Asia Frontier Capital (AFC) - July 2014 Newsletter |

|||||||||

In this IssueAFC Asia AFC Vietnam Fund

|

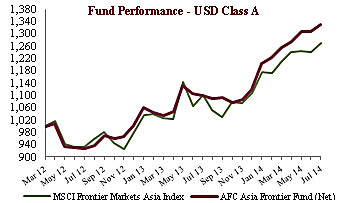

"Let him who would move the world first move himself." In July 2014 the AFC Asia Frontier Fund returned +1.6% and AFC Vietnam Fund returned +1.9%, bringing the YTD total for each fund to +18.7% and +14.1% respectively. New capital has continued to flow into both funds and we would like to welcome on board our new investors and thank existing investors who have increased their allocation to our funds. Looking at our markets, July was a relatively quiet month for Asia Frontier Capital when compared with the events that unfolded in the previous two months. The exception to this relative calm is in Iraq which has seen another escalation in the ISIS threat to peace and stability over the past few days. Events in emerging and frontier markets outside of our investment universe have become increasingly dramatic, which highlights that South and South East Asia are somewhat unique in the frontier world. With ongoing issues between Russia and Ukraine driving uncertainty in Europe as well as a - technical - default by the Argentinean government on its international debt obligations, South America has also been causing concern to investors. Across the Middle East there has been a dramatic increase in regional tension following the flare up in violence between Israel and Palestine. News out of several West African nations also indicates that the containment of the deadly Ebola virus has so far not been successful. Guinea, Sierra Leone and Liberia have confirmed several hundred cases causing death with the most recent victims coming from Nigeria's capital Lagos (which is Africa's most populous city). These issues highlight the importance of regional political stability, the threat of violence and the state of the disease environment when looking for investment returns. Take for example the outbreak of Ebola which has not only tragic health outcomes but also drastic economic consequences as this issue can have a dramatic effect on the output of human capital within the overall population. A worsening of health outcomes lowers overall productivity and can decrease growth as well as education outcomes in developing economies as people stay away from work and school. Looking forward at the options available to contain the contagious disease the potential to negatively impact regional trade is very high should governments introduce quarantine measures to reduce the risk of spreading infection. The effects of this can already be seen, with the GDP growth rate of Sierra Leone falling by 1% since the Ebola outbreak began. Whilst AFC has a great deal of belief in the future opportunities of frontier markets generally, we specifically see the health, educational and political environment in the Asian frontier, particularly in South and South-East Asia, as offering the greatest opportunity as well as returns for equity investors in the coming decades. AFC NewsAFC in the Press

A New Way to Invest in AFC Asia Frontier Fund USD -A-: It is now possible to invest in AFC Asia Frontier Fund USD -A-via the Royal Skandia and the Skandia International fund platforms. If you have an account with these providers and would like to invest in this way please ask your Skandia account manger or email Stephen Friel at AFC Wins Alternative Investments Awards With the awards season in full swing, AFC's funds have continued their climb to the top of the tables after producing a great performance despite some uncertain moments in global markets. As part of the Alternative Investment Awards 2014 AFC has won the following prestigious awards:

Upcoming AFC TravelIf you will be in any of the locations listed below and have an interest in meeting with our team, please contact our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager Comment

July was a relatively calmer month compared to last month where various country and macro events played out in Iraq, Pakistan and Vietnam. The fund saw a rebound in performance for some of its larger country holdings like Pakistan and Sri Lanka which saw AAFF holdings in these countries gain by +4.1% and +8.7% respectively, outperforming the respective country indices. Though we expected Pakistan to be quiet during the month due to Ramadan, this was only the case for Bangladesh, where we did not see lot of action. The Vietnamese economy continues to stabilize and posted GDP growth of +5.0% for the fourth quarter in a row which is a positive. The situation in Iraq remained fluid during July but as of writing, the U.S. has authorized and begun airstrikes on ISIS targets in Northern Iraq. This should not come as a surprise given the strategic importance of Iraqi oil assets to western and US interests which we mentioned in the June 2014 manager comment. The launch of air strikes could possibly be a negative for market sentiment as this reflects the gains ISIS is making in Iraq but if Iraqi authorities can make some gains along with US support then this could offer some respite to market sentiment. The Iraqi parliament has already elected a new Speaker of parliament and a new President. What remains to be seen is who will be the new Prime Minister and talks continue on coming to some sort of compromise on this issue. We continue to monitor the situation but expect it to remain fluid in the coming few months and do not expect Iraq to be a significant part of our portfolio until we see more clarity on the political front. If there is momentum on some sort of political compromise then the fund could look at some of the better companies whose stock prices and valuations have been beaten down. The Mongolian currency remained weak and we believe that sooner or later the Mongolian government will have to sort out issues related to the Oyu Tolgoi expansion or agree to some sort of funding from a foreign government in order to attract foreign direct investment (FDI). This could be a positive trigger for the Mongolian market. The best performing indexes within the AAFF universe in July were Laos and Sri Lanka (each up 6.8%), followed by Vietnam (+3.1%) and Mongolia (+2.5%). The poorest performing markets were Cambodia (-5%) and Iraq (-1.9%). The top-performing portfolio stocks were a Mongolian construction company (+41%), followed by a Mongolian junior copper mining company (+36.4%), a Sri Lankan food company (+28.1%), a Vietnamese food producer (+19.8%), and a Cambodian junior gold mining company (+17.7%). We continue to track and invest in companies we like and have met with either on the ground or at investor conferences. Consumer, cement and textile stocks in Pakistan and infrastructure and consumer names in Sri Lanka are some sectors and companies we are confident in with respect to future outlooks due to macro positives and/or undervaluation relative to where these companies can trade at going forward. The quarterly season is already upon us in most of our key markets and the numbers for our larger holdings which have declared results look good and we expect the same for companies which will declare results this month as well. In July we added to existing positions in Bangladesh, Cambodia, Mongolia, Pakistan, Sri Lanka and Vietnam and we reduced one holding in Vietnam. We sold three entire positions of Vietnamese companies: a light bulb manufacturer, a steel producer and a manufacturer of home entertainment products. As of 31st of July 2014, the portfolio was invested in 114 shares, 1 closed-end fund (with 27% discount to NAV), 1 GDR (with 54.7% discount) and held 7.7% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.4%) and a junior copper mine in Mongolia (3.8%). The countries with the largest asset allocation include Vietnam (20.9%), Pakistan (18.7%) and Bangladesh (12.4%). The sectors with the largest allocation of assets are consumer goods (38.3%) and materials (14.6%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 14.39x, the weighted average P/B ratio was 1.69x and the dividend yield was 4.67%. AFC Vietnam Fund - Manager CommentTo review this manager comment in German please click here. In July 2014 the AFC Vietnam Fund returned +1.9% which was an outperformance of the VH Index (+1.7%) but an underperformance versus the VN Index which returned +3.1%. July was, as expected, a quiet month in terms of volume, with comparatively low volatility. The Ho Chi Minh index had a quick upward move due to a rumor about a JV between Apple and a local technology company which was denied quickly. There was also a strong performance in a few companies which are already 49% foreign owned. The overall increase of in the Ho Chi Minh and Hanoi indices does not reflect the broad market and hence we must be satisfied with the moderate fund returns this month. The Vietnamese economy, however, remains on the road to recovery. Foreign investments helped to improve the industrial production (+7.5% in July yoy) and the trade balance. There are now clear signs that domestic demand is also picking up. In the first half year of 2014, retail sales rose by 11% to almost USD 80 billion and the consumer confidence rose to 134.1 in July from 131.0 in June. 55% of Vietnamese families believe in an improvement in their financial situation over the next 12 months, whilst only 6% expect a decline. It is quite a different picture in Europe! Only the Purchasing Managers' Index declined, but still remains on a level of expansion. The increase in the credit rating by Moody's from B2 to B1 reflects the improved overall situation of Vietnam. It is impressive to see the international confidence in the economic future of Vietnam. More and more globally-leading companies are betting on Vietnam. If companies such as Intel, Samsung, and various textile companies shift their major production sites to Vietnam and are hence economically dependent for years, this should strengthen our confidence too. With an increase in exports of 14% in the first seven months and a trade surplus of USD 1.26 billion, there are now mainly higher quality products that are gaining in importance. In addition to Samsung, which will soon manufacture more than half of all their smartphones in Vietnam, Intel has also recently announced impressive figures. By the end of next year, 80% of all of Intel's computer chips will be produced in Vietnam. According to Sherry Boger, CEO of Intel Vietnam, low error rates and the rapid adaptation of the local workforce to Intel guidelines were the main reasons for this fast development of the company's Vietnamese factory, which is only four years old. As an example, the same process took over 15 years in Intel's Chinese Chengdu factory. One would assume that ultimately also listed local companies will benefit from this dynamic economic development. About two-thirds of our holdings have now announced their results for the second quarter of 2014. Out of these nearly 50 companies only 3 have so far disappointed, while the remaining companies reported decent to very good results. We are also in the process to invest in some new companies, such as a turnaround story of a pharmaceutical company, which trades 50% below its book value with a P/E ratio of 5.5x according to our current forecast and therefore seems to be extremely undervalued.

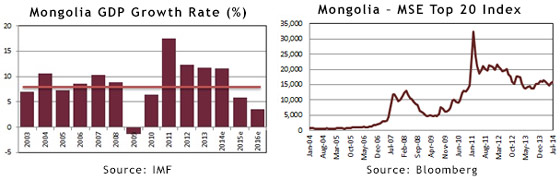

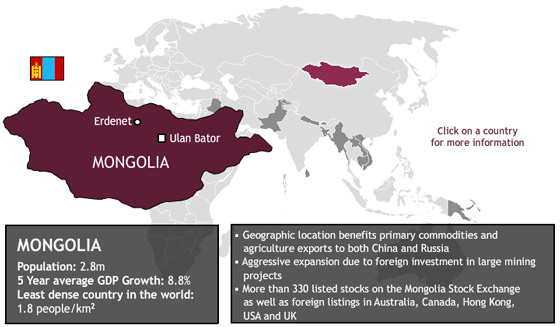

While Ho Chi Minh has made up almost all of its losses from May, Hanoi is still trading almost 15% below the interim high in March. Mid-cap stocks should therefore benefit from a further increase in the second half of this year. Over the last few days we could also observe again the relative independence of Vietnam from major U.S. and European stock markets. The recent sell-off, which dragged some of these markets into a negative overall performance for the year 2014, left Vietnam's stock markets completely unscathed so far. This will most likely continue as long as there is no dramatic sell-off as in 2008. In July the fund's largest positions were: Sam Cuong Material Electrical and Telecom Corp (4.0%) - a manufacturer of electrical and telecom equipment, Gypsum and Cement JSC (2.4%) - a cement company, KLF Joint Venture Global (2.4%) - a real estate development services company, FLC Group JSC (2.4%) - a real estate development company and Dong Nai Port JSC (2.2%) - a port operator. As of 31st July 2014 the portfolio was invested in 70 shares and held 4.4% in cash. The sectors with the largest allocation of assets were consumer goods (34.9%) and industrials (20.9%). The fund's weighted average trailing P/E ratio was 6.61x, the weighted average P/B ratio was 0.97x and the average dividend yield was 7.03%. AFC Country Snapshot: MongoliaAlthough Mongolia is the least densely populated country in the world, with less than 3 million people living in a land area of 1.5 million km², the country has the potential to see the greatest growth of any market within the AFC Asia Frontier Universe. Mongolia's economy is traditionally based on herding and agriculture, but is expanding aggressively due to foreign investments in large mining projects that capitalize on the country's vast deposits of coal, copper, gold, tungsten, tin, nickel, zinc, silver and iron. GDP growth has been under pressure in recent years due to government policies impacting the investment environment, however, the resolution of these issues will likely spur investment in mining and continued economic expansion. Mongolia's growth is steered by high levels of agriculture production, commodity prices and the spillover from China's epic growth.

Stock Market: The Mongolian Stock Exchange (MSE), located in Ulan Bator, was established in 1991 and is the country's sole stock exchange. The MSE lists over 330 companies and has a market capitalization of USD 860 million as of July 2014.

Country snapshots for all of AFC's markets can be found on our website at www.asiafrontiercapital.com AFC Travel Report: MongoliaIn line with our process of being on the ground in the countries we invest in, AFC's Regional Research Analyst, Scott Osheroff, travelled to Mongolia during the month of July to cover the country's development for AFC from the ground. It is easy to forget the role that foreign portfolio investment plays in Mongolia when you first arrive in Ulaanbaatar. If you have your finger on the pulse however you can begin to see the footprint of the stock market around every corner. Looking around you can see cashmere clothing on passersby and evidence of growing consumption which is typical of rapidly growing frontier markets. After peering through the window of a duty free shop in the Ulaanbaatar train station I saw vodka and other products for sale on the way to the night train where I settled into my compartment. As I waited to depart, I contemplated what was happening in the markets that day as the sales of cashmere garments, duty free shop and vodka that I had just passed were all driving revenues of companies listed on the Mongolian stock exchange. At 20:00 we pulled away from the station, remarkably on time, heading west into the sunset. As the train gained speed we passed the ubiquitous ger districts until we broke through into the Mongolian steppe, on our way to Selenge Aimag (Povince) in northern Mongolia for a Naadam vacation. A ger is the traditional tent-like dwelling of nomads in Mongolia that is made from wood and felt. It is made to be easily collapsed and reassembled and is usually transported by horse, camel or yak. These days a ger will also fit nicely on the top of a small four wheel drive. As I saw the sun beginning to disappear beyond the hills from the train window I headed for my own shelter on the top bunk and tucked in for the night. Eight hours later a tap on my shoulder from the train staff was followed by some Mongolian which I was able to decipher as "we have arrived in Sukhbaatar", Selenge's central city. More of a farming town than a city, I proceeded to an unmarked taxi and squeezed in with seven others as we began a ninety minute journey to a village, Tsaagan Nor, where I was to meet my friend and his family for the holiday. Leaving Sukhbaatar at approximately 5am and en route toTsaagan Nor, I witnessed a gorgeous Mongolian sunrise which was a welcoming change to the complete darkness of the steppe. As the sun rose ever higher the darkness gave way to the rolling hills of Selenge and its vast wheat and rapeseed fields. Selenge is regarded as Mongolia's breadbasket and is increasingly being transformed with modern farming practices allowing the country to become a net exporter of grains.

Having arrived at Tsaagan Nor to meet my friend, I was quickly introduced to his family before partaking in the establishment of a motorcade towards his summer home on an 8,000 hectare farm. Meandering our way through countless fields and occasionally losing our way on the wrong dirt tracks, we finally arrived atop a hill overlooking a 100 hectare produce farm my friend calls home during the summer months. I could quickly see why he spends three months per year here, as we were surrounded by open steppe, rolling hills and the Selenge River.

Upon reaching home the Naadam festivities began and a bow and arrow quickly appeared as we took turns shooting, getting better with each arrow. After seeing who had the best shot we proceeded back home and cooked a popular dish, khor khog, which in this case was a sheep whose meat was cooked in the carcass. For those who live a nomadic lifestyle, this method of cooking is highly practical as one needs no stove, but merely hot, glowing, rocks which are put into the animal with the occasional vegetable. Contrary to what you might think, the cooked meat is fall-off-the-bone tender and could easily be served in a Manhattan restaurant as its flavor is rich and delightful. Ironically, the only seasoning is a pinch or two of salt. After our meal evening activities followed suit and everyone then went to bed. The next morning, having a short period in Selenge, I departed my friend's home and proceeded to the Mongolian-Russian border town of Altanbulag where a free trade zone had been inaugurated only weeks before. It was quiet arriving on a Saturday at 10am though Mongolian exporters were busy hawking their wares from cashmere products to spare auto parts. Mongolia has an opportunity to increase trade with neighboring Russia and it will be worth watching how Altanbulag develops in the coming months and years as it is only just gaining its proverbial legs.

Following Altanbulag, before boarding the train back to Ulaanbaatar, I asked my driver to take me west, down a dirt road on the opposite side of Sukhbaatar, where I would be left to my own devices on a short hike. Arriving at the top of a hill after a twenty minute stroll, I found myself overlooking a very special place called Saikhanii Khutul ("beautiful place between the mountains"). This is where the Selenge and Orkhon Rivers intersect before crossing the Russian border as they progress towards Lake Baikal. It was breathtaking, and I spent the next two hours exploring and reflecting as the scale of Mongolia is to the degree of which a camera often has difficulty capturing its beauty. The photos I was able to capture show but a mere glimpse of this great land.

The stereotypical response when a foreigner mentions "Mongolia" being "Chinggis Khan," this elicits visions of an aggressive country and one not worth visiting. On the contrary, spending some time visiting the 18th largest country in the world (also the least densely populated) I wager you will find a romance to it. The kindness of individuals with the warmest hospitality I have ever experienced, coupled with the one-of-a-kind beauty of Mongolia's wide variety of terrain, Mongolia is a hidden gem AFC is proud to be a frequent visitor to, as well as a participant in its phenomenal economic upside. AFC Country Report: MongoliaOnce the darling story for bold investors and mining enthusiasts, Mongolia has struggled in recent years to maintain investor confidence and to capitalize on its enormous resource potential. With a small population of 3 million and lucrative mineral reserves, Mongolia was tipped as possibly becoming the next Qatar or Norway. Enthusiasm for the country has waned, however, as mining giant Rio Tinto has been embroiled in disputes with the Mongolian government over its mega-mine, Oyu Tolgoi. The Oyu Tolgoi project proved to be a litmus test for foreign investors, and frequent changes to legislation and government backtracking spooked many investors. GDP growth has slowed from its record-high of 17.3% in 2011, and the World Bank has lowered its previous forecast for this year from lofty double-digits to an even 10.0%. The dramatic fall in Mongolia's economic outlook has largely been attributed to the compounding effects of dwindling foreign direct investment (FDI) and an overreliance on both the domestic mining sector and on China. Rattled by Rio Tinto's problems in dealing with the Mongolian government and the country's position on foreign ownership of its resources, investors have spurned the country, with FDI decreasing 52% last year and 70% in the first half of 2014. To offset the dramatic decline of FDI, Mongolia has increasingly turned to China, which accounts for 90% of Mongolia's exports and 50% of its imports. Mongolia is in talks with China's Sinopec Group to sign a gas project and supply accord in August to construct two coal-to-gas plants, with 95% of output going to China through pipelines and gas production expected to start in 2019. But China's economic slowdown and recently falling commodity prices have highlighted the danger of being too dependent on one trading partner and one sector - more than 80% of the country's FDI goes into the mining sector. Exports, particularly coal, have fallen in line with China's economy, and Mongolia's earnings from coal exports fell 17% in the first half of the year. China's growth in Q2 2014, however, was higher than expected and an upwardly revised full-year economic forecast for China's economy would bode well for Mongolia. To try and counter an overreliance on China, President Tsakhiagiin Elbegdorj signed a free trade agreement in July with Japanese Prime Minister Shinzo Abe that will cover all of Mongolia's exports to Japan and 96% of Japanese exports. The agreement was also seen as a diplomatic move by Japan, as Mongolia enjoys an unusually close relationship with North Korea that Japan may seek to leverage as it tries to free a number of its citizens that are currently imprisoned by the government in Pyongyang. While Mongolia's political neutrality makes it of strategically importance to Japan, the Ulaanbaatar government is likely keep a close eye on the ongoing events unfolding in Ukraine, which like Mongolia is an independent and democratic former Soviet Union country that shares a land border with Russia. Vladimir Putin's territorial ambitions have likely caught the attention of Mongolia, which has vast resource potential and a small population. On the macroeconomic front, the Mongolian government has pursued expansionary fiscal and monetary policies, which have led to external debt rising to more than 150% of GDP. The expansionary policies have contributed to inflation, and the national currency, the tugrik, has fallen 10% against the dollar this year. Currency reserves have fallen rapidly from USD 2.2 billion at the beginning of the year to USD 1.6 billion in May 2014, in spite of a narrowing current account deficit. The effect of the macroeconomic policy is that Mongolia has received two ratings downgrades this year. In April, Standard & Poor's cut Mongolia's rating from BB- to B+, and in July, Moody's cut its rating to B2, five levels below investment grade. Moving forward, Mongolia needs to take firm action to rebuild confidence among foreign investors to catalyze the strong economic growth it experienced only a few years ago. Small yet encouraging steps have been taken, such as in April when Prime Minister Altankhuyag Norov introduced a "100 day action plan" to promote investment by approving changes to the 2006 Minerals Law and passing a new law on energy. But the "Wolf Economy" must now think from the perspective of damage control, and create effective policies and legislation to nourish the country's economic and business environment back to health. Despite the bearish outlook covered in international media and the slump of the Mongolian Stock Exchange (MSE) Top 20 Index, Mongolia remains an interesting investment story. For one, the MSE Top 20 has not been broadly representative of the overall performance of the country's stock exchange. Many of the largest companies on the MSE by market capitalization, which are part of the MSE Top 20, are poorly-managed state owned enterprises (SOEs). In contrast, there are many small cap stocks of privately-controlled local companies that have posted strong performance. As local brokerage firm BDSec JSC has pointed out, the YTD return of the MSE Top 20 as of July 30th 2014 is -2.3%, but if you instead look at the performance of the top 20 largest privately-controlled companies on the MSE, the YTD return is 21.2%. Although it is a contrarian investment case, Mongolia has many attractive small-cap companies with healthy fundamentals, and the bearish global outlook on the country has led to cheap prices for many of these stocks. In the longer term, we think that the government will take a softer stance in its negotiations with Rio Tinto to try and reassure foreign investors that Mongolia is open for business. After all, Mongolia's GDP is roughly USD 12 billion, while Rio Tinto's market capitalization is USD 107 billion! As the government gradually improves legislation and mining rights and FDI begins to trickle in once again, economic growth should pick up, boosting consumer spending and contributing to solid performance from mining stocks as well as domestic plays in consumer goods, textiles, materials, and hotels. |

||||||||

|

I hope you enjoyed reading our monthly newsletter and remain with kind regards, Thomas Hugger |

|||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||

GO TOP |

|||||||||