Asia Frontier Capital (AFC) - May 2014 Newsletter |

|||||||||||||||||||||||||

In this IssueAFC Asia AFC Vietnam AFC Travel Report: Fund

|

"I will tell you how to become rich. The end of May 2014 marks a very important milestone for Asia Frontier Capital as we have officially passed the one year mark as an independent fund company. Since the first day of operations after the MBO 12 months ago AFC has seen dramatic growth in both scale and scope with a doubling of fund products offered, more than tripling of our team headcount and an increase in AUM of more than 6 times! Though AFC is a niche operator in the fund world if the AUM growth rate continues at this pace AFC could be on track to hit our soft close in the next 18 months - but there is a great deal of work to be done before then! With a dedicated focus on public equities AFC has been producing great performance with the AFC Asia Frontier Fund seeing a return of +16.8% YTD and a total of +30.8% since inception. The fund's focus on being overweight markets that have a more stable macroeconomic outlook and finding good undervalued companies has seen this performance maintain a lower monthly volatility profile than the MSCI World and MSCI Emerging Markets and incredibly low correlation with global market indices. This month is also the 1 year anniversary of the announcement of tapering in the US which has seen the correlation of our fund become negative against the MSCI World Index, MSCI Emerging Markets Index and MSCI BRIC Index. You can revisit Thomas' CNBC interview from June 2013 on frontier and emerging markets outflows after tapering by clicking on this link. The AFC Vietnam Fund also continues to impress with a 13.0% return since inception in December 2013, despite the dramatic turn in markets over the past month. Even with the largest single day drop in Vietnamese shares in history happening on the 8th of May 2014 the fund held its ground to return -0.3% this month whilst the VH and VN Indices fell -5.1% and -2.8% respectively. This represents a net outperformance of both the VN and VH Indices since its launch less than six months ago. Be sure to read this month's AFC Vietnam Manager comment for a more detailed look into the Vietnamese market. We would like to take this opportunity to welcome all of our new investors who have come on board this month. We would also like to thank all of our investors since AFC's inception for their continued support as we continue to bring you returns from Asia's investment frontier! AFC NewsAFC to host Marc Faber at Vietnam Investment Forum on 19th June 2014 In conjunction with HVS Vietnam Securities and Vietnam Investment Review, Asia Frontier Capital is very pleased to announce that we will be hosting the Vietnam Investment Forum in Ho Chi Minh City, Vietnam on 19th June 2014. The topic of the conference is 'The Rise of Frontier Markets and Opportunities for Vietnam' and guest speakers featured include renowned contrarian investor Marc Faber, alongside AFC's Thomas Hugger and Andreas Vogelsanger. For more information on this exciting event please visit http://vietnaminvestmentforum.vn/en/ or click here to see the forum brochure. There is a limited number of tickets available to our existing and potential investors who may wish to attend. If you may have an interest please direct any enquiries to AFC's Marketing Director Stephen Friel at AFC in the Media This was a big month for AFC in the press with a feature on the AFC Asia Frontier Fund in Marc Faber's Gloom, Boom & Doom Report and Thomas Hugger crossing media paths with Jim Rogers to weigh in on frontier market investing. All of this month's media is available via the links below and also on our website at http://www.asiafrontiercapital.com/news/latest-news.html

Upcoming AFC TravelIn the next few months, AFC's team will be traveling around the world to meet with potential and current investors. If you will be in any of the locations listed below and have an interest in meeting with our funds team please contact our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager Comment

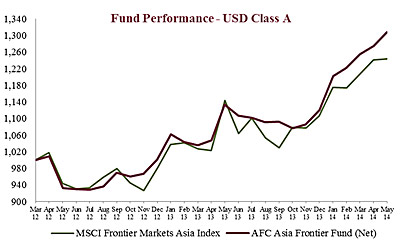

AFC Asia Frontier Fund (AAFF) USD A-shares gained +2.6% in May 2014, outperforming the MSCI Frontier Markets Asia Index (+0.2%), the MSCI World Index (+1.6%) and underperforming MSCI Frontier Index (+5.4%). The MSCI Frontier Index has seen a strong rally in the past few months which has continued after the announcement on May 14 that Qatar and United Arab Emirates would be moved up into the MSCI Emerging Markets Index. This reshuffle is somewhat unsurprising as it reflects the more advanced nature of these economies with GDP per capita in these markets being USD 89,800 and USD 65,600 respectively as of December 2013. Consequently 13 stocks will be added and 30 deleted from the MSCI Frontier Index. Among the three largest additions two of the companies are from Pakistan (Pakistan Tobacco Company and K-Electric) and 23 of the deletions obviously come from Qatar and the United Arab Emirates. The best performing indexes within the AAFF universe in May were Pakistan (+2.9%), followed by Laos (+1.0%) and Sri Lanka (+0.6%). Pakistan has continued with its strong performance over the past 18 months and has been benefiting from the increase in weight allocated after the changes to the MSCI Frontier Index. The poorest performing markets were Hanoi/Vietnam (-5.1%) and Mongolia (-4.6%). The most significant market moving event in our country universe this month stemmed from the naval tension in the South China Sea after China moved an oil drilling rig into waters disputed by Vietnam. Alongside a panic sell off the event has triggered nationalist outcries from both sides and anti-Chinese sentiment in Vietnam. Both sides of this dispute have a great deal more to lose than gain from its escalation so we are hopeful that cool heads and good policies will prevail. China has had multiple international incidents on this issue with other countries in South East Asia related to claims over disputed waters in the region. There is more coverage of this issue specifically in the AFC Vietnam Fund Manager comment below. Mongolia has also seen a slide with continued pressure on the stock market with the Oyu Tolgoi (which is 66% owned by Rio Tinto) issue still remaining unresolved which has kept the mine from fully developing its production capacity. Continued issues with Mongolia's Balance of Payments have seen pressure on the local currency continue but a solution to the Oyu Tolgoi dispute should spur output as well as growth and lead to an increase in FDI which could address both of these issues. This should represent a good buying opportunity in Mongolian equities for companies we find attractive and good stock selection has helped AFC's Mongolia portfolio perform well. The top-performing portfolio stocks were a Pakistani beverage company (+73.1%), followed by a Pakistani TV network (+50.6%), a Mongolian bakery (+41.6%), an Iraqi oil producer (+32.2%) and a Vietnamese food processing company (+27.8%). In May we added to existing positions in Bangladesh, Iraq, Laos, Mongolia, Pakistan, Sri Lanka and Vietnam and reduced the holding in a Pakistani beverage company. We sold the entire positions of a Bangladeshi pharmaceutical company, shares and warrants of a Cambodian infrastructure company and also of a Vietnamese infrastructure company. We added three new stocks to the portfolio: a Pakistani denim producer, a Vietnamese light bulb manufacturer and a Cambodian casino operator which we exited exactly a year ago and now bought back. As of 31st May 2014, the portfolio was invested in 119 shares, 1 closed-end fund (with 19.9% discount to NAV), 1 GDR (with 50% discount) and held 8.1% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.9%) and a junior copper mine in Mongolia (3.3%). The countries with the largest asset allocation include Vietnam (20.1%), Pakistan (19.0%) and Bangladesh (14.1%). The sectors with the largest allocation of assets are consumer goods (37.1%) and materials (15.2%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 14.98x, the weighted average P/B ratio was 1.53x and the dividend yield was 4.43%. AFC Vietnam Fund - Manager CommentTo review this manager comment in German please click here. May 2014 the AFC Vietnam Fund returned -0.3% for a total of +10.3% YTD. Last month we experienced the largest one day stock market loss in the still relatively young market history of Vietnam, which was triggered by the Paracel Islands incident between Chinese ships and the Vietnamese Coast Guard in the South China Sea. The positioning of the Chinese oil rig HYSY981 was clearly perceived as a provocation, since Vietnam this area as their territory. On May 8, the two indices lost 5.87% and 6.40% respectively and there were 30 stocks up against 500 stocks down, the majority of the losers closed limit down. In our special report shortly after this incident, we informed our customers about this very special situation and referred to the chances of a speedy recovery. Due to the panic reaction of Vietnamese investors the Ho Chi Minh and Hanoi indices lost from the high in March 17% and 26% respectively. During that period we saw massive inflows from foreign investors who were net sellers before. Does this mean foreigners are the smarter investors? Generally, I would clearly deny this, but foreign institutional investors have experienced these kind of political situations in other markets over and over again, were Vietnamese retail investors who only invest in their home market were put in fear and panic. The strong recovery that began in the second half of May couldn't fully make up the losses and the Ho Chi Minh and Hanoi indices ended the month down 2.8 % and 5.1% respectively. As already mentioned before, we hope that during correction phases our fund won't suffer as much as the market. As seen in the graph below, this was also the case this time. At the low point of the recent crash the annual stock market gain was erased completely, whereby our fund lost 6% in the low and closed the month almost unchanged. There were a lot of corporate actions and dividend payments this month. The Vietnamese Dong was slightly weaker (-0.5%) which also affected the NAV in USD. Our European investors won't be impressed with such a currency movement of 0.5% in 1 month, since they are experiencing these kind of movements in EUR/USD in a matter of a few hours regularly. If we look at the EUR/VND (Euro versus Vietnamese Dong) movements of +/- 2% in 2014 seems relatively low, and the Vietnamese Dong has even slightly appreciated versus the Euro since December last year.

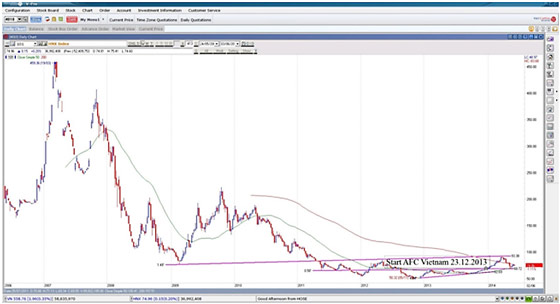

The Vietnamese government tried to settle this conflict through diplomatic channels, but as it looks now they will probably file a lawsuit against China in the hope that they can put them under pressure. Also completely unexpected by both sides were the Vietnamese rioters which looted or destroyed factories of primarily Chinese and Taiwanese companies. Meanwhile there are more and more international voices which suggest that China should be prepared for a compromise and participate in constructive discussions in order to calm the situation. In addition to Vietnam there are also Japan, the Philippines and Taiwan involved in the conflict with China and the increasing political isolation of China cannot be in the interests of this economic giant. However, as we have seen from other major nations again and again and also today, is often to use such a foreign policy to distract from domestic political problems and weaknesses, but often the main reason has to do with massive oil and gas deposits in the region. The theme will probably haunt us for a little bit longer, but often investors will take less and less interest in it and the daily routines and life will take over and the only negative economic impact on Vietnam is the risk of smaller foreign direct investments. But the Vietnamese government is reacting quickly in offering some companies tax incentives. Originally, we were expecting a longer consolidation period, but the recent crash should have completed the correction. After a short pause we will probably see the return of Vietnamese investors, which will primarily benefit our small caps. As the long-term chart below clearly shows, the investment rational has not changed:

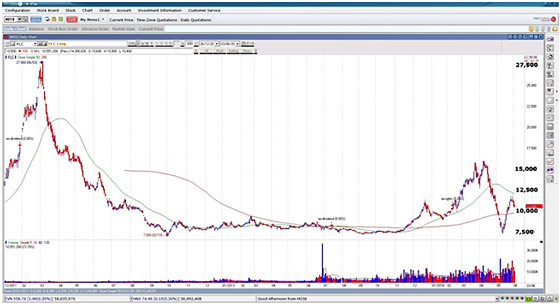

Our assessment is therefore again very positive and with the generally quite good corporate results of our holdings we expect a prosperous second half year. As in last month's edition, we want to demonstrate with a concrete example of one of our holdings, the enormous upside potential of individual stocks and sectors in Vietnam. This month highlighted company is FLC, our fourth largest position. This real estate company is listed on the stock exchange since October 2011 and was in recent months the most actively traded stock in Vietnam. In 2010 the sales of this company were at less than USD 2 million and the profit was at USD 0.3 million; sales and profits multiplied over the past few years and are stood at the end of 2013 at USD 82 million and USD 4.7 million respectively. In order to keep the balance sheet healthy and to finance growth, the capital has massively increased. Meanwhile the market capitalization is around USD 100 million and the enormous growth continues as well in 2014. In the first quarter of this year, sales increased by 70% and the profit multiplied to almost 2 million. According to a statement of management a few days ago, the profit target of the first half of the year alone is at USD 7 million compared with USD 4.7 million for the whole year of 2013. From today's perspective I expect their full year 2014 profit to be at USD 15 to 20 million. The dividend yield of 2013 was at 4% and for 2014 it is expected to be at 10% (!). Despite these impressive numbers, we are currently believed to be the largest foreign investor. Although FLC no longer belongs to the small cap segment and is now almost as big as the firms that are currently included in the index, brokerage houses and international investors are managing to ignore this jewel very successfully. Today for example, only 25,000 shares out of 10.5 million shares of FLC were traded by foreigners. With further growth in this company, an inclusion in the stock market index can be expected. With only 1.8% of foreign shareholders, FLC could become a very popular blue chip if the economic development continues to remain positive. The chart below shows the volatile development of the stock price - as opposed to the overall market, where foreign purchases counter steered to the panic selling of the Vietnamese retail investors, the price of FLC dropped within a few weeks 50%. During the crash we increased our position significantly and our average purchase price is now under 10,000 Vietnamese Dong.

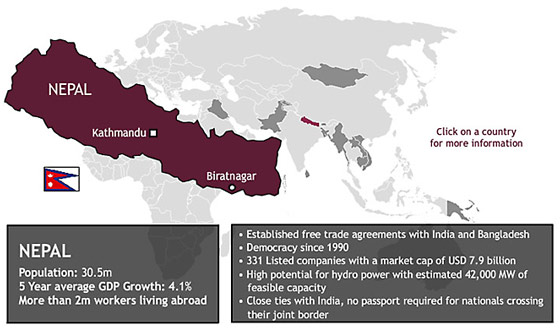

It is also worth noting that, FLC is not the only position in our fund which has this sort of profile! AFC Country Snapshot: NepalAfter ten years of civil war between the government and Maoist rebels ended in 2006, Nepal is looking to shed its violent past and provide its citizens with political stability and economic growth. In the foreseeable future, economic growth will largely depend on the government's ability to exploit the country's hydroelectric power potential, which could provide electricity to energy hungry neighbors in the subcontinent, including India and Bangladesh. Additional natural resources consist of quartz, timber, copper, cobalt and iron ore. Increased agricultural production, which amounts to one-third of GDP and employs 75% of the work force, will also be a crucial element for any near-term economic growth. Nepal's inchoate tourism industry also has potential to spur economic growth.

Stock Market:

Country snapshots for all of AFC's markets can be found by clicking on the map above and are available on our website www.asiafrontiercapital.com AFC Travel Report: Nepal - Exploring Chaotic KathmanduIn line with our process of being on the ground in the countries we invest in, AFC's Contributing Writer, John Enos, travelled to Nepal at the end of April to cover the country's development from the ground. The visa line on arrival at Kathmandu's Tribhuvan International Airport is a telling sign of the chaos that is omnipresent in Nepal's capital. Hundreds of foreigners and Nepalis were shuffling, pushing, and waiting for the customs officers to return from their tea break and resume stamping passports. Luckily I'd be warned about the long wait and made a beeline for the closest looking immigration official who had a working visa stamp and looked ready to let us in to the country. We had arranged for our hotel to pick us up from the airport, and by the time we got our bags, it was nearly 10 pm. Entering the city and navigating its labyrinthine alleys was all the more difficult at night given that Kathmandu was almost completely pitch black. Our driver told us that Kathmandu's electricity supply has been stretched far beyond its means, and the city has been strictly rationed to a "loadshedding schedule", meaning that large swathes of the city are without power for 12-16 hours a day! I suppose that explained why the few merchants closing up shop at 10 pm were having conversation and one final cup of tea by candlelight. I had heard of Pakistan's ongoing problems with power cuts, but hadn't been prepared for Nepal to have similar challenges, especially given its aggressive push towards developing the country's hydropower sector. We woke up early the next morning and drank a large pot of sugary, milky Nepali tea to get ready for a full day of wandering Kathmandu's chaotic streets. Our first stop was Durbar Square, a UNESCO World Heritage Site that was once the ruling epicenter for the Kings of the Kathmandu Valley and features all sorts of spectacular buildings and relics from the 17th and 18th centuries. Many of the buildings have intricate carvings and anywhere we looked we could see a marbled elephant or royal lion staring down at us from the crossbeam or roof overhang of a temple.

As it was Nepali New Year when we visited in April, the Durbar Square was bustling in anticipation of the holiday's upcoming festivities - flowers being sold, fried honey momos - Nepalese dumplings - were peddled by street vendors, and crowds gathering round for a traditional Nepali ceremony with elegant singers and enchanting drums.

Walking back to our hotel after a full day at Durbar Square, we wandered the congested streets of Thamel, which is the main backpacker and tourist bazaar, housing hundreds of shops offering, amongst other things, prayer flags, yak milk soap, pashmina and cashmere scarves, and "authentic" North Face and Columbia trekking gear. We were quite overwhelmed by the selection of goods for sale and how well-targeted the items were to the myriad of tourists passing through Nepal every day. Despite the abundance of shops selling goods aimed at tourists, the Thamel neighborhood still felt authentic; as soon as you took one turn off of the main drag, you'd find yourself lost in another dusty lane chock full of Nepali merchants selling motorcycle parts, henna dyes, and "Nepaliwood" films to local Nepali shoppers. Strolling the maze of Kathmandu was a great way to spend our first day and get a feel of life on the ground in Nepal, seeing the sights that the city had to offer and sampling the local culinary specialties (buffalo-meat dumplings and Tibetan chhaang (millet beer) served warm, anyone?) The only drawback was the level of dust and pollution in the city. Air pollution levels have gotten far worse in recent years due to the increasing number of cars on the road. Nepal's air quality recently ranked 177th out of 178 countries, according to Yale's 2014 Environmental Performance Index (EPI), and during peak traffic, the level of small particulate matter can reach 20 times the World Health Organisation's safe upper limit! Needless to say, we soon recognized the necessity of wrapping scarves around our faces to serve as de facto smog masks.

On the second afternoon, to get out of the traffic and get a view of the Kathmandu Valley, we ventured up to Swayambhunath, an ancient religious complex towering over the city and also known as the "Monkey Temple". I've learned far too often living in Asia that monkeys, in reality, are far from the cute little animals in movies and are usually cheeky little pests that pull your hair and snatch your snacks right from your hands. We kept a close eye on the wild packs of monkeys jumping from temple to tree, waiting for opportune moments to steal a camera or a cookie from unsuspecting tourists.

Swayambhunath is reportedly one of the most sacred Buddhist pilgrimage sites, and I can see why. Once we finally surmounted the climb to the top of the temple (365 steps…thank god I'm not a smoker), we were graced with breathtaking views of the city and scores of Buddhist pilgrims walking clockwise around the stupa while local monks looked on and Nepali prayers were recited. Perhaps the experience felt surreal because I was short of oxygen, but it was definitely an entrancing scene.

Leaving Kathmandu, we headed to Bhaktapur, an ancient Newar town in the Kathmandu Valley with an equally astonishing Durbar Square, before taking a terrifying 8-hour busride on the edge of the Himalayas to Pokhara, Nepal's lakeside town famous for its adventure sports that often draws comparisons to Swiss Alpine towns. Despite queasy stomachs that kept us bed-ridden for a few days, we still managed to try out whitewater rafting and paragliding. I must say, standing on the edge of a cliff with a questionably-durable parachute strapped behind me and a chain-smoking French adrenaline junkie instructing me to "run as fast as you can off the mountain" made me wonder at the last minute whether paragliding in a developing country was such a bright idea, but it ended up being incredible and worth the risk for the world-class views. I highly recommend it to anyone who wants a sense of what it would be like if humans could fly.

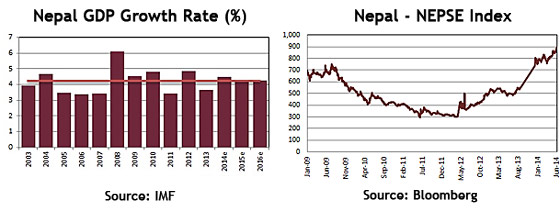

10 days in Nepal felt too short, and many of the travelers we met were there for much longer, with ambitious treks planned for the Annapurna Circuit or Everest Base Camp. The duration of the trip did allow us to experience the enchanting allure of Nepal and it was easy to see why so many tourists keep coming back. Tourism is a key sector of the Nepali economy, and we saw all types of visitors, from Korean families to Austrian mountaineers to dreadlocked young backpackers attempting to recreate the Hippie Trail of the '60s. But Nepalis are quickly catching on to the rise of Asia's disposable income - we met loads of tourists from China, Thailand, and Malaysia. One moment in particular summarized the extent of globalization's reach today. While shopping in a customized leather store, my girlfriend and I noticed that a Chinese couple was speaking to the shopkeeper in Chinese and pointing at us. We were amazed to learn that the shopkeeper, who was Pakistani, was fluent in Mandarin (as well as English, Urdu, Nepali, and some French), and he translated for us, saying that the Chinese couple thought we looked sharp in the leather jackets and that similar merchandise would be far more expensive in Beijing. What a situation - a Pakistani leather trader translating Mandarin to English for his Chinese and American customers in Kathmandu. The spirit of travel and trade is clearly alive and well! Nepal is well-suited to handle travelers of every variety, and the hospitality and warmth of the Nepali people ensured the trip was hassle-free. If you're looking for an adventurous getaway to a country that feels different from anywhere I've ever been, I'd highly recommend taking a closer look at Nepal. AFC Country Report: NepalIn line with focusing on a country from AFC's investment universe in each month's newsletter this month we cover Nepal to discuss its economy and future prospects. Nepal is best known as an alluring tourism destination, boasting 8 of the 10 highest mountains in the world. The small, landlocked country bordering India and China is home to nearly 28 million people and is the most rural country in South Asia, with 80% of its citizens living in rural areas. The country is rapidly urbanizing, however, as evidenced by Kathmandu becoming increasingly crippled by pollution and gridlock - an overpopulated city stretched well beyond its means. Nepal remains desperately poor, and with an average annual income of USD 646, it is in the poorest 10% of countries in the world according to the IMF. The country's GDP stands at just under US $19 billion, and GDP growth has remained relatively low in comparison with the region, hovering around 3-4% per year, although it increased to 4.9% in 2012. Nepal became only the second Least Developed Country (LDC) after Cambodia to gain entry to the World Trade Organization in 2004. As a landlocked, mountainous nation, Nepal is heavily reliant on India for its seaport access, and India is the country's largest trading partner, accounting for over 55% of its trade. The Nepali Rupee is pegged to the Indian Rupee at 1.6 NPR/INR, and has suffered from the depreciation that recently afflicted India in the aftermath of the Fed's tapering of quantitative easing. Historically, Nepal has had closer ties with India than China, but the new Maoist leadership has gotten cozier with China as Beijing has increasingly discussed financing large hydropower projects and road construction to help alleviate the country's desperate power shortages. China, however, still keeps a close eye on the Sino-Nepali border due to its ongoing tensions with Tibet. The country has struggled to attract substantial foreign direct investment, especially in comparison to other countries in South and Southeast Asia, and a number of challenges exist. Repatriating capital or withdrawing investments requires foreign investors to receive central bank permission and selling Nepali currency requires letters of credit. State monopolies control the electricity distribution and petroleum sectors, and a number of sectors are still closed or restricted for foreign investors. The Nepal Stock Exchange (NEPSE) is effectively off limits to foreign investors, although NEPSE signed an agreement with Bloomberg in March to internationalize the stock market and take steps towards attracting interest from foreign investors. India has been the largest source of foreign investment in Nepal, and many Indian companies are moving towards expansion in the country, especially due to the fixed currency peg that eliminates foreign exchange risk for Nepali subsidiaries. There is also free flow of labor (an open border) between India and Nepal, and many cultural similarities in terms of marketing Indian goods towards Nepali consumers. Other top countries for FDI in Nepal include China, the US, and South Korea, with energy being the largest sector. Remittances from Nepalis working overseas have been a vital contributor to the Nepali economy and have become quite a contentious topic in recent years. More than 2.2 million Nepalis are estimated to work abroad, primarily in India, UAE, Saudi Arabia, Qatar, and Malaysia, and it is reported that nearly 1,500 Nepalis migrate abroad for work every day, primarily working on construction sites and in factories. The sheer impact of remittance inflows in Nepal is massive. Inflows grew 14% YoY to US $4.8 billion in 2012, according to the World Bank, and were estimated to reach US $5.21 billion in 2013. Nepal has the third highest level of remittances as a percentage of GDP after Tajikistan and Kyrgyzstan, accounting for 25% of GDP. The inflow of remittances has assisted in the economic development of Nepal and has helped reduce poverty, shore up foreign exchange reserves, and expand local banks and financial institutions. The news has not all been rosy, however. Numerous advocacy groups and human rights organizations have shed light on the poor overseas working conditions for Nepali migrant laborers, and a recent piece by The Guardian estimated that 185 Nepali migrant workers had died in 2013 alone working on World Cup projects in Qatar. Additionally, development economists have warned of Nepal's overreliance on labor migration and remittance inflows to keep its economy afloat, with one economist stating that "the mass migrant outflow is a reflection of the complete collapse of Nepal's economy". Much of the money in Nepal is earned outside of the country, and is in turn spent on imported goods that were produced outside of Nepal - meaning that there isn't much of a "value-add" by Nepal on either end. The large inflows of cash coming in from overseas workers contributed to asset valuation bubbles and were largely blamed for the crashes in the country's real estate market and stock market in 2011. Hydropower is one area that is attracting attention. Nepal has hydropower potential of 83,000 megawatts, but will require large megaprojects to reach that anything near that capacity. Currently, hydropower accounts for only 2% of all energy consumed in Nepal. In-country energy demand could reach 10,000 megawatts in the near future, which would allow ample overcapacity for regional export, particularly to India, if Nepal were able to scale up and develop its hydropower capacity. A number of the projects, however, especially those being financed by China, have come under scrutiny for potentially negative environmental consequences. Nepal's per capita electricity consumption of 93 units is the lowest in Asia, contrasted with India (644), China (2,942), and Sri Lanka (445). Tourism is another key sector of the economy. Nepal's mountains attract many mountaineers, adventure thrill-seekers, and Hindu/Buddhist pilgrims. The Mount Everest disaster in April 2014, however, highlighted the dark side of the growth in tourist arrivals and the often harsh conditions that many of Everest's Sherpas face. The tourism industry accounted for 3% of Nepal's GDP in 2012 and is the second largest source of foreign exchange for the country after remittances. Nepal attracted more than 600,000 foreign tourists in 2012, a 10% YoY increase and its tourism industry employs more than 550,000 people. Nepal has launched a renewed focus on attracting Asian tourists, with 75,000 Chinese tourists arriving in 2012, a 60% increase YoY. Agriculture is the traditional mainstay of the Nepali economy and the source of livelihood for 80% of the population. It accounts for more than 1/3 of GDP, with major exports including rice, wheat, maize, millet, barley, coffee, and tobacco. Nepal also has a small but growing textile and tapestry sector. Production of ready-made garments (RMG), carpets, and pashminas has grown steadily due to Nepal's duty-free export provisions. Exports to the EU in particular have benefited from the country's Least Developed Country (LDC) status and the recent depreciation of the Nepali Rupee. Looking forward, Nepal will need to overcome a number of significant challenges to continue to grow its economy and attract foreign investment. The liberalization of key industries, opening of its stock market, and reduction of corruption will all help towards that goal. Political stability has improved dramatically with the end of the civil war in 2006 and the completion of the peace process in 2013. Domestic job growth is vital to ensure that there are enough in-country opportunities for Nepal's rapidly urbanizing population, and the country cannot continue to rely on remittance inflows to prop up its economy. Nevertheless, Nepal stands to benefit from its strategic location nestled between two economic powerhouses, and Asia Frontier Capital expects to keep a close eye on developments in the country and positive signals that might indicate that Nepal is serious about liberalizing its stock exchange. |

||||||||||||||||||||||||

|

I hope you enjoyed reading our monthly newsletter and remain with kind regards, Thomas Hugger |

|||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||

Nepali men watching a performance and wearing the ubiquitous

Nepali men watching a performance and wearing the ubiquitous  Crowds gather at a temple in the center of Kathmandu's Durbar Square

Crowds gather at a temple in the center of Kathmandu's Durbar Square The dusty and manic streets of Kathmandu!

The dusty and manic streets of Kathmandu! Only 365 more steps to go…dodging monkeys and making

Only 365 more steps to go…dodging monkeys and making Nepali monks and locals gaze out at the hazy skyline

Nepali monks and locals gaze out at the hazy skyline Buddhist pilgrims come to spin the prayer wheels while

Buddhist pilgrims come to spin the prayer wheels while  A view over the terraced Pokhara Valley, taken while paragliding

A view over the terraced Pokhara Valley, taken while paragliding