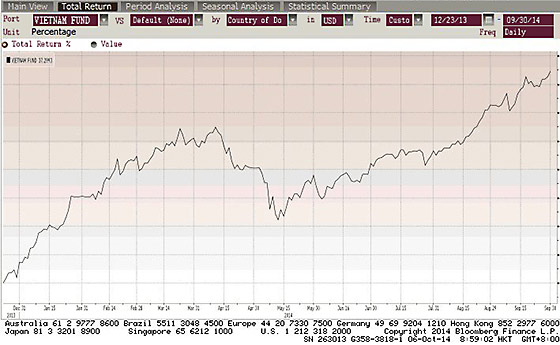

September saw a significant bounce in performance from the previous month, which ended flat, as political tensions in Pakistan subsided which led to AAFF’s Pakistani holdings rallying. Besides being aided by an uptick in Pakistan, a consumer and a healthcare holding in Bangladesh as well as the fund’s infrastructure and consumer holdings in Sri Lanka also helped bolster the positive performance. Many of the fund’s holdings that have performed well during the month as well as year to date are companies which are not part of the relative index, i.e. MSCI Frontier Markets Asia Index. Whilst we do include this index as an indicator of our fund’s comparative performance, it is important to note that our investment strategy is not benchmark constrained in relation to it in any way. This is one of the reasons the fund has been able to show a strong performance over the past year as this strategy allows us to look for opportunities not included in the index. Though the political noise in Pakistan has subsided, the situation has not fully returned to normal as there continues to be incidents of political protest from certain opposition parties. If the pressure from the opposition continues to mount, there are talks/rumors of mid-term elections but this is not confirmed. Then again, one must keep in mind that the political situation in Pakistan has a history of being unstable and this is to some extent reflected in valuations. The more important impact of the political issues surrounding Pakistan is the macro stability given that the government has committed to reforms due to the financial package it received from the IMF last year. Any political pressure to not go ahead with the reforms as per the IMF agreements could put some pressure on the country’s macro outlook. In our other key markets such as Bangladesh, Sri Lanka and Vietnam the political and economic situation has remained stable this year. Mongolia continues to grapple with the Rio Tinto / Oyu Tolgoi issue while the situation in Iraq has reached a point where Western governments appear to be on the same page to remove the ISIS threat, but this could be a long drawn out affair and is not something that will be completed in a few weeks. In Cambodia, our gaming play continued to post good gross gaming revenue numbers even though Macau has seen a drop in this metric over the past quarter. The best performing indices within the AAFF universe in September were Bangladesh (+10.8%), followed by Pakistan (+4.1%) and Sri Lanka (+3.1%). The poorest performing markets were Vietnam (-5.9%) and Laos (-3.8%). The top-performing portfolio stocks were a Mongolian mining company (+42.6%), followed by a Pakistani health care company (+40.2%), a Pakistani car producer (+26.5%) and a Sri Lankan conglomerate (+19.6%). In September we added to existing positions in Cambodia, Laos, Mongolia, Pakistan, Papua New Guinea, Sri Lanka and Vietnam and we reduced one holding in Vietnam, two holdings in Pakistan and sold the entire position of a glass manufacturer in Sri Lanka. We added a new Mongolian cashmere producer and a Vietnamese construction company. As of 30th September 2014, the portfolio was invested in 116 shares, 1 closed-end fund (with 32.5% discount to NAV), 1 GDR (with 68.4% discount) and held 7.4% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (.5.5%) and a pharmaceutical company in Pakistan (3.5%). The countries with the largest asset allocation include Vietnam (22.2%), Pakistan (18.7%) and Bangladesh (13.5%). The sectors with the largest allocation of assets are consumer goods (39.9%) and materials (13.9%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 13.87x, the weighted average P/B ratio was 1.79x and the dividend yield was 4.28%. AFC Vietnam Fund - Manager CommentTo review this manager comment in German please click here. In September 2014 the AFC Vietnam Fund (AVF) returned +3.9% bringing the YTD performance to +25.0%. The VN Index and VH Index returned -5.9% and +1.8% respectively in September. As the fund NAV is calculated monthly it can be difficult for our investors to see the movements in fund performance on a more regular basis. As such, we have put together the daily fund returns (gross) of our portfolio since inception which can be seen below.

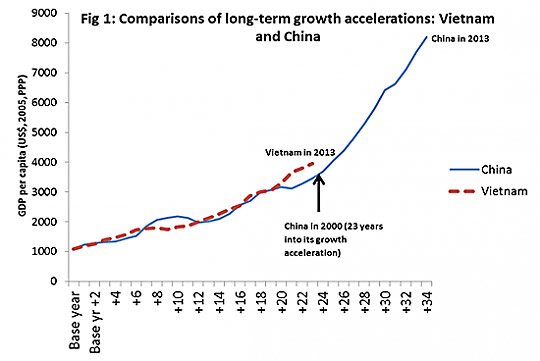

September was not an easy ride for the Vietnamese stock markets. At the beginning of the month, the momentum, especially for the heavily weighted oil shares in Hanoi, remained very positive, until mid-month profit taking took place. Nevertheless, the Hanoi VH Index finished slightly positive which was significantly better than the much more well-known Ho Chi Minh VN Index. Some of our holdings had very good buying interests and managed to increase within a few weeks by 20-40% which according to our standards is "expensive" with a valuation of almost 10x (price/earnings ratio). We therefore sold some of these positions and increased our cash portion to around 9%, but also started to build up several new positions. Even though many of our larger companies also corrected, we were able to continue the increase of our NAV in September. After the index increased by approximately 20% between May and the end of August, a correction at this level is, on a medium term view, positive and we expect that the upward trend will continue again in October. Economic growth increased in the third quarter by +5.6%, according to preliminary figures, suggesting a full year growth rate of almost 6% which we regard as realistic, given that inflation currently stands at just under 5% - even though some other sources are slightly less optimistic. We ask ourselves what the longer-term development of the stock market could look like. Even if the current valuation compared to other markets is much cheaper and the economic outlook remains very healthy, there are more and more people arguing that the Vietnamese stock market is no longer cheap now. With a price / earnings ratio of nearly 15x and barely profit growth for 2014 - in stark contrast to our 70 shares in the fund - this certainly seems to be correct on the first sight. The current favourite sectors, especially of foreigners, are energy, real estate and food, which are weighted with a total of just over 50% of the index. If you however would exclude these three sectors, then a very different picture appears: Suddenly the valuation of 15x would drop to 11x, compared to an average of about 7x in our portfolio of shares. In the short term, the market is oversold like we haven’t seen for many years and we expect it to rebound. From a medium term perspective, we are still slightly overbought and therefore rallies will probably be more modest in scale. We also think that sector rotations will take place, which should further benefit our fund portfolio. From a long-term perspective, however, nothing has changed. Taking the example of the development of China we see very well the stage where Vietnam currently is at. We can also go back a little bit further and compare it to the economic recovery in Germany in the 50s and 60s, where a hardworking nation with low economic growth caused a boom in the economy and the stock market. Germany saw stock market price increases by 60-80% in the late 50s for two consecutive years’ and only after a modest increase in the third year did the market finally see a correction of 30%. Although we do realize that a constant increase from year to year is not realistic, we strongly believe in the overall positive developments that we expect to continue in the coming years in Vietnam, which will typically end in a massive exaggeration on the upside.

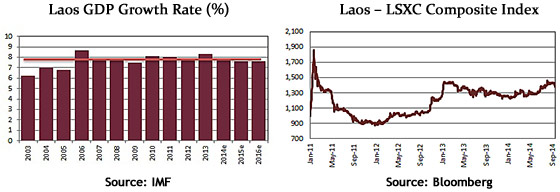

In September the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (3.0%) - a manufacturer of electrical and telecom equipment, KLF Joint Venture Global (2.5%) – a real estate company, Gypsum and Cement JSC (2.4%) – a cement company, Dong Nai Port JSC (2.3%) – a port operator and FLC Group JSC (2.2%) – a real estate development company. As of 30th September 2014 the portfolio was invested in 69 shares and held 9.0% in cash. The sectors with the largest allocation of assets were consumer goods (32.8%) and industrials (20.4%). The fund’s weighted average trailing P/E ratio was 7.02x, the weighted average P/B ratio was 1.02x and the average dividend yield was 6.35%. AFC Country Snapshot: LaosAlthough one of the few remaining one-party communist states, the Laotian government’s attempts to decentralize control of the economy and encourage private enterprise starting in 1986 have resulted in an annual growth rate of 6% from 1988-2008. Laos’ economy has maintained consistently high GDP rates through 2012 due to strong growth among its main trading partners in the region, particularly China. High prices on the global commodities market have improved foreign interest in Laos’ extractive sector prospects, and foreign mining companies are increasing production and looking to attain additional concessions. Laos looks to benefit from an increase of agriculture production, which accounts for 33% of GDP and employs 75% of the population, as large swaths of land have been leased to foreign investors for greater agricultural development. Laos is looking to complete two massive railway projects in the coming years - costing upwards of USD 12 billion - with the intention of connecting China, Thailand and Vietnam via Laos. These new railway lines should significantly boost trade and tourism for the country which presently has only 3.5km of operating rail.

Stock Market: The Lao Securities Exchange (LSX) was founded in January 2011 with technical and financial support from South Korea. LSX, headquartered in Vientiane, currently lists 3 companies; EDL Generation-Public Company - a subsidiary of the state-owned energy company Electricite du Laos, Banque Pour Le Commerce Exterieur Lao (BCEL) - the country’s largest bank and Lao World - a property services company. LSX has a total market capitalization of US$ 1.2 billion as of September 2014.

Country snapshots for all of AFC's markets can be found on our website at www.asiafrontiercapital.com AFC Country Report: LaosTiny Laos is drawing interest from Asia’s largest economies – China, Japan, and South Korea – due to its strategic location, natural resources, and low cost of labor. But much of Laos’ rising significance is due to the changing landscape of Asian politics, as China and Japan jockey for geopolitical influence and trade in Southeast Asia. Building ties with once-ignored countries like Laos is increasingly becoming part of the political and economic calculus for both Beijing and Tokyo. In the aftermath of the sovereignty dispute between China and Japan that occurred in April of this year over the Diaoyu / Senkaku Islands, Japan decided in July to lift the ban on its armed forces fighting overseas. The move was significant, as it marked the first change to Japan’s 70-year-old pacifist constitution and also demonstrated how the rising might of China is increasingly making some of its regional neighbors uneasy. Japan’s plan to counter Chinese ambitions focuses on bolstering aid and investment in Laos, Vietnam, Cambodia, and Myanmar, all countries that have traditionally maintained close links with Beijing. Laos, however, shares many cultural similarities to Thailand, a country in which Japan has invested heavily and which continues to be a strong trade partner for Tokyo. Japan hopes to leverage its successful track record in helping to develop Thailand’s economy and infrastructure to pivot into Laos to gain access to the country’s low wages and untapped opportunities, in addition to its own political agenda of countering Beijing’s influence. Japanese companies like Toyota and Nikon, for instance, have recently opened production and assembly facilities in Laos, and Japanese investment in Laos has recently grown by nearly 15x, from USD 27.5 million in 2012 to USD 406 million in 2013. This uptick is visibly evident on the streets of Vientiane, Laos’ sleepy capital city of around 800,000, where Japanese businessmen are a common sight and an unsuspecting visitor might be surprised to find 12 Japanese restaurants in Vientiane alone! Japan is hoping that its renewed push for investment and trade links with countries like Laos and Myanmar is coming at just the right time, as an increasing number of Asian countries have recently begun expressing concern over their economies becoming far too dependent and intertwined with China. In Myanmar, China was historically embraced by the former junta as a key trading partner and investor, but hostile attitudes towards China have grown, as many people in Myanmar see Beijing as only interested in the country’s resource and energy potential and the opportunity to build oil and gas pipelines across Myanmar to Kunming in Yunnan Province. Others believe that China is directly to blame for the longevity of the military government’s rule, as its status on the UN Security Council allowed Beijing to block any Western interventions into Myanmar. The statistics speak for themselves on the fraying relationship between Myanmar and China: Chinese investment in Myanmar dropped from USD 12 billion between 2008 and 2011 to just USD 400 million for the 2012-13 financial year. Like Myanmar, Laos has also had historically strong economic ties with Beijing – China is one of the country’s largest trading partners alongside Thailand and Vietnam. China’s interest in its southern neighbor is principally due to Laos’ strategic location and natural resource potential, from hydropower projects to reserves of gold, silver, copper, and potash. China’s headline project in Laos is certainly its proposed 418 km high-speed railway connecting Kunming to Vientiane, which comes at a price tag of a whopping USD 7.2 billion, accounting for more than 60% of Laos’ USD 11 billion GDP. The Renminbi-denominated loan to finance the project is so large that some economists have speculated that Laos might even consider pegging its currency, the Kip, to the yuan to hedge against any increases in the debt burden due to currency fluctuations. But despite China’s grandiose infrastructure plans, wariness of Beijing’s motives is increasing in Laos, as the proposed railway project would involve 5 million metric tons of minerals, mainly potash, being exported from Laos to China every year until 2020, in addition to numerous other timber, agricultural, and mining concessions. In addition to saddling the Laos government with a comparatively enormous debt burden, another criticism of the project is that it is unclear how it will stimulate Laotian job growth or economic opportunities – the 5-year construction of the railway will rely on bringing in 50,000 Chinese workers instead of sourcing laborers from the local population, one-third of whom live below the global poverty line of USD 1.25 / day.

The Lao Securities Exchange (LSX), established in 2011, remains very small and currently lists only three companies: Electricite du Laos Generation Public Company (EDL-Gen), Banque Pour Le Commerce Exterieur Lao (BCEL), and Lao World Public Company (LWPC). PetroTrade, a major fuel distributor in Laos with 106 fuel stations nationwide, announced plans in to prepare for a listing on the LSX in Q4 2014. PetroTrade is looking to raise capital to help build two additional fuel storage facilities, one in Champassak province able to store 700,000 liters of fuel for general vehicle supply, and one in Vientiane able to hold 1.3 to 1.5 million liters of aviation fuel. A successful listing would make PetroTrade the fourth stock on the exchange and help to grow the market capitalization and liquidity of the bourse. There are several companies listed on overseas exchanges that have operations in Laos, including PanAust, a Brisbane-based copper and gold mining and exploration company listed on the Australian Securities Exchange (ASX), MMG Limited, a Melbourne-based mining company that operates the open-pit Sepon copper mine in Laos and trades on the Hong Kong Stock Exchange (SEHK), Kolao Holdings which trades in Seoul, South Korea and is a car distributer, and Asia Potash Group, a Sichuan-based company that operates potash mines in Laos and has announced plans to list on the SEHK. AFC Travel Report: LaosIn line with our process of being on the ground in the countries we invest in, AFC's Contributing Writer, John Enos, travelled to Laos in August to cover the country's development from the ground. Perhaps the best indicator that you have arrived in a frontier market still overlooked by investors is that the taxi drivers waiting around the airport arrivals hall seem to be surprised that you are interested in their services. At Vientiane’s tiny Wattay International Airport, which receives only a handful of international flights a day from Bangkok, Hanoi, Seoul, Kuala Lumpur, and Kunming, I probably could have picked up my backpack and walked or bicycled into town. It was drizzling lightly and I didn’t know exactly where I was going, so I followed the taxi driver, who still seemed incredulous that he already had one customer before lunchtime! Laos’ official name is the Lao People’s Democratic Republic, otherwise known as Lao PDR. The joke among travelers and expats is that Lao PDR actually stands for Lao, Please Don’t Rush. This becomes clear to any newcomer almost immediately upon arriving in Laos, whether it is by air at Vientiane’s small airport or by bus over the Thai/Lao Friendship Bridge connecting Udon Thani in northern Thailand with Vientiane. Coming from the big city hustle and bustle of Bangkok or the chaotic traffic of Ho Chi Minh City or Phnom Penh, Vientiane seems like a capital city that is still awakening from a deep afternoon nap. The main thoroughfare in downtown Vientiane is lined with haute cafes, tour agencies, and high-end gift shops, but despite the increasing number of luxury SUVs backed up on the street, the main road still only has one lane of traffic in each direction and can easily be crossed on foot, with no stoplight. In the late 19th century, the territories of Luang Prabang and Vientiane were added to French Indochina, and the Gallic influence in Laos can still be felt to this day, from the abundance of quaint Parisian cafes serving fresh croissants to various French names one comes across, such as the national electricity corporation, Electricite du Laos. Although Vientiane is small, walkable, and roughly mapped in a grid-like fashion, I found myself continuously getting lost on foot. I blame a combination of my lack of a background in French and the fact that Lao names are nearly impossible to pronounce and can be spelled a multitude of ways. Several times a day I’d find myself chasing down an unsuspecting Laotian to ask if he could direct me to Rue Setthathilath or Rue Nokeakoummane or how far it was to the intersection of Quai Fa Ngum and Rue Chanthakhoumane? Now imagine asking for these directions while dripping sweat in the 34 degree Celsius Laotian heat and you can quickly understand my frustration at having learned no words of French, Lao, or Vietnamese in school. In many ways, Vientiane is quite similar to Phnom Penh, the larger capital of Laos’ southern neighbor, Cambodia. Both cities are adjacent to a river, and the promenade along the riverbanks is a gathering spot in both Vientiane and Phnom Penh for old men to drink, young children to frolic, and middle-aged women to do sunset calisthenics en masse. Strolling along the banks of the Mekong River in Vientiane, one soon reaches the massive statue of Chao Anouvong. Anouvong was the last monarch of the Lao Kingdom of Vientiane who is a famed hero in Laos for leading the Laotian Rebellion in the 1820s against the Siamese to gain complete independence from Thailand.

In Laos, of course, the drink of choice is inevitably Beerlao, the fabled lager that has a reputation so prominent that the company’s marketing director and head of international sales once told a reporter in an interview that when he visited international beverage distributors, even in Asia, many of them had heard of his beer but had not heard of his country! It is unclear when Beerlao’s immense popularity took off, but seasoned expats and gap-year backpackers helped to create a customer base for the lager that stretched far beyond the quiet streets of Luang Prabang or the bacchanalian banks of the Nam Song River in Vang Vieng, long a mecca for hard-partying travelers looking to discover the hedonistic side of the country. Beerlao is brewed by the Lao Brewery Company, which was nationalized in 1975 when the Lao PDR was officially established, and in the early 2000’s, Danish brewing giant Carlsberg and its Thai partner each acquired a 25% stake in the company. Although the beer was originally based on locally-grown jasmine rice, Beerlao has since rolled out a number of new products, including Beerlao Dark and Beerlao Gold. A bottle of the extraordinary lager goes for about 10,000 Kip in Vientiane, roughly USD 1.25, and it is easy to see why the locals are so proud of their national tipple and why the company enjoys a market share of 99% of the beer sold domestically.

Apart from the plethora of farangs (Lao word for foreigner) and visa runners that I saw swigging Beerlao, one other thing I noticed in Vientiane was the abundance of Japanese businessmen, which I certainly did not recall seeing when I had previously visited the city two years prior. I counted upwards of 10 Japanese restaurants in the tiny capital, many of which had menus in Japanese, with pretty Lao staff courting customers on the sidewalk with catch phrases in Japanese, all of which were lost on me. As discussed in the country report on Laos also in this newsletter, Japan is increasingly focusing on peripheral Southeast Asian countries as part of its geopolitical strategy to counter China’s influence in the region, and Japanese businesses seem to be welcoming this effort by expanding production facilities in Laos due to the country’s close proximity to Thailand, which is a long-standing trade partner of Japan, and Laos’ low labor costs. But despite the recent increase in foreign businessmen and the usual backpackers and Thai visa runners, Vientiane remains a pleasant, quiet town still very much connected to the traditional Lao way of life. Buddhism is the main religion in Laos and has shaped much of the culture, but animist traditions and belief in traditional spirits is still an integral part of Laos’ national psyche and one can sense the deep impact that both Buddhism and Animism have had on Laos through the country’s food, culture, and even clothing. One of the most interesting and unusual moments of my trip was when I was walking next to one of Vientiane’s few recently-opened shopping malls and stumbled upon a woman sitting on the sidewalk hawking herbs, roots, and all sorts of other unusual leaves and bits of bark. A young Lao bypasser seemed interested in my curiosity, and after a short conversation with the old woman selling the goods, he explained that the wares were all key ingredients for various traditional medicines. According to one study, over 70% of Lao households still use traditional medicine! I found this scene quite enthralling on my last day in Vientiane, and the sight of an old woman peddling medicinal ingredients speaks volumes of Laos’ continued close connection to the country’s traditional culture and beliefs.

I hope that even with the rise of Beerlao’s fame or the country’s attractiveness to foreign companies, the unique cultural heritage of Laos remains intact! |

|||||||||

|

I hope you enjoyed reading our monthly newsletter and remain with kind regards, Thomas Hugger |

||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

||||||||||

GO TOP |

||||||||||

Source: Bloomberg

Source: Bloomberg Source: EMIA, Penn World Table

Source: EMIA, Penn World Table

Source: The Economist

Source: The Economist Anouvong, Leader of the Lao Rebellion

Anouvong, Leader of the Lao Rebellion Enjoying the legendary Beerlao Dark Lager for a bit over a dollar a bottle

Enjoying the legendary Beerlao Dark Lager for a bit over a dollar a bottle A variety of roots, herbs, leaves, and bits of bark being hawked

A variety of roots, herbs, leaves, and bits of bark being hawked