Asia Frontier Capital (AFC) - August 2014 Newsletter |

||||||

In this IssueAFC Asia AFC Vietnam Fund

|

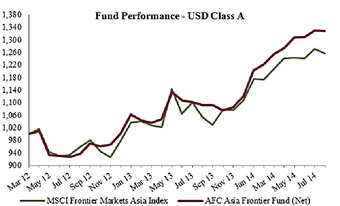

"In business, words are words; explanations are explanations, In August 2014 the AFC Asia Frontier Fund returned 0.0% and AFC Vietnam Fund returned +5.5%, bringing the YTD total for our funds at +18.7% and +20.3% respectively. This month saw some uncertainty facing frontier markets in Asia and around the world which resulted in a decline in the broader frontier indices. The MSCI Frontier Markets Asia Index and MSCI Frontier Markets Index lost -1.2% and -1.0% respectively last month. Across AFC’s investment universe the news was mixed and exciting as the AFC Asia Frontier Fund continues to outperform the MSCI Frontier Markets Asia Index. Vietnam and the AFC Vietnam Fund saw a significant rally whilst Pakistan was put under significant pressure due to an increase in political tension. This saw the local market slip while the Pakistani rupee depreciated roughly -3% in August which had a negative impact on returns calculated in USD. Both of our funds have shown to be resilient as the markets move and the ability of our funds to pick up key stocks outside of the major indexes has been a key differentiating factor that has supported our strong performance. The difference in return profile for AFC’s funds and closest comparable indices is a reflection of the differences in portfolio composition and in weighting to specific countries and sectors. The AFC Asia Frontier Fund’s investment strategy has an emphasis on finding consumer, healthcare, and materials stocks that offer attractive valuations. The AFC Vietnam Fund also does not track the Hanoi or Ho Chi Minh indices and has a much greater focus on significantly undervalued small and mid-cap stocks. New capital has continued to flow into both of our funds and we would like to welcome on board our new investors who have joined us this month and existing investors who have increased their allocations. AFC Asia Frontier Fund: USD 10 Million Milestone Special Offer – No Fees for 12 months!In September 2014 the AFC Asia Frontier Fund is set to pass a significant milestone with AUM reaching USD 10 million. To celebrate this event Asia Frontier Capital has decided to waive all fees for 12 months for one of the investors who subscribes in September 2014. This will be valid for new investors as well as existing investors that increase their allocation. This special offer will apply to the entire subscription amount received from that lucky investor in September 2014. The draw will be completely randomized and the lucky investor will be informed directly at the beginning of October when the September NAV is finalized. If you have any questions regarding this offer or the subscription process please be in touch with Stephen Friel at AFC NewsAFC in the Press

AFC on New Fund Platform As announced last month the AFC Asia Frontier Fund has been included on the Skandia International Fund platform. Having received several enquiries from clients regarding other fund platforms in the past months we have contacted them directly and the majority of them indicated that they are able to begin the due diligence process on our funds when they receive a request from their existing clients. If you would like assistance investing via your existing trading account please be in touch directly with them and Cc in Upcoming AFC TravelIf you will be in any of the locations listed below and have an interest in meeting with our team, please contact our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager Comment

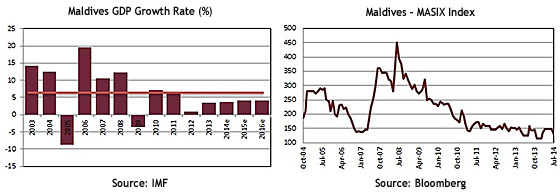

August witnessed political tensions in Pakistan which led the MSCI Frontier Markets Asia Index dropping by 1.2% but with AAFF being underweight in Pakistan relative to the benchmark index, the fund managed to weather the 5.7% correction in the KSE-100 Index along with a 3% depreciation the Pakistani rupee. This was possible due to the fund’s approach diversifying across its country universe in order to manage risk. This approach has helped the fund especially over the past year where we have seen political/security issues in Bangladesh, Vietnam, Iraq and Pakistan. Given these situations and our approach of managing risk using a top down approach and bottom up stock selection process has led to net returns of +18.7% year to date which is a reflection of our strategy of having our eyes and ears open to changing scenarios and opportunities. Coming back to Pakistan, the market correction occurred due to a political protest rally started by Pakistan Tehreek-e-Insaf (PTI), a political party formed by former cricketer, Imran Khan. The PTI’s initial issue was that parts of the May 2013 national elections were rigged but over the past few weeks this issue has been escalated by Imran Khan who wants the Prime Minister Nawaz Sharif to resign due to the fact that his claims that Sharif’s party rigged the elections. It is surprising that the PTI is making such allegations or escalating this issue almost 18 months after the elections. The May 2013 elections were convincingly won by Nawaz Sharif’s party, the PML-N (Pakistan Muslim League – Nawaz), which won 54% of the seats in the National Assembly. Given the strength of the government in the National Assembly, the likelihood of the Prime Minister stepping down due to pressure from the PTI appears low. These pressurizing tactics by the PTI were aided by another political party, PAT (Pakistan Awami Tehrik) which also joined the protest. The protest rally began on 14th August in the capital, Islamabad, and escalated in the last week of August. As of the time of writing, the protests have died down as the opposing political parties are holding talks to arrive at some sort of compromise. These events made the market nervous as there were rumors that the Army might step in and there could be a coup. Though this is a possibility if things take a serious turn, the likelihood of the Army staging a coup does not appear very high due to the fact that they are involved in anti-terrorist operations in Northwest Pakistan and there would be a lot of U.S. and Western pressure on Pakistan if the Army were to step in given the fact the country receives financial aid from the U.S. and the IMF. Having spoken to a few of our contacts on the ground, it does not appear that the protest has mass nationwide support, but we will watch and keep track of developments. The current government appears to be committed to reforming and stabilizing the economy and such political noise would only distract the government with its tasks in setting things straight in the economy. The correction in Pakistan was negated by good performance by AAFF holdings in Bangladesh, Iraq, Mongolia, Sri Lanka and Vietnam. Quarterly results for our larger holdings in Bangladesh, Sri Lanka and Vietnam were satisfactory and we continue to look to invest in companies we like and have met with personally. Pakistani companies should report later this month and we expect good numbers for our larger holdings in the country. The best performing indexes within the AAFF universe in August were Vietnam (+6.8%), followed by Iraq (+6.6%) and Bangladesh (+2.8%). The poorest performing markets were Cambodia (-6.4%) and Pakistan (-5.8%). The top-performing portfolio stocks were a Mongolian confectionary company (+28.5%), followed by a Vietnamese Brewery (+27.0%), a Mongolian leather producer (+22.5%) and a Vietnamese food producer (+21.7%). In August we added to existing positions in Bangladesh, Cambodia, Mongolia, Pakistan, Sri Lanka and Vietnam and we reduced one holding in Vietnam. We added new a Mongolian construction material company and a Mongolian leather producer. As of 31st August 2014, the portfolio was invested in 116 shares, 1 closed-end fund (with 30.1% discount to NAV), 1 GDR (with 66.3% discount) and held 7.7% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (5.1%) and a junior copper mine in Mongolia (3.0%). The countries with the largest asset allocation include Vietnam (22.0%), Pakistan (17.3%) and Bangladesh (13.3%). The sectors with the largest allocation of assets are consumer goods (39.2%) and materials (15.1%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 13.61x, the weighted average P/B ratio was 1.78x and the dividend yield was 4.55%. AFC Vietnam Fund - Manager CommentTo review this manager comment in German please click here. August 2014 was our second best month since the launch of the fund with a performance of +5.5%. With an NAV of USD 1,232 we clearly exceeded our old high of March. Our initial investors will certainly enjoy the performance of 23% in only 8 months, but may also have some concerns that we could face a possible setback. As you may remember, we had correctly predicted a correction (but not the reason) back in spring, but in contrast to those days, we now feel much more confident when we look forward to the upcoming months. Of course, there may be a consolidation in the short term, but the technical and economic conditions are much more favourable than they were six months ago. We started late last year with a portfolio of about 50 stocks with an average price/earnings ratio of about 7x, while the overall market was valued at about 12x. Today - 8 months and +23% later - we have 70 shares and still the same favourable average P/E ratio of 7x, while the overall market is now trading at about 14x. With the half year earnings season behind us, we discovered a few new and promising companies that fit well within our existing portfolio. What are the kind of risks we have to take into account? Our investments are broadly diversified over a large number of smaller companies, all with good balance sheets and attractive valuations, which are in our opinion vastly undervalued with a potential to increase by 100% and more in the coming years. There is of course always the risk of negative (and positive) surprises, but with such a high number of positions this doesn’t really represent a serious problem. We just experienced in the past month some great developments for our investments; such as for example the inclusion of FLC (a company we previously wrote about) in a few major indices, the analyst community finally started to discover some of our shares we are holding and as well an increasing number of local investors who seem to be interested in some of our investments. Regardless of the short-term movements in the stock market index, which was on some days strongly influenced by 1 single stock with a P/E ratio of about 18x and hence never would fit our investment criteria, our portfolio is as inexpensive as on the first day when we launched our fund. With our quantitative and fundamental investment approach, we often can’t rely on research reports, especially for smaller companies, and we therefore are calculating our own forecasts. After the completion of the half-year reporting season we can now draw a few very interesting conclusions. The first quarter results are typically not very meaningful to predict the full year and we increased our average forecast for annual sales in 2014 by 2.9% and earnings by 1.1%. These minimal changes in our estimates after three months shows us that the development of these companies, which received so far very little attention, can be quite accurately forecasted and that in the long term they probably will exploit their full potential. Currently the average 2014 earnings forecast for our portfolio is at +13.2% in comparison to +12.6% in 2013, and the arithmetic mean for the profit increase is even at +23%. We can of course never exclude the possibilities of shorter consolidation periods, but we clearly think that a reversal of the positive trend for this year is not very likely. As of 31st August 2014 the portfolio was invested in 70 shares and held 4.0% in cash. The sectors with the largest allocation of assets were consumer goods (35.5%) and industrials (20.3%). The fund’s weighted average trailing P/E ratio was 6.98x, the weighted average P/B ratio was 1.02x and the average dividend yield was 6.40%. AFC Country Snapshot: MaldivesThe Maldives, an archipelago nation consisting of over 1,000 islands in the Indian Ocean, has experienced consistent economic growth throughout the latter part of the last decade with annual real GDP growth averaging 6%. The Maldivian economy is primarily dependent on tourism - more than 700,000 tourists visit annually - and auxiliary industries such as transportation, communication, and construction. Fishing remains an important aspect of the economy as well, though catch has dropped substantially in recent years. The government has begun to privatize certain sectors, starting with the main airport, and is partially privatizing the energy sector. In addition, the government is aggressively promoting the construction of new island resorts throughout the islands.

Stock Market: The Maldives Stock Exchange (MSE) is located in Male and was established in April 2001. Currently the MSE lists six companies: Maldives Transport and Contracting Company Plc, Bank of Maldives, State Trading Organization, Maldives Tourism Development Corporation Plc, Amana Takaful Maldives and Dhivehi Raajjeyge Gulhun Plc. MSE has a total market capitalization of USD 500 million as of August 2014.

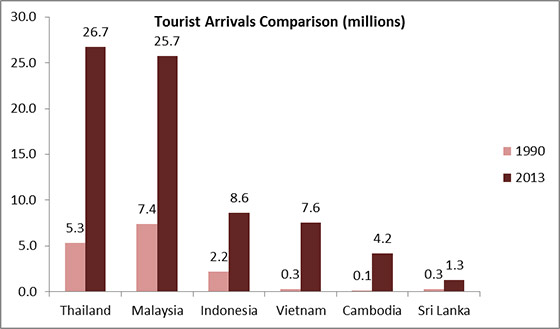

Country snapshots for all of AFC's markets can be found on our website at www.asiafrontiercapital.com AFC Country Report: MaldivesPerhaps you are surprised to see that this month’s country report focuses on the Maldives, a tiny island nation consisting of a chain of over 1,000 islands surrounding 26 atolls in the middle of the Indian Ocean and Arabian Sea. Roughly 600 km southwest of India and 750 km southwest of Sri Lanka, the Maldives are certainly best known for their luxurious beaches and world-class resorts, providing a remote paradise for well-heeled holidaymakers accessible via direct flights from Singapore, Dubai, and Istanbul, amongst others. Malé, Capital of Maldives – 5th most densely populated island on earth With a population of under 400,000, the country is heavily dependent on tourism to support its USD 2.3 billion economy, and the tourism industry accounts for approximately 40% of GDP, according to the Asian Development Bank (ADB). Transport and construction are two other major economic sectors intricately linked to the tourism industry and the demand from hotels and resorts. Traditionally, fishing was the backbone of the Maldivian economy, and the sector still employs 20% of the labor force and accounts for 10% of GDP. About half of the catch is exported, primarily to Asia and Europe, and all fishing must be done by line – nets are illegal. Environmental issues are a serious concern for the Maldives, which is the lowest country in the world in terms of elevation. Climate change activists have warned that the Maldives is at risk of disappearing as ocean levels rise due to global warming, and the nation is also prone to floods, damaged marine life, and natural disasters due to its vulnerable location and lack of natural barriers or storm deterrents. The government has made climate change a focal area of its public policy and plans to eliminate or offset all of its carbon emissions by 2020. Economic growth is projected to pick up moderately to 4.5% in 2014, according to the ADB, primarily due to favorable economic prospects in Asia and an increasing number of high-end tourists from China, India, and other emerging markets in Asia. There is a large number of airlines connecting the Maldives to destinations in Asia, Europe, and the Middle East, and budget carriers have also recently entered the market, including Air Asia (to Kuala Lumpur), Tiger Air (to Singapore), and flydubai (to Dubai). However, the island wants to retain its strategy of being a high-end tourist destination, and the average rate per night at most hotels and resorts is USD 400-500, with 5-star resorts ranging up to USD 4,000 / night! The Maldives Stock Exchange (MSE) is located in the capital, Malé, and started as a Securities Trading Floor in 2002. The exchange currently has six listed companies in the financial services, tourism, trading, transport & construction, insurance, and telecommunications sectors, and as of August 2014 had a total market capitalization of USD 500 million. The country’s Capital Market Development Authority (CMDA) is working with the Ministry of Economic Development & Trade to facilitate foreign portfolio investment in the Maldives, but currently the bourse is not open for foreign investment. Investment opportunities in the country also exist via Sri Lankan companies with assets located in the Maldives. Aitken Spence is a Sri Lankan blue chip conglomerate that is listed on the Colombo Stock Exchange and is the largest foreign resort operator in the Maldives. Aitken Spence also offers freight forwarding, cargo, and event management services in the Maldives and serves as a survey and claim settling agent for Lloyd’s of London, covering the principal commercial port in the Maldives. John Keells Holdings is a similar Sri Lankan conglomerate that operates five resorts in the Maldives and trades in Colombo. Other Sri Lankan companies that are publicly-listed on the Colombo Stock Exchange and have business operations in the Maldives include Ceylinco (insurance), Amana Takaful (insurance), eChannelling (healthcare/ICT), and Sierra Cables (wire/cable manufacturing). Interest in the Maldives has extended beyond just regional businesses. In February 2013, international private equity firm The Blackstone Group purchased a controlling stake in two Maldivian seaplane companies, Maldivian Air Taxi and Trans Maldivian Airways. The terms of the transaction were not disclosed, but the deal highlighted the prominence of the country’s tourism industry and its international appeal. As developed economies in the West recover and incomes in Asia continue to produce a new pool of high-end tourists, the Maldives should experience robust tourism growth that will bring much-needed foreign exchange reserves and cash to the economy. But given the serious of threat of global warming and the potential consequences it may have on the tiny island nation, Maldivians are increasingly concerned about their nation’s future and how it will be affected by environmental changes that are largely beyond its control. AFC Travel Report: Sri LankaIn line with our process of being on the ground in the countries we invest in, Senior Investment Analyst of the AFC Asia Frontier Fund, Ruchir Desai travelled to Sri Lanka to attend an investor conference held in Colombo. This was my first visit to Sri Lanka since joining the AFC team and I was looking forward to visiting the country and meeting companies, as I have heard good things about the country from my AFC colleagues. Flying in from a connecting flight from Singapore it was not surprising to see quite a few tourists at immigration given that Sri Lanka is an upcoming tourist destination in Asia. Connectivity to Colombo from large Asian cities is quite good with most established airlines flying to the city. Getting through immigration was pretty uneventful and the airport is still pretty basic but I think as the tourism economy and the economy in general grows one will see changes and improvements to the airport infrastructure. Since tourism is expected to play an important part of the economy, applying for a visa is easy compared to travelling to other countries in Asia as you just need to apply online without much paperwork. Once through immigration and on the way to collect bags, you pass through a small hallway loaded with shops selling electronic goods and other duty free goods with shopkeepers trying to hustle these goods. Welcome to Colombo Duty Free! Getting hold of a pre-paid taxi is also pretty easy from one of the taxi counters and once you are on the road, getting to the city takes about 20-30 minutes due to the newly launched Colombo-Katunayake Expressway. In fact this is one of the major infrastructure developments which have been executed or are being planned in Sri Lanka. The Southern Expressway has also been launched recently which connects Colombo to the Southern city of Galle. The 120 km odd journey from Colombo to Galle now takes about 90 minutes compared to a few hours prior to the launch of the expressway. More expressways are also being planned connecting Colombo to Central and Northern Sri Lanka. The traffic within the city is like any developing city in Asia but talking to individuals who live in Colombo or who have been to the city prior to the end of the civil war in 2009, there has been a pretty significant change in the environment. It used to take a few hours to get to the city from the airport due to the fact there was no expressway and this was made worse by security checks within the city. I did not go through any security checks outside the airport, within the city or at the hotel. It gives a sense of stability post 2009. This lack of hassle is quite important if the government wants to promote tourism. Tourist arrivals in 1982 prior to the start of the conflict were about 400,000 and in 2009 when the conflict ended the number was about 450,000. Not much movement in this number given the situation the country but tourist arrivals in 2013 were 1.27 million and this number has been growing at double digit growth rates since 2009. The Sri Lanka tourism market is still very small compared to other Asian tourist destinations and this could change in the next decade as more star hotels and infrastructure come up.

Since I got to Colombo on a Sunday I had the day free to check out the city and coincidentally it was also Day 4 of the 2nd Cricket Test match between Sri Lanka and Pakistan. The match was being played at the Sinhalese Sports Club and I took the opportunity to go watch an hour or so of play. Post some live action Cricket I was driven through the city and parts of it reminded me a lot of Mumbai as many of the older buildings built during British times have similar architecture. Galle Face Road is the heart of downtown Colombo and this road overlooks the Indian Ocean. Most of the five star hotels, commercial and government buildings are located in and around this area. Two new five star hotels are expected to come up in the next few years on Galle Face Road overlooking the ocean. Shangri La Hotels and ITC Hotels of India are both putting up five start properties adjacent to each other. Sites of Shangri-La and ITC Hotel on Galle Face Road, Colombo Room capacity is expected to double in Colombo in the next three to four years as other brands like Grand Hyatt, Sheraton and Movenpick are also expected to put up new capacity. Furthermore, the largest conglomerate in Sri Lanka by market capitalisation, John Keells Holdings, is developing the Waterfront project which will include a casino, hotel and retail space. It will not be surprising to see the skyline of Colombo change in the coming decade as new real estate developments get executed. This expected increase in room capacity reflects the change in the operating environment post the conflict in 2009. It would not be surprising to see existing five star hotels in the city to go through refurbishments in the near future as there was not much completion until a few years ago. The investor conference was held at one of the city’s five star hotels, Cinnamon Grand which is a part of John Keells Hotels (a subsidiary of John Keells Holdings). The morning session on day one was opened by the Governor of the Central Bank of Sri Lanka and over the next two days I would have the opportunity to meet with management teams of 14 companies some of which are part of our portfolio holdings. We had met some of the management teams at the Sri Lanka Investor Forum in Hong Kong last year so it was good to meet again and get updates first hand. The companies that I could meet were diverse from banks, consumer staples to infrastructure. Meeting with management teams of companies we hold helped re-assess our view on them and we are confident in the outlook for most of our Sri Lankan holdings but would review the performances of holdings on a quarterly basis. The third day of the conference was spent outside the hotel which I think is always good as going to see the management teams in their offices or manufacturing plants gives a better feel of the company and its outlook. Balance sheet and cash flows is just one part of due diligence. Being out on the road also gives a feel of the city and the country. We visited the factories of Ceylon Tobacco and Ceylon Cold Stores. Ceylon Tobacco is the Sri Lankan subsidiary of British American Tobacco while Ceylon Cold Stores is the leading soft drinks and ice cream manufacturer in the country. The machinery and equipment at both factories was modern with very knowledgeable factory staff as well as management teams. With wide distribution networks, established brands and modern equipment both companies have built up a strong competitive advantage for themselves. In between one of the visits we also got time to visit the modern retail store, “Keells Super” which is also part of the John Keells Holding group and is a subsidiary of Ceylon Cold Stores. It is what you would expect from any modern retail store in a developing country but what stood out was pop music playing in the store. That was a first. Hemas is a leading consumer brand in Sri Lanka and its products share shelf space in the store with Colgate and Unilever products. Prices for its products are also lower than the competition as it caters to the larger mass market. We also got the chance to check out a residential property under development and the view from the 34th floor apartment. Real estate prices zoomed post the end of the 2009 conflict but dropped in 2011-2012 as interest rates increased but prices have recovered over the past year. View of Colombo skyline Overall, it was a good trip as I got a chance to meet companies we hold in the portfolio as well as check out on the ground operations for some companies. I look forward to visiting other parts of Sri Lanka in the future to explore the country and opportunities further. We look forward to continue visiting companies on the ground not only in Sri Lanka but also in other countries in our universe and updating our investors and readers. |

|||||

|

I hope you enjoyed reading our monthly newsletter and remain with kind regards, Thomas Hugger |

||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

||||||

GO TOP |

||||||

Source: John Keells Holdings, Country specific Tourist Departments

Source: John Keells Holdings, Country specific Tourist Departments