Asia Frontier Capital (AFC) - April 2014 Newsletter |

|||||||||||||||||||||||||||||||||||||||||||||

In this IssueAFC Asia AFC Vietnam AFC Fund

|

"The only source of knowledge is experience." This month at AFC has seen international travel, news, awards and the announcement of a major conference. Alongside the exciting upcoming events, our funds have witnessed interesting developments in a number of key markets which we discuss in this month's manager comments. April also saw a strong inflow of new capital as new investors came on board and existing investors increased their existing holdings. So far in 2014 the AFC Asia Frontier Fund has returned +13.8% YTD and the AFC Vietnam Fund has returned +10.7%. AFC NewsAFC to host Marc Faber at Vietnam Investment Forum on 19th June 2014 In conjunction with HVS Vietnam Securities and Vietnam Investment Review, Asia Frontier Capital is very pleased to announce that we will be hosting the Vietnam Investment Forum in Ho Chi Minh City, Vietnam on 19th June 2014. The topic of the conference is 'The Rise of Frontier Markets and Opportunities for Vietnam' and guest speakers featured include renowned contrarian investor Marc Faber, alongside AFC's Thomas Hugger and Andreas Vogelsanger. For more information on this exciting event please visit http://vietnaminvestmentforum.vn/en/ or click here to see the forum brochure. There is a limited number of tickets available to our existing and potential investors who may wish to attend. If you may have an interest please direct any enquiries to AFC's Marketing Director Stephen Friel at AFC Wins Fund Awards As we enter the 2014 fund awards season, we are very pleased to announce that Asia Frontier Capital has been recognized with awards from international finance magazines Acquisition International and ACQ5. This follows AFC's preceding award for fund launch of the year after Thomas Hugger's MBO of the AFC Asia Frontier Fund in 2013 (click here). We are of course very pleased to be recognized in our industry and will continue to work hard to bring you not only great investment performance but also the personal level of service that we pride ourselves on as a boutique fund.

AFC Expands Research Team - Scott Osheroff, Regional Research Analyst

AFC's Andreas Vogelsanger in the News In April, Marc Djandji of ASEAN Investor caught up with Andreas Vogelsanger to discuss the outlook and drivers of Asian Frontier Markets as well as different ways to invest in these rapidly growing markets. You can read the full interview online (click here). Kh. Asadul Islam Steps Down as Director We would like to thank Kh. Asadul Islam (Ripon) for all of his service and wish him all the best for the future after stepping down from his role as a Director at Asia Frontier Capital and AFC Asia Frontier Fund. Ripon has stepped down for personal reasons and this has not impacted the Asia Frontier Capital team, other directors or the continued development of AFC's funds. Upcoming AFC TravelIn the next few months AFC's team will be travelling the world to meet with new and existing investors. If you will be in any of the below locations and have an interest in meeting with our funds team do be in touch with our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager CommentAFC Asia Frontier Fund (AAFF) USD A-shares gained +1.5% in April 2014 bringing the total YTD performance to +13.8%. The fund outperformed the MSCI World Index (+0.8%) whilst underperformed against the MSCI Frontier Markets Asia Index (+2.8%) and the MSCI Frontier Index (+5.4%), which both saw a significant rally. April also saw a significant inflow of new funds from individual as well as institutional investors who have invested in AAFF for the first time. The best performing indices within the AAFF universe in April were Pakistan (+6.5%), followed by Sri Lanka (+4.3%) and Iraq (+3.0%). AAFF outperformed the index in Sri Lanka, as some of our relatively undervalued consumer names appreciated. Whilst our holdings in Pakistan were in positive territory (+4.4%), we were slightly behind the index. The few companies we hold in Iraq (-1.3%) trailed the index where there was some uncertainty due to the elections held at the end of April. The star performance for country-specific stocks in the AAFF was in Bangladesh where the portfolio holdings (+10.2%) significantly outperformed the index (+1.7%), as our healthcare and consumer stocks rallied in anticipation of good quarterly results. The poorest-performing country indices were in Hanoi/Vietnam (-10.7%) and Mongolia (-4.8%). The AAFF portfolio stocks held up well in the face of significant downturns in these markets, retreating only -1.3% in Vietnam and -2.6% in Mongolia. There has been profit taking after the Vietnamese market has run up over the past few months, but the inclusion of small and midcap names in the portfolio helped amid the downturn. In Mongolia, our consumer names performed relatively well against the overall market. The top-performing portfolio stocks were two Bangladeshi pharmaceutical companies (+36.2% and +30.9%), followed by a Bangladeshi shoe chain (+30.4%), a Pakistani health care company (+24.5%) and a Pakistani insurance company (+23.1%). In April we added to existing positions in Laos, Mongolia, Pakistan, Sri Lanka and Vietnam. We sold one Sri Lankan tile company and a Pakistani consumer good company. We bought the Pakistani company exactly one year ago at 80 Rupees and sold it this month at a 16x the purchase price. When we sold the company it was trading at a trailing P/E of 102x. We also participated in an IPO of a Mongolian concrete producer - the first IPO in Mongolia in nearly 2 years. As of 30th April 2014, the portfolio was invested in 120 shares, 1 closed-end fund (with 20.1% discount to NAV), 1 GDR (with 55.2% discount) and held 8.6% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.5%) and a junior copper mine in Mongolia (4.0%). The countries with the largest asset allocation include Vietnam (19.6%), Pakistan (16.4%) and Bangladesh (16.2%). The sectors with the largest allocation of assets are consumer goods (37.6%) and materials (14.2%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 14.54x, the weighted average P/B ratio was 1.51x and the dividend yield was 4.18%. AFC Vietnam Fund - Manager CommentThis month AFC Vietnam Fund's (AVF) CIO, Andreas Karall has gone the extra mile and translated the AVF manager comment into German (click here). This month AVF saw an influx of new capital from investors looking to take advantage of the long term opportunities offered by the Vietnamese market. As suspected last month, the consolidation period progressed further and even accelerated since mid-April leading to an April return of -4.6% for AVF. Within only six trading days, the Ho Chi Minh index lost 7% and the Hanoi index 10% to end the month down -10.7% and -2.3% respectively. Even though some of the blue chips in Ho Chi Minh were able to recover in the last few days, the indices remained in negative territory during the month of April. The chart below shows the price movements of the more volatile Hanoi index:

It is interesting to observe that our fund showed a much higher correlation with the Ho Chi Minh index, although about two-thirds of our shares are listed in Hanoi. We are very much dependent on a broad increase in Vietnamese stocks, since our portfolio consists of about 10% of the total shares listed in Vietnam. Hence a short term rebound of some Ho Chi Minh listed large caps has little effect on our fund, as the following chart of the Ho Chi Minh index illustrates:

If we however extend the observation period from 2.5 years to 8 years, then you will clearly see how insignificant the movements of the past few months were, putting it into context with a longer time horizon. It actually shows what opportunities exist in the long term in Vietnam, assuming that our positive view over the coming years will be confirmed:

The focus of our investment strategy is geared towards the long-term development of fundamentally undervalued companies and therefore the business development of those companies is much more important. Meanwhile, around 70% of our holdings have released their results for the first quarter and, with a few exceptions, the financial numbers were in line with (or even above) our expectations. We still expect that all of the 65 companies we are invested in will be profitable in 2014. Most likely the major part of the correction is now behind us and we feel much more positive about the market than we did one month ago. In April the fund's largest positions were: Sam Cuong Material Electrical and Telecom Corp (4.4%) - a manufacturer of electrical and telecom equipment, VICEM Gypsum and Cement (2.9%) - a cement company, FLC Group JSC (2.6%) - a real estate development company, Bentre Aqua Product Import & Export (2.4%) - a seafood exporter and Pharmedic Pharmaceutical Medicinal JSC (2.3%)- a specialist pharmaceutical company. As of 30th April 2014 the portfolio was invested in 65 shares and held 3.8% in cash. The sectors with the largest allocation of assets were consumer goods (36.4%) and industrials (18.7%). The fund's weighted average trailing P/E ratio was 6.97x, the weighted average P/B ratio was 0.96x and the average dividend yield was 6.93%. One example of the numerous investment opportunities in the Vietnamese stock market is the sugar industry. The agricultural sector of Vietnam is still one of the major pillars of the country. Over the last decade, stocks from this sector were among the favourite topics of analysts and investors worldwide. With the onset of the economic crisis and the price decline of most commodities, many investors lost interest. Despite this, food production remains an important topic given the ever-growing world population and the increasing prosperity and consumption of developing countries. The end of declining commodity prices does not necessarily mean that prices will bounce back strongly in the short-term, although we saw price increases in cocoa and coffee of 50% and 100% in recent months. Prices for oats, corn, and soybeans are also already well above their recent lows. We therefore see good long-term investment opportunities in food production companies. In contrast to the increasingly unpopular speculation in commodities, the share capital of the company is the fundamental basis for an increase in the production of food. After three years of price declines in sugar prices, there finally seems to be a price stabilisation. What would happen with company earnings assuming that prices only recover towards the USD 20 or 25 level?

Vietnamese sugar companies are still profitable and we see some insider buying in these companies over the last few months. Using the example of one of the leading sugar companies (SBT), a clear relationship between sales/operating profit and sugar prices over the past few years can be observed:

Sugar consumption is increasing rapidly, especially in developing countries. In Thailand, the consumption quintupled over the past 40 years. The consumption increase in Asia as a whole is about 5% annually (currently around 23kg per capita), which is the same level of the U.S. more than 100 years ago!

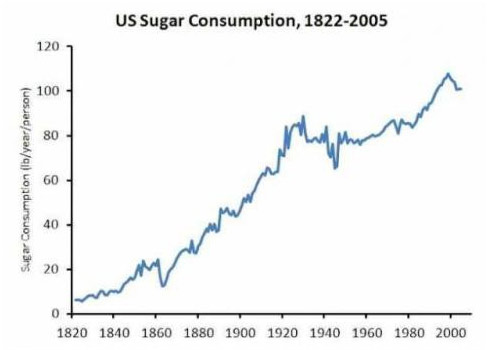

Source: www.sucden.com

Source: Dr. Stephan Guyenet, US Department of Agriculture, Economic Research Service There are numerous listed Vietnamese sugar companies. Their price/earnings ratios based on 2013 numbers are between 5x and 10x. Some of the companies are trading 20% below their book values and the dividend yields are around 8-12%. Depending on whether the price of sugar has now stabilized and whether the company operates efficiently, dividend cuts are unlikely. Company valuations might fall further in the first half of this year, but will then most likely stabilize. Because of the cheap valuations and the sharp profit drop due to lower margins over the last few years, these companies will have large upside potential in the future if sugar prices recover. The balance sheets are generally very good and shouldn't cause any sleepless nights. Of course these are all long-term thoughts and will not necessarily results in short term gains if the market rallies, but it demonstrates what kind of investment strategies are possible in Vietnam. A few days ago the third largest sugar company in Thailand was listed on the stock exchange. While Vietnam's sugar companies are valued at 5x to 10x earnings, this Thai sugar company managed to place its shares at an astonishing 30x earnings! As an agricultural nation and top 3 exporter of rice, coffee and rubber, Vietnam's sugar production ranks "only" at position 21 in the world, but certainly has the potential for further growth if the sugar market situation should change again. Looking ahead to May there have been some tensions develop in the South China Sea (click here) which has seen pressure on the markets as some investors that fear the worst and have begun some panic selling. Whilst geopolitics and the rise of China will no doubt influence market sentiment in the Asia region the factors driving the long term potential of Vietnam remain unchanged. Should a further panic take hold of investors as regional powers rattle their sabers this will provide an excellent opportunity for the fund to accumulate positions in strong companies that draw the majority of their revenues from the domestic Vietnamese market. We look forward to updating you on the latest developments in next month's newsletter. AFC Country Snapshot: VietnamSince the introduction of market reforms that opened up the country to foreign investment in the late 1980s, Vietnam has become one of the fastest-growing economies in the world, averaging annual GDP growth rates of 7-8% throughout the nineties. Agribusiness production has nearly doubled over the past two decades, transforming Vietnam into one of the world's largest exporters of rice and shrimp. Currently, Vietnam is in the midst of a transformation from a manual labor/agrarian-based economy towards one fueled by skilled- labor. Agriculture production has decreased 5% to account for 20% of GDP over the last five years, while the government has begun to provide incentives for hi-tech companies -- such as Intel, Canon, and Samsung -- to bring skilled manufacturing jobs to Vietnam.

Stock Market: Vietnam hosts two large stock exchanges; the Ho Chi Minh City Stock Exchange (HOSE), Vietnam's largest stock exchange, and the Hanoi Stock Exchange (HNX). Established in 2000, HOSE currently lists 301 companies and has a market capitalization of US$ 44.7 billion and a P/E ratio 13.9x of as of February 2014. The HNX hosts 377 companies and has a market capitalization of US$ 5.5 billion as of February 2014.

Country snapshots for all of AFC's markets can be found by clicking on the map above and are available on our website www.asiafrontiercapital.com AFC Travel Report: VietnamIn line with our process of being on the ground in the countries we invest in, Chief Investment Officer of the AFC Vietnam Fund, Andreas Karall and Senior Investment Analyst of the AFC Asia Frontier Fund, Ruchir Desai travelled to Vietnam to attend the Viet Capital Investor Conference held in Ho Chi Minh City. It is always nice to go back to Ho Chi Minh City (HCMC). The place is bustling, has a good amount of history and enables one to actually feel the potential which Vietnam offers. Similar to my previous trip in August 2013, I flew on the state-owned Vietnam Airlines from Hong Kong. The airline is supposedly looking at an IPO sometime this year as the government looks to pare down its stake in various state owned entities. Since Vietnam is a pretty big tourist destination in Asia, getting through immigration and getting hold of transport via a private taxi is not an issue and is pretty organised. There are multiple private taxi operators lined up outside the terminal but I prefer to take the Vinasun taxi. They are clean and dependable and easy to get hold of not only at the airport but anywhere in HCMC. The other reason I choose to take Vinasun's taxis is because the company is publicly listed, is part of our portfolio and travelling in their taxis helps in doing some real on-the-ground research! The airport is not too far from downtown HCMC so getting to my hotel did not take more than 30 minutes but traffic in the city is similar to that of any developing city - chaotic. As usual, lots of two wheelers but also lots of cars too. In HCMC, there are dozens of hotels to choose from besides the five star ones. Vietnam gets more than 7 million tourists a year so getting hold of decent accommodation and places to check out or eat out is not a problem at all. A suggestion for good Vietnamese food is Ngon on Pasteur Street or Pho 2000 right next to the Ben Thanh market which is a bit more local but quick and cheap (and Bill Clinton ate here back in 2000). Walking around District 1 (downtown HCMC) is quite comfortable with walkways shaded by trees and major tourists spots walking distance from one another. (Presidential Palace, War Museum, Notre Dame Cathedral, and Saigon Post Office). The next morning, getting to the conference in morning rush hour traffic took about 10-15 minutes even though it was very close to where we were staying. Walking would have been better instead but the heat at this time of year in Vietnam is pretty sapping! The investor conference, held at the InterContinental, was a great platform to meet with management teams of various companies and also to hear what people on the ground had to say about the country and its economy. The conference was very well attended by institutional investors and there were a few investors looking at Vietnam for the first time or visiting the first time. Clearly, Vietnam has caught the fancy of investors and this is reflected in the run up of the VN index and investor participation at the conference. During the conference, we were fortunate to get quite a few small group meetings with company management teams given the heavy participation in the conference. This gave us the chance to ask more questions as compared to being in an open presentation and therefore allowed us to get a better grip on the future prospects of the company. The companies we met with in small group meetings were from diverse industries such as technology, healthcare, transportation, oil & gas and real estate. Of these meetings, the company which we liked the most was a technology company. It has a leadership position in the Vietnam technology market but it also has over the past few years developed into providing IT outsourcing services to clients, especially in Japan. With Vietnam offering a low cost talent pool with a background in computer engineering/software engineering it would not be surprising to see Vietnam's IT outsourcing exports grow in the coming years. The other companies of interest were a healthcare company which focused on manufacturing and distribution of herbal and traditional medicines. It has a leading position in the Vietnam market and differentiates itself from the other players due to its product offerings which are not the generic over-the-counter products that other companies offer. In the oil & gas industry we met with a state owned drilling rig operator which has a dominant position in the Vietnam oil drilling market due to its close relationship with the state owned oil company, Petro Vietnam. The real estate company we met with is a leading player in the affordable housing segment and has developed some good projects in HCMC and the transportation company we met was involved in logistics and operating ports but is investing in some unrelated businesses. What was common across all these meetings was that management teams were quite open in sharing details about their company's business, the market potential, their strategy and future outlook. They were open to taking on uncomfortable questions linked to investing or strategy decisions as well and communication was not much of an issue. At times investors ask us if speaking with company management teams is an issue because not everyone speaks English at the management level. The answer is yes and no. For the above meetings all the management teams spoke English and there was not much of an issue getting ideas across. With smaller companies it could be an issue but there is usually a translator who does a pretty good job. The translator is usually a sell side analyst. Besides these meetings which we attended, the conference also had various speakers one of whom was the Chairman of McDonalds Vietnam. McDonalds began operations in Vietnam just a few months ago in February 2014 and if reports are true, the chain served 400,000 customers within the first month of operations! The menu has some additions to it in order to cater to Vietnamese tastes such as the "Double McPork" which would cost about USD 3. With average monthly income in Vietnam at USD 150 it is not surprising that so many people are turning up at the counter as eating at McDonalds is a pretty big deal for the average Vietnamese. I remember when McDonalds first came to India in the late nineties there was an equal amount of clamour to get hold of a McDonald's burger! Even today in India, families which are beginning to earn more view eating at McDonalds as a new experience and you will not see too many empty outlets. It will not be surprising to see a similar trend in Vietnam and how good this is for the Vietnamese population's health, time will tell. The two days of meetings and guest speakers' talks at the conference went very well and we wrapped up with a pleasant evening at a location overlooking downtown HCMC. Night view of Ho Chi Minh City and Ben Thanh Market

Besides attending the conference, we also took a few days out to meet with companies that are part of the portfolio of the AFC Vietnam Fund and the AFC Asia Frontier Fund. Getting out of conference mode also is a good way to get a feel of the country/city instead of sitting in five star hotel conference rooms. Typical Street View - Ho Chi Minh City

None of the meetings that we attended was in the Central Business District (District 1) and getting into other parts of the city was a good way to check out other parts of the city on the ground. Our first meeting of the day took place at an industrial park about 45 minutes from the central business district. The industrial park has been done up in an organised manner and with good paved roads. Also, whilst traveling to the industrial park we took one of the newer highways that has been built in an around HCMC. The thrust on infrastructure development is evident and there are also plans to develop a metro in the city with construction of the metro already beginning in Hanoi. Industrial Park in Ho Chi Minh City

The first company we met was a copper/optic fibre company which supplies cables to the telecom industry and its management team had its head on the ground which is a good sign. The chairman of the company was kind enough to show us around his factory and talk about the future plans for the company. Capacity at the company is expected to increase in the coming year and it would not be surprising to see higher growth rates from this company in the coming few years. The next two companies we met were both state owned with one of them manufacturing tobacco packaging for the domestic tobacco industry and the other a manufacturer and distributor of consumer electronics. At both these companies, we met with the CFOs and considering that these are smaller companies the level of openness and knowledge of the business was as good as many of the companies we met during the conference. The tobacco company expects to increase capacity in the North of Vietnam and the fact that it is backed by a state owned tobacco producer provides the company stability in terms of recurring business. The consumer electronics company we met was doing a lot of things such as karaoke systems, white goods and audio systems. It would be interesting to see how things pan out for this company given that big consumer players like LG, Sony etc. have already entered the market in Vietnam. On the last day, we met with two other companies. A taxi operator which was discussed in the earlier part of this report and an agricultural seed producer/distributor. We met with CFO of the taxi operator which currently has close to 50% of the HCMC market and plans to enter in newer cities later this year and in 2015. Going to their offices gave us a chance to look at their customer service operations as well which function through a call centre in the same building. Our last meeting was with the CFO of the agricultural seed producer and distributor whose main products are corn, rice and vegetable seeds. It is a leading supplier in Vietnam and a trusted brand which does research on new products and is planning to expand capacity for one of its product lines. What was common in these five companies that we met are they are run by good management teams, no flashy offices and businesses that are simple, cash generating and not heavily levered. Additionally these are the companies that are ignored by most institutional investors which allow us to find value. The P/Est of all the five companies we met post conference are less than 10x. Overall, this was a very fruitful trip as we got the opportunity to meet with both, portfolio companies as well as companies which the fund does not hold but finds interesting at the right valuation. We were satisfied with the progress and future plans of our portfolio companies and more importantly these companies are still trading at a discount to the overall market in spite of their future growth potential! We will continue to track the developments of our companies both on and off the ground and will report back after our next trip to Vietnam!) Vietnam Travel Report:

|

||||||||||||||||||||||||||||||||||||||||||||

|

I hope you enjoyed reading our monthly newsletter and remain with kind regards, Thomas Hugger |

|||||||||||||||||||||||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||||||||||||||||||||||

The black spots in the sand dunes are - you guess it - plastic bags!

The black spots in the sand dunes are - you guess it - plastic bags!