Asia Frontier Capital (AFC) - June 2014 Newsletter |

|||||||||||||||||||||||||||||||

In this IssueAFC Asia Frontier AFC Vietnam Fund

|

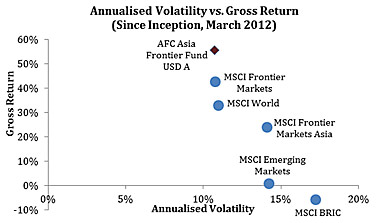

"In investing, what is comfortable is rarely profitable." June has been an incredibly busy month for Asia Frontier Capital, with a major conference in Vietnam, international interviews, and another positive monthly performance by our funds! An increase in capital has bolstered the funds' investment capacity as new investors continue to come on board and existing investors increased their portfolio holdings with AFC. It has not all been smooth sailing in AFC's markets, however, as political uncertainties, unrest, and even violence has filled the news from Pakistan, Iraq, and Vietnam. While we are obviously a proponent of actively managing investments, the need for an on-the-ground approach to research when investing in frontier markets is of paramount importance. Despite recent turmoil in the markets, the AFC Asia Frontier Fund and AFC Vietnam Fund have continued their strong upward movements in 2014 with returns of +0.1% and +1.5% in June. This brings the YTD return to +16.9% and +12.0% for each fund respectively. As a means of comparison, in 2014 YTD the MSCI World Index, MSCI Emerging Markets Index, and MSCI Frontier Markets Asia Index have returned +6.2%, +5.9% and +12.4% respectively. One of the key reasons for this strong ongoing performance - despite temporary hiccups in our markets - has been the investment strategy and unique approach to portfolio allocation that is a core component of AFC's funds. The focus on finding solid companies at attractive prices has helped our funds perform well during rallies and remain defensive during downturns. For illustrative purposes it can be seen in the chart below that this strategy has produced good results for the AFC Asia Frontier Fund since inception on an Annualised Volatility vs. Gross Return basis. As the AFC Vietnam Fund continues to build its track record, we are looking forward to a similarly positive dynamic unfolding.

AFC NewsVietnam Investment Forum - AFC Overview After traveling the globe to visit investors in Europe, USA, Canada, Singapore and Thailand, AFC has stepped up its efforts to draw attention to the opportunities presented by Asia's frontier markets. The Vietnam Investment Forum was a highlight for Asia Frontier Capital, with more than 400 investors, public figures, business leaders, and government representatives turning up to take part in the conference. The conference co-hosts and sponsors, HVS Securities and Vietnam Investment Review, brought everything together, from translation headphones to conference halls, and delivered one of the best catered events AFC has attended in memory. Always known for his unique take on investing, Marc Faber delivered a popular presentation, covering topics including energy security, opportunities and threats from China, Asia's growth potential, and the seemingly inexplicable rise of some of the world's more developed equity markets. While we won't be naming names on which equities were drawn into question, Marc's views on the state of the world since the Global Financial Crisis are quite well reported. He also talked in depth about the difficulty in predicting how the unwinding of global economic stimulus plans will play out and how this uncertainty may potentially impact global markets. Thomas Hugger's presentation on other Asian frontier markets proved to be a point of interest with the crowd later in the day, as a large portion of the attendees were enthusiastic about Vietnam but also looking to learn more about other opportunities in Asia. Some of the other panel discussions proved to be lively debates, which could have been expected given the almost polarizing views on the role of the government between speakers. The event provided a unique opportunity for government leaders in a rapidly growing Communist nation to speak candidly with investors about opportunities for capitalism as a tool to help develop growth. Key points of conversation involved the level of government ownership of companies and restrictions on company ownership limits present in Vietnam. During the discussion, Marc Faber and Andreas Vogelsanger voiced the opinions of many in the crowd by highlighting that while Vietnam offers great opportunities, the administrative hurdles and regulations on foreign investors are overly cumbersome and a significant barrier to attracting international capital. The Vietnamese government looks to be taking slow but steady steps towards a more open economic system, with privatization of government entities contributing to the up and coming swell in equity markets with an average of roughly one IPO per day predicted over the coming 18 months. While it is very unlikely that we will participate in every upcoming listing, there will be ample opportunities presented for investors willing to do their homework over this period. The government in Vietnam is taking steps to attract FDI which we see as a good sign for the future of Vietnam. To see pictures of the Vietnam Investment Forum on AFC's Facebook page, please click here. AFC in the Media

AFC Funds approved in the UK for The Offshore Funds (Tax) Regulations 2009 HM Revenue and Customs has given notice that the AFC Asia Frontier Fund (non-US) and AFC Vietnam Fund have been approved under Regulation 55(1) (a) of The Offshore Funds (Tax) Regulations 2009 with effect from 1 April 2014. This provision is relevant to UK-based investors in our funds and it provides clarity of the treatment of your investment for tax purposes. There is more information available on the regulation available here: http://gabbai.com/law/uk-offshore-funds. If you would like to enquire as to whether this may impact you, please be in touch at Upcoming AFC TravelIf you will be in any of the locations listed below and have an interest in meeting with our team, please contact our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager Comment

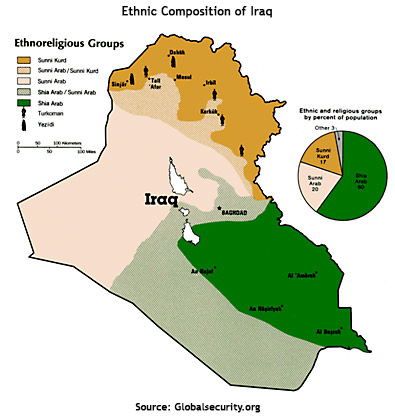

AFC Asia Frontier Fund (AAFF) USD A-shares gained +0.1% in June 2014, outperforming the MSCI Frontier Markets Asia Index (-0.3%) and MSCI Frontier Index (-0.5%) but underperforming the MSCI World Index (+1.6%). The month saw tense activities in some of our markets like Iraq and Pakistan while Bangladesh passed a budget for the new financial year, which was a dampener for retail investors. The Sri Lankan and Vietnamese markets ended in positive territory while the Mongolian market also had a positive performance after three months of negative returns. The best performing indices within the AAFF universe in May were Mongolia (+4.6%), followed by Vietnam (+2.9%) and Sri Lanka (+1.8%). The poorest performing indices were Iraq (-13.9%) and Pakistan (-0.3%). Iraq has been in the news in the past month due to the spillover of the Syria conflict into northwestern Iraq. The Islamic State of Iraq and Syria, better known as ISIS or ISIL (Islamic State of Iraq and the Levant) has continued to make inroads into central and northwestern Iraq ever since making its impact felt in the beginning of the year when the group took control of parts of Anbar province in January. Without getting into the complexities of the history of the region, Iraq has three major regional/religious segments, namely Shia Arabs, Sunni Arabs, and Kurds. The Shias are the majority in terms of size of population as well as in the government in Baghdad, and the Sunnis feel marginalized by government policies made in Baghdad. At present, Shias make up a large part of southern Iraq, Kurds control northeastern Iraq and Sunnis are spread across northwestern Iraq. (refer to ethnic map below) With Syria being governed by a Shia Arab and the majority of the population being Sunni, who are against the current power structure in the country, the uprising which has taken place in Syria over the past few years has played a role in strengthening the base of ISIL in northern Syria. With ISIL gaining strength in northern Syria and being a pro Sunni group, it was not surprising to see the group make inroads into Iraq given the Sunni population's resentment towards Baghdad. Therefore, what we have is resentful populations in both Syria and Iraq, a powerful militant group in ISIS which is pro-Sunni, and a polarizing Prime Minister in Baghdad which has ultimately led to instability in Iraq. The current reach of ISIL spreads from Nineveh province in the northwest to Anbar province in central/western Iraq. Going forward, this conflict has the possibility of carving out Iraq into three ethnic regions with Iraqi Kurdistan in the northeast (which is already present), a Sunni region in western and northwest Iraq and a Shia region in the south which includes Baghdad.

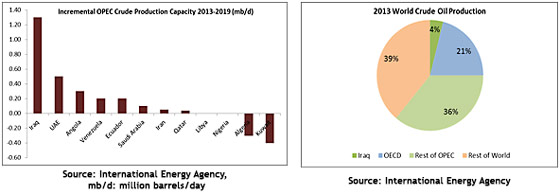

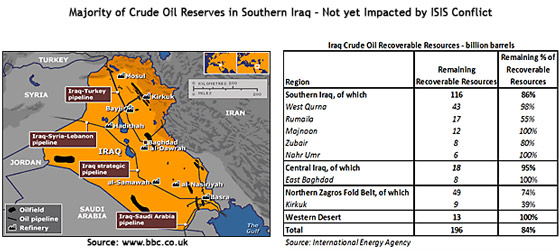

What can the possible impact of these events be? One of the biggest concerns for global investors has been the impact of this conflict on Iraq's oil exports/reserves. At present, a majority of oil exports as well as oil reserves are in the south of Iraq which has so far not been affected by the conflict. The possibility of the south being impacted is low given that the region south of Baghdad is Shia dominated which would mean there would likely be more resistance if ISIS tries to make its way towards Baghdad and the south. Time will tell if there will be resistance but more importantly, the U.S. comes into play given the importance of oil assets in the south and it is unlikely that that the US would want to give up strategic leverage in Iraq to Iran or another power, given that Iran is a supporter of the Shia-led government in Baghdad. Another point to consider is that Iraq's neighbors in the region (i.e. Saudi Arabia, even though it is Sunni dominated (similar to ISIS)) would not want ISIS to become more powerful in the region than it already is given the group's agenda of being anti-state. With the conflict is showing no clear signs of abating, Brent Crude prices shot up in June to USD 115.71/barrel. With the conflict being restricted to northwestern and western Iraq and the possibility of the conflict reaching the South not high, Brent crude prices fell a bit to close at USD 112.25/barrel, which is still 14% higher than the April-June quarter of 2013. Iraq is expected to be the leading contributor to increased output within OPEC in the next decade, therefore the continuation of the conflict may not lead to a significant correction in oil prices in the near term even if the unrest does not reach southern Iraq.

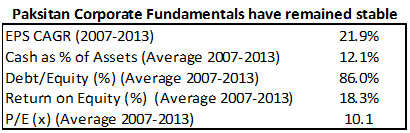

The ISIS situation has ironically played out well for the autonomous Iraqi Kurdistan region. The conflict has strengthened Kurds' leverage over the central government in Baghdad given that the Kurds now control Kirkuk, a town that possesses the second biggest oil field in Iraq which exports oil via Turkey through the Kirkuk-Ceyhan pipeline (although this pipeline has not been in operation since March 2014 due to the ongoing security issues). The Kirkuk oil field is quite old, however, and has much lower reserves than the fields in the south. The current situation will also make the Kurds push for further autonomy with respect to their own oil exports without interference or revenue sharing with the Iraqi government in Baghdad. We shall see how this situation pans out for the Kurds but it appears they do have more leverage and this is a positive for the Kurdistan region. The fund has an investment in a Canadian listed junior oil play with an oil project in Kurdistan. This stock was up 3.5% in June. The ongoing conflict is not a good sign for the Iraqi economy and the possibility of it ending in the near term appears low. Having said that, the market discounts the future and with the Iraqi market down 14% in June any further downside from here could present opportunities assuming the future is that the current situation will not escalate and that Iraqis will be able to bring back some sort of stability to the country. We will be watching the situation very closely. At present, the fund does not have a significant exposure to the country with 4.4% of assets invested in Iraq. This month also saw the Pakistan military launch major operations against the Taliban, who have built up a base in the tribal areas of the country in the northwest bordering Afghanistan. There was talk of an offensive for a while but the Karachi airport incident in early June was the triggering point for the launch of this operation. The current operation is taking place in North Waziristan, which forms part of the Federally Administered Tribal Areas. This is not the first operation launched by the Pakistani military against the Taliban within its borders. There have been more than a few military operations in this region but with a new government led by pro-business Nawaz Sharif, as well as Army and civilian government backing, there seems to be more conviction in the government's actions. The operation should last for about 3-4 months and if it helps in significantly reducing Taliban presence in the border regions, this would be a positive for the economy and the market as well. Permanently eliminating this threat in the short term may be a long shot given the porous border between Pakistan and Afghanistan and the fact that Afghanistan security forces are still not well equipped to manage an insurgency. Though this military operation has received a lot of publicity in the media, the fundamentals of Pakistani companies remain strong and the current operation, like previous ones, is taking place in the border regions which are a fair distance from the economically significant hubs of Karachi and Lahore. Repercussions in major cities could be a possibility but the current security situation is not something that is new to investors and even during prior military operations there was no significant fall out which negatively impacted companies' fundamentals. Over the past 6 years, which includes the 2007-2009 period that saw both the financial crisis as well as multiple military operations, earnings growth of Pakistani companies have grown at a CAGR of 21.9% between 2007-2013, balance sheets have been healthy with cash as % of assets at 12.1% on average and leverage levels are not significantly high with average debt/equity levels at 86%. RoE's have also been consistent with an average of 18.3% between 2007-2013. Furthermore, the P/E of the KSE100 Index is currently at 8.4x based on 2014 earnings and has averaged 10.1x between 2007-2013 which reflects the current situation on the ground to an extent. We therefore feel that any negative sentiment over the military operation would be a great opportunity to pick up stocks given the value proposition that the Pakistan market offers.

The Bangladesh market also had some important developments during the month as the Finance Ministry tabled the annual budget for the upcoming financial year July-June. The budget proposed introducing a capital gains tax for domestic high net worth investors and also proposed rolling back tax rebates for companies that pay out 20% of paid up capital as a cash dividend. Since Bangladesh is a predominantly domestic retail driven market, these proposals led to profit taking before the beginning of the new financial year and impacted sentiment. Interestingly, due to the negative fallout of the proposed measures these proposals were rolled back on the day when the annual budget was passed in Parliament on 29th June. This should see retail investors coming back to the market and sentiment should become more positive. In Vietnam, worries over China's claim to the waters surrounding the Paracel Islands in the South China Sea continued as the Chinese moved another oil rig off into "disputed" waters. The Vietnamese market has stabilized since the first oil rig incident occurred in May and though worries remain over the future outlook the fact that talks have begun between both sides could lead to future stability. Furthermore, given the developing nature of Vietnam's economy relative to China, and Vietnam's attraction to foreign investors with respect to manufacturing activity, the authorities will hopefully keep in mind the negative fallout of the long, drawn out protests and violence that occurred in May. The Vietnamese Central Bank also devalued the currency by 1% during the month which was likely done to help maintain export growth. Overall, it was a challenging month given the many moving parts but the fund did manage to have some good individual stock performances which helped manage returns relative to the index. The top-performing portfolio stocks were a Bangladeshi holding company (+39.2%), followed by a Vietnamese equipment producer (+17.5%), a Mongolian gold mining company (+16.1%), a Vietnamese telecom equipment producer (+15.0%), and a Vietnamese gas distributor (+14.9%). In June we added to existing positions in Cambodia, Iraq, Laos, Mongolia, Pakistan, Sri Lanka and Vietnam and we reduced three holdings in Vietnam. We sold the entire position of a Vietnamese confectionary company as well as a Mongolian construction material company. As of 30th June 2014, the portfolio was invested in 117 shares, 1 closed-end fund (with 19.9% discount to NAV), 1 GDR (with 50% discount) and held 8.3% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.2%) and a bank in Laos (3.0%). The countries with the largest asset allocation include Vietnam (20.1%), Pakistan (18.3%) and Bangladesh (13.0%). The sectors with the largest allocation of assets are consumer goods (36.8%) and materials (14.8%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 15.87x, the weighted average P/B ratio was 1.58x and the dividend yield was 4.55%. AFC Vietnam Fund - Manager Comment"Vietnamese work hard and they have ambitions. Investors To review this manager comment in German please click here. In June 2014 the AFC Vietnam Fund returned +1.5% which was an underperformance versus the VN Index and VH Index which returned +2.9% and +2.8% respectively. This month was one of the quietest in recent times. Declining stock market volumes and low volatility, despite ongoing political tensions with China, confirm our view that investors slowly but surely return to business as usual. Meanwhile more Chinese oil rigs were set up in the disputed territory and it looks like international courts will be eventually involved with this conflict. In a few years' time we will probably see countless oil rigs in the South China Sea, and it will only be a matter of which nationalities will control and operate the oil exploration. Increasing reports about privatizations are dominating the local business news. In addition to Vietnam Airlines and Vinatex, a leading textile company whose IPO will take place in the coming weeks/months, some further 500 privatizations of companies are planned by the end of 2015, which equates to roughly one IPO per day. To what extent this can realistically be done successfully remains to be seen. Many IPO's have no participation of foreign investors, since prospectuses are normally in Vietnamese only and also the attractiveness and profitability of the companies is often unsatisfactory. In addition to that, there is this peculiarity in Vietnam that the time of the IPO announcement and the first trading day takes between several months and a year, instead of the usual 3-14 days like in most countries. Our participation in IPO's will therefore be very selective until the market condition for public offerings is more favourable. Before the start of the Q2 reporting season, the devaluation of the Vietnamese Dong and the forthcoming privatizations were the main topic of the month. As pre-announced a few months ago the Vietnamese Dong was devalued in June by 1% to around 21'300 VND to 1 USD in order to meet the demand of the export economy. As mentioned last month, currency movements of that magnitude are on the open foreign exchange market normal daily movements. The fund valuation however is affected directly by this, even though the prices of shares in the export sector didn't react to this news. On the other hand the indices in Ho Chi Minh and Hanoi, which are obviously calculated in Vietnamese Dong, increased during June. After the fund showed a significant outperformance in the previous month, this months' difference to the indices is mainly due to the devaluation and once again due to the increase of a few large index weighted shares. Even on days where the indices closed in positive territory there often was a negative market breath by a wide margin. We hold approximately 10% of all listed shares, and hence on such days there is no way to make any money. Most likely the main reason is the still cautious attitude of the Vietnamese investors who have not yet returned to the stock market due to uncertainties with China. Meanwhile foreign investors pumped new money into the market and concentrated their purchases on a handful of stocks. However, over the last few days we were seeing more interest from local investors in some smaller companies. This fact combined with an attractive chart technical situation further increases our confidence for the coming months. Here is an example of one of our investments in the field of infrastructure/housing, which is trading well below book value, although the company has been able to increase sales and profits by 50% in the difficult last three years and has a dividend yield of 10% and a price/earnings ratio of around 5x.

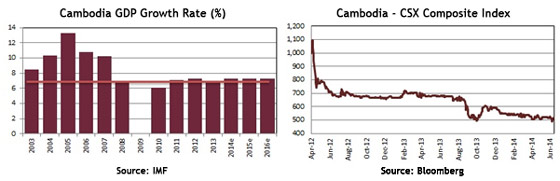

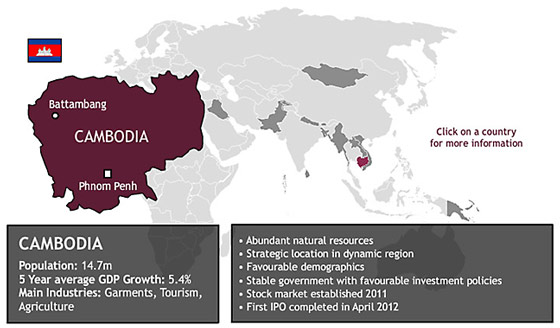

If the second quarter earnings results are again positive, we then could see small- and mid-caps rally very sharply since most of them are still trading between 20% to 40% below their March peaks. Generally the mood remains very positive and, as confirmed on the recent Vietnam Investment Forum in Ho Chi Minh, the consensus opinion is that Vietnam is very well positioned to be among the long-term beneficiaries in the region. In June the fund's largest positions were: Sam Cuong Material Electrical and Telecom Corp (4.4%) - a manufacturer of electrical and telecom equipment, KLF Joint Venture Global (2.6%) - a real estate development services company, Gypsum and Cement JSC (2.6%) - a cement company, FLC Group JSC (2.5%) - a real estate development company and Bentre Aqua Product Import & Export (2.4%) - a seafood exporter. As of 30th June 2014 the portfolio was invested in 67 shares and held 1.6% in cash. The sectors with the largest allocation of assets were consumer goods (37.7%) and industrials (20.6%). The fund's weighted average trailing P/E ratio was 6.64x, the weighted average P/B ratio was 0.95x and the average dividend yield was 6.98%. AFC Country Snapshot: CambodiaAfter decades of political mismanagement and civil war, Cambodia has recently begun to capitalize on its economic potential. Since adopting free-market economic policies in the 1990's and increasing its integration within the international community, Cambodia's economy has flourished. From 1998 to 2007, Cambodia's GDP growth ranked sixth in the world (9.8%) and fastest in the Far East after China. Cambodia's continued upward trajectory will be driven by several factors. Cambodia is resource-rich with newfound offshore oil and gas deposits in the Gulf of Thailand and mineral deposits in the northern provinces. Tourism is also growing quickly, as Cambodia is home to pristine beaches, world-class cultural relics (Angkor Wat) and a burgeoning eco-tourism sector. Cambodia also benefits from a young and cheap workforce, and a growing middle-class.

Stock Market: The Cambodia Securities Exchange (CSX) was established in July of 2011 and is headquartered in Phnom Penh. The CSX held its first IPO of state-owned Phnom Penh Water Authority on 18 April 2012. The CSX finalized its second listing on the 16th June 2014 with garment manufacturer Grand Twins International completing its IPO. The market capitalization for the CSX was USD 195 million as of 30th June 2014.

Country snapshots for all of AFC's markets can be found on our website at www.asiafrontiercapital.com AFC Travel Report: CambodiaIn line with our process of being on the ground in the countries we invest in, AFC's Regional Research Analyst, Scott Osheroff, discusses the development of Cambodia and its rural economic growth. On 19th June 2014 Asia Frontier Capital co-hosted the Vietnam Investment Conference in Ho Chi Minh City Vietnam. Spending roughly nine months per year in Phnom Penh, Cambodia, I always leap at the opportunity to venture into the countryside to assess the rural economy, where the majority of Cambodia's 15 million inhabitants live. So, rather than taking a plane to HCMC I opted for the overland route to see just how quickly Cambodia's provinces are growing. Travelling on the roads in Cambodia is always an adventure and the first step is clearing Phnom Penh's incredible traffic. During my first trip to the Kingdom in 2012 traffic was hardly noticeable; now the streets are clogged with used Mercedes, Range Rovers and a plethora of other vehicles, providing a clear indication that there is a small, yet burgeoning middle class. After forty minutes en-route I had cleared the Monivong Bridge on National Road One and was moving into Kandal Province, one of three I passed through to the border. Upon reaching the edge of Phnom Penh the scenery transition was abrupt. Shop houses and small foundries turned to rice paddies of a gorgeous shade of green, the likes of which I have only encountered in Southeast Asia. As the rainy season had set in the flooded fields and beginning of the rice planting season made for a stunning view.

Two hours in, having passed countless farms and the occasional dwelling, we came to an abrupt stop at the Mekong River. Cambodia not well known for boasting modern infrastructure, most of which has fallen into a state of disrepair over the past several decades, there is no bridge spanning the river. Therefore, we proceeded to the ferry to make our journey across. Waiting in line to board the boat, hawkers of all sorts were peddling their goods. Once on board I took the opportunity to stretch my legs to interact with the locals, hoping this time they would have fried tarantulas on offer. With a dusting of chicken seasoning and a texture like soft shell crab they are an ever-so tasty snack for the road. Though I am sure our 8 legged friends are not everybody's cup of tea I suspect few would be able to identify the origins of the flavoursome treat they were eating if it were presented to them with their eyes closed. This part of Cambodia will soon be moving faster as the river crossing is about to get sped up with the completion of a USD 131 million world-class bridge being built by the Japanese. It is expected to be completed in 2015. The new bridge will expedite the transportation of goods and people leading to lower transit costs leading to a profound effect on growth as National Road Number One is the main road to Vietnam.

Once across the river we continued onward to Svay Rieng, a province bordering Vietnam. Driving through Svay Rieng has always been an interesting part of the journey for its downtown boasts a small square with farming statues and an eerie stillness which is reminiscent of scenes of small Mexican villages in the movie The Good, the Bad and the Ugly. As Cambodia's rural economic development continues it is not uncommon to see new buildings pop up. The latest addition was at the far end of the town square where a new Acleda Bank branch had nearly arrived. Acleda is Cambodia's largest commercial bank and last month announced that it would re-invest USD 39 million in corporate profits into branch expansion. The bank was founded to service Cambodians living in the provinces and in Svay Rieng I passed three branches under construction and several others already adding clients in a largely unbanked country. This increased access to credit is expected to aid growth in the region as farmers mechanize and individuals seek modern forms of transit. The demand for credit was evident as I passed downtown on the final kilometers to Bavet. Bavet is the industrial heartland of the Province, where two SEZ's, the Manhattan and Tai Seng SEZ's sit virtually across the street from one-another. There is an additional two dozen other projects under construction in the vicinity. With relatively inexpensive electricity provided by Vietnam the region is ideal for energy intensive industries which also need access to HCMC's port. This mini factory boom has not only stimulated the local economy, but has led to a swelling of the local population as regional Cambodians flock to Svay Rieng's factories in search of stable employment. Thus, it made sense to see several real estate projects involving the build out of shop houses, villas and commercial properties on the highway well underway. I was surprised however by just how quickly this construction was occurring for it was non-existent during my last journey on this road, one year prior.

Having grown up in California I have always been enamored with how border towns can exist in stark contrast to one another across an imaginary line. Bavet being no different, on the Cambodian side, driving towards the border I came across bustling casinos, karaoke parlors and a few non-descript, but bustling local coffee shops. And one cannot forget the pothole laden roads which are falling into increasing disrepair. The Vietnamese side however was quite the opposite. Having cleared immigration we began the home stretch to HCMC. Vietnam is described by some as being ten years more advanced than Cambodia, and every time I take this journey and cross the border it is easy to observe the future of Cambodia's provinces. While at first glance the Vietnamese side doesn't seem much different, a closer look yields larger buildings which are better constructed, newer and nicer cars in the driveways, more grandiose villas, and a relatively pothole-free road with sound infrastructure to mitigate flooding. Smaller items such as the clothes for sale and those being worn by locals are also of a better quality leading to the sense of poverty being less obvious. Cambodia has a long way to go in its economic upswing and signs of mean reversion between Vietnam's countryside and Phnom Penh are well under way. Previously minimalist countryside dwellings, these are slowly giving way to modern shop houses interspersed with luxurious accommodations. The occasional larger motorcycle speeds by, as does a new car and the quality of life seems to be improving as well, leading to more disposable income and a more stable existence. Cambodia's rapid economic growth of 7.2% in 2013, reported by the ADB, is expected to continue, leading to greater advancement in Cambodia's provinces and move towards greater equality with the middle class of Phnom Penh. AFC Country Report: Cambodia2014 has been a tumultuous year for Cambodia's garment industry, a mainstay of the economy that accounts for over 80% of exports and employs over 600,000 people, 90% of whom are women. On January 3rd, government forces opened fire on striking garment workers, killing five and injuring dozens more. The heavy-handed response received international media coverage and condemnation from human rights groups and from apparel companies that rely on Cambodian garment factories for production. The source of the unrest was a call by garment labor unions to increase the minimum wage to USD 160. The government finally settled on a new minimum wage of USD 100, which the unions have thus far not accepted. Cambodia's heavy reliance on its garment industry remains a questionable move from an economic standpoint. The garment industry flourishes on cheap wages and the industry's razor-thin margins mean that manufacturers have an incentive to move production to cheaper countries like Myanmar or Bangladesh as Cambodian wages rise. At the same time, however, the industry is a key foreign exchange earner for Cambodia and has provided income and employment for many of the country's rural residents who have traditionally been under-employed. The January 2014 walk-out of workers cost the country's garment industry an estimated USD 300 million from the sudden halt in production, and global clothing and retail giants Levi Strauss and Target have both announced their intentions to scale back production and sourcing from Cambodia as a response to the unrest that has occurred this year. To try and dispel the notions that the industry remains in turmoil, the Cambodian government is working with the World Bank and the International Labor Organization to reach a consensus on what is a fair minimum wage for the sector. To add fuel to the fire, the strikes among garment workers have become increasingly politically-charged, citing the country's growing income inequality and building on the momentum of the political demonstrations by the opposition that occurred after the July 2013 national elections. Despite the unrest, which began in December of last year, the garment sector grew 20% in 2013 to USD 5.5 billion, even with a 54% increase in the number of "labor days lost" in 2013 due to the December protests which continued into the New Year. Garment exports to the US were up 7.6% YoY and exports to the European Union were up 28% YoY. Against the backdrop of growth in the garment sector and the simmering unrest, Grand Twins International (GTI), a Taiwanese-owned garment manufacturer that produces clothes for Adidas, decided to pursue an Initial Public Offering on the Cambodian Securities Exchange (CSX) in June, becoming only the second traded stock on the exchange after Phnom Penh Water Supply Authority (PPWSA) listed in April 2012. GTI shares began trading in June, receiving a lackluster response from investors in comparison with PPWSA's successful flotation. The less-than-stellar demand from investors was attributed to the continued uncertainty of the garment sector, as many disputed issues remain unresolved. GTI sold 8 million shares (20% of the company) and raised USD 19.3 million, less than the USD 28 million the company had initially targeted. The capital raised will fund new factories and GTI's expansion plans. The IPO date was pushed back numerous times due to delays in receiving necessary regulatory approval. The CSX has been unable to attract other companies in Cambodia to list on the exchange, and some potentially-interested businesses are reportedly waiting until the bourse increases its market capitalization and gains liquidity before they proceed with IPO plans. To encourage more companies to go public, the CSX may need to work in conjunction with the Cambodian government to offer regulatory incentives and tax advantages to spur growth in the country's capital markets. A lack of confidence in the Cambodian Securities Exchange will be a difficult problem to fix without upgrades in securities regulations and resolved technical issues. Some observers also wonder whether many of the local business groups would agree to the financial transparency that going public would entail, given that Cambodia is a country still plagued by corruption, with a large disparity between the rural poor and the business and political elite. One testament to the growing income inequality in Cambodia is that Rolls Royce, the luxury British carmaker, recently announced plans to open a showroom in Phnom Penh, despite the fact that the average income per capita in the country is only USD 950. Tourism has been another strong contributor to the economy - in 2013, Cambodia received 4.2 million tourist arrivals, representing a 17.5% increase over the previous year. Overall revenue from the tourism sector rose to USD 2.5 billion in 2013, a 15% increase YoY. Siem Reap Airport, Cambodia's busiest and the gateway to Angkor Wat, will undergo a USD 1 billion passenger terminal upgrade beginning in August 2014 that is expected to double the airport's capacity to 15 million passengers. The political unrest in neighboring Thailand has also affected Cambodia in recent weeks. New regulations imposed by the Thai junta aiming to crack down on illegal migrant workers in Thailand lead to the mass exodus of over 250,000 Cambodian migrant workers in late June. The influx of migrant workers into Cambodia has created significant challenges for both Cambodia and Thailand. Cambodia is trying to cope with the logistical task of handling the sudden return of more than 1.5% of its entire population. Thailand, on the other hand, will no doubt feel the effects of a shortage of manpower in its construction industry - it is estimated that more than half of construction workers in Thailand are from Myanmar and Cambodia. Thai factories and ports have also complained of the effects of a labor shortage and are anticipating delays in shipping delivery times and decreases in factory output. To address the problem, Cambodia is trying to lower passport costs and expand passport processing centers in Thailand to help many of the migrant workers return to Thailand to work legally. Many rural Cambodians depend on remittance inflows from migrant workers in Thailand, where wages are higher and employment is easier to find. The events have complicated relations between Cambodia and Thailand. Cambodia's longstanding Prime Minister, Hun Sen, has close ties with exiled former Thai Prime Minister Thaksin Shinawatra and Cambodia was rumored to be a potential asylum base for Thaksin in the aftermath of Thailand's coup earlier this year. Hun Sen, however, was quick to play down such rumors and has not granted asylum to Thaksin. A quick resolution to this mass exodus of Cambodian migrant workers is in the best interest of both countries. Cambodia doesn't have the economic resources to deal with a sudden influx of over 250,000 people, and Thailand's economy will certainly contract without the necessary workforce for its key labor-intensive industries such as construction, seafood, and manufacturing. Although this year has seen its share of uncertainties with regards to the garment sector and Cambodian migrant workers in Thailand, Cambodia continues to register strong economic performance, with the Asian Development Bank expecting that GDP growth will rise from 7.2% in 2013 to 7.5% in 2014, primarily driven by an expansion in exports (primarily garments), tourism, agriculture, and construction. |

||||||||||||||||||||||||||||||

|

I hope you enjoyed reading our monthly newsletter and remain with kind regards, Thomas Hugger |

|||||||||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||||||||

Source: Asia Frontier Capital and Bloomberg

Source: Asia Frontier Capital and Bloomberg

Source: Bloomberg

Source: Bloomberg

Border Casinos in Bavet

Border Casinos in Bavet