Asia Frontier Capital (AFC) - May 2016 Newsletter |

|||||||||||||||||||||||||||||||

In this IssueAFC Asia AFC Iraq AFC Vietnam Fund

|

"The best time to plant a tree was 20 years ago.

AFC Funds Performance Summary

A famous Chinese proverb says “The best time to plant a tree was 20 years ago. The second best time is now”. This often applies to investments as well. Sometimes this proverb is quoted in situations where starting 20 years ago is not an option and the proverb is merely used as an argument to invest now. But to us an alternative interpretation is more appropriate. We can almost invest in the past by focusing on countries in the world whose development has been lagging behind by 20-30 years, and whose development is now ongoing or imminent. It doesn’t take a rocket scientist to realize that countries which come out of isolation or civil war and move back into the fold of peaceful developing nations in the global economy have a better chance of growing faster than developed countries. Countries whose development have been lagging behind for 20-30 years won’t become emerging tiger economies overnight, but it is reasonable to expect that some of these countries may soon go through a development cycle that their emerging market neighbours have already experienced. Let us have a look at two typical emerging market powers India and China. With all their challenges and difficulties these countries made great progress in recent decades, each in their own way. Besides growth of GDP, education levels, reduction of poverty and the increase of life expectancy, their stock markets have also seen very healthy developments. India’s benchmark BSE Sensex Index for example has grown from 14.7 USD at the end of 1979 to 394.3 USD at the end of 2015 representing an increase of 26.9x or a compound annual growth rate of 9.6% in USD terms. The development in China was even faster when the country opened up under Deng Xiaoping and the Shanghai Stock Exchange was re-opened in 1990. Since then the Shanghai Composite Index subsequently grew from 24.4 (in USD terms) to 545.5 (in USD terms) at the end of 2015 which is an increase of 22.4x representing a growth rate of 13.2% annualized in USD terms. These growth numbers don’t account for the effect of dividends and compounding thereof, or for the benefits of active portfolio management. We believe that some of the same factors playing a role in the growth of India and China are now taking place in most of the frontier markets that we invest in, and undoubtedly some of these markets will become recognized as emerging markets in the medium term, with a corresponding increase in asset values. We aim to take advantage of these developments by actively investing in the best companies in these countries that most benefit from the overall development of these economies. However Asia Frontier Capital is not alone in seeing opportunities in these frontier countries. President Obama just travelled to Vietnam to strengthen ties even further and he sent John Kerry, the US Secretary of State, to Mongolia to do more of the same there. While Asia Pacific Equity Funds have shown significant net outflows during the last few years, as reported by eVestment, our funds have all seen net inflows. This accelerated in the past two months with significant inflows in our AFC Vietnam Fund and, including May 2016 subscriptions, the AFC Vietnam Fund has now reached USD 26 million in assets under management. This could partly be explained by the outstanding return of the AFC Vietnam Fund which added another +1.4% in May reaching a performance of +55.2% since inception which represents a very attractive annualized return of +19.2% since inception, while the Ho Chi Minh index only returned +14.6% in the same period. It is no surprise therefore that the AFC Vietnam Fund won another recognition award from BarclayHedge for being amongst the top 10 performing funds in the sectors Emerging Markets - Asia and Emerging Markets Equity - Asia.

AFC to establish an office in Vietnam and appoint a new fund managerAfter a period of rapid growth in the AFC Vietnam Fund, we have decided to expand in order to capture future growth opportunities through having a local presence in Vietnam. Asia Frontier Capital is therefore in the process of opening an office in Ho Chi Minh City (HCMC) which should be operational in the second half of this year. We are also very pleased to announce that Mr. Vicente Nguyen will join us as Fund Manager for the AFC Vietnam Fund and Chief Representative of our future HCMC office as of 1st July 2016. He will be reporting to Andreas Vogelsanger, CEO of Asia Frontier Capital (Vietnam) Limited. Vicente has over 10 years of wide-ranging experience in investment management, audit and stock brokerage business. He holds an MBA from Ecole de Management Strasbourg in France, an audit and accounting diploma from Institute of Business Management and Accounting and University of Economics in HCMC. Prior to joining Asia Frontier Capital (Vietnam) Ltd., Vicente was the CEO of a brokerage company in HCMC.

|

||||||||||||||||||||||||||||||

| Ho Chi Minh City | 28th May - 14th June | Scott Osheroff |

| Tokyo | 20th - 23rd June | Andreas Vogelsanger |

| Nagoya | 24th June | Andreas Vogelsanger |

| Hong Kong | 26th June - 14th July | Andreas Vogelsanger |

| Toronto | 27th June | Thomas Hugger |

| New York | 28th June - 2nd July | Thomas Hugger |

| Luzern, Switzerland | 18th July | Andreas Vogelsanger |

| Zurich | 19th - 21thJuly | Andreas Vogelsanger |

| Geneva | 26th - 27thJuly | Andreas Vogelsanger |

| London | 28th - 29th July | Andreas Vogelsanger |

AFC Asia Frontier Fund - Manager Comment May 2016

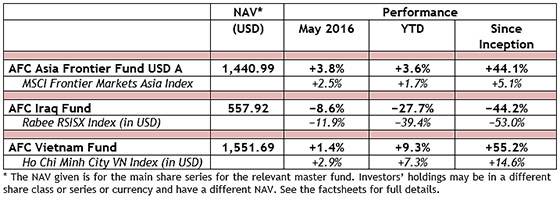

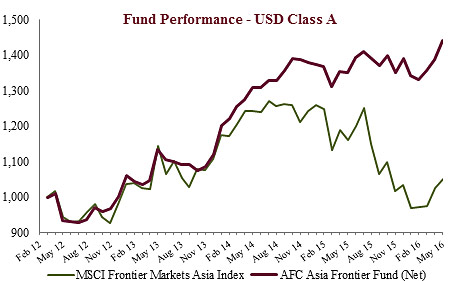

AFC Asia Frontier Fund (AAFF) USD A-shares gained +3.8% in May 2016. This month, the fund outperformed the MSCI Frontier Markets Asia Index (+2.5%), the MSCI Frontier Markets Index (+0.3%) and the MSCI World Index (+0.2%). The USD A Class shares achieved a new all-time high at USD 1,440.99 (the previous high was in July 2015 at an NAV of USD 1,409.51). The performance since inception, on 31st March 2012 now stands at +44.1% versus the MSCI Frontier Asia Index which is up +5.1% and MSCI Frontier Index (+4.6%) during the same time period.

Positive performance continued for the fund during the month and this was the fourth best monthly performance since inception. Fund performance and markets have seen a recovery after a turbulent start to the year with the fund now up +3.6% YTD. The 1 year performance is also remarkable at +6.7%, better than over 97% of similar funds in Bloomberg’s universe, while many markets have a negative performance in the last 12 months: Dow Jones: -1.3%; MSCI World: -6.3%; MSCI Emerging Markets: -19.6% and MSCI Europe: -12.6%, all in USD terms.

Though the fund’s larger markets of Bangladesh, Pakistan and Sri Lanka helped with performance during the month the leading driver of performance were Mongolian junior mining stocks which rallied smartly. A junior copper explorer announced a strategic merger of exploration properties in Mongolia’s famed Oyu Tolgoi copper/gold belt which well-positions the company going forward. Another junior explorer, in the gold sector, experienced a good run of late due to multiple intersections of high grade gold at a highly prospective exploration site. Share prices of these companies have been further supported by renewed interest in the broader resource sector, as well as, the Mongolian mining sector.

In Bangladesh, performance was aided by the fund’s largest holding, a pharmaceutical company in which the fund holds the company’s GDR and this trades at a 62% discount to the local listing in Dhaka. In Pakistan, the State Bank of Pakistan unexpectedly cut benchmark interest rates and this was negative for the banks but with the fund having no exposure to Pakistani banks this correction in banking stocks was positive for relative performance. It was announced that Sri Lanka will be receiving a loan of USD 1.5 billion from the IMF to overcome the near term balance of payment issues that it faces but in the short run the country is expected to face some headwinds given its fiscal position. Vietnam performance was led by a stationery company and a pharmaceutical company both of which showed good net profit growth in the March 2016 quarter.

The best performing indexes in the AAFF universe in May were Bangladesh with +5.3%, Pakistan (+3.9%) and Vietnam (VN-Index) with +3.4%. The poorest performing markets were Iraq with -10.9% and Cambodia (-6.0%). The top-performing portfolio stocks were a junior copper mining company from Mongolia (+100%), followed by a Mongolian junior gold mining company (+54.3%), a Mongolian trading company (+34.9%), and an oil and gas company from Papua New Guinea (+28.8%).

In May we added to existing positions in Cambodia, Mongolia, and Vietnam and we reduced our holding in a Sri Lankan holding company.

As of 31st May 2016 the portfolio was invested in 101 companies, 1 fund and held 6.3% in cash. The two biggest stock positions were a pharmaceutical company in Bangladesh (6.6%) and a Pakistani pharmaceutical company (5.0%). The countries with the largest asset allocation include Vietnam (30.2%), Pakistan (20.4%) and Bangladesh (15.6%). The sectors with the largest allocation of assets are consumer goods (35.8%) and healthcare (17.9%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 16.99 x, the estimated weighted average P/B ratio was 1.52 x and the estimated portfolio dividend yield was 2.96%.

For more information about Asia Frontier Capital’s Asia Frontier Fund please click the following links:

AFC Iraq Fund Manager Comment May 2016

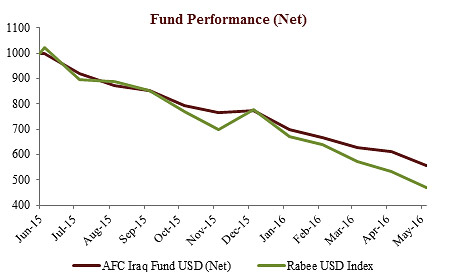

AFC Iraq Fund Class D shares returned -8.6% in May 2016 with an NAV of USD 557.92, an outperformance of +3.3% vs. the Rabee RSISX USD Index (RSISUSD) which returned -11.9% in USD terms. The fund has outperformed the RSISUSD by +11.7% YTD and +8.7% since inception.

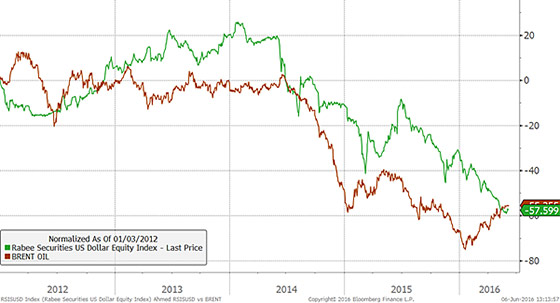

The market continued its decline for the 5th month and hasn’t responded to the recovery in oil prices even though it followed them, with a time lag, during the last few years. The chart below shows the market's correlation to the oil price and price trend.

The Iraqi equity market as measured by

Rabee Securities RSISUSD Index vs. brent crude

(Source: Bloomberg)

The economy's dependence on oil is the largest factor affecting domestic liquidity as it accounts for most of the GDP, directly and indirectly. The government response to lower oil revenues has been to reduce spending on wages and pensions, to stop spending on goods & services as well as investments. Proposed government IOU's, in lieu of its obligations to local businesses, are expected to be trading at discounts of up 40% while the Kurdistan Regional Government’s IOU’s are reported to be trading at discounts of up to 60%. The conclusion being that the continued dry up of local liquidity that manifested itself on the ISX by forced/distressed selling and in combination with foreign portfolio selling, as reported in the last few newsletters, took a significant toll on the market. A consequence of the persistent selling over the last few months is that prices for most stocks are low enough that each price increment between buying and selling is a few percentage points and as such the mere trading on the bid side or an increment lower is 2-4% lower points and in the process exaggerate the declines.

Every stock within the RSISUSD is down by more than -19% YTD with the biggest losers being Mamoura Real Estate (-45.7%), Iraq Middle East Bank (-41.2%), Bank of Baghdad (-39.3%), Investment Bank of Iraq (-38.2%), Asiacell (-36.5%), Gulf Commercial Bank (-33.3%) and Baghdad Soft Drinks (-31.6%).

Strategic and liquid investors have begun to take advantage of the current market environment with Bahrain’s Al-Ahli Bank announcing an increase in its holding of Iraq’s Commercial Bank from 54.7% to 64.7% by purchases in the open market over the next two months. Commercial Bank is currently trading at 0.4x book value, which is in-line with selected banks under coverage with an average of 0.4x and a range of 0.1-0.8x book value. Keeping in mind that banking in Iraq is in its infancy and as such current low valuations are based on depressed earnings that are a function of a country in conflict and as such don’t reflect the earnings potential once the country is the on a post-conflict trajectory to recovery.

Iraq’s international sponsors are backing their commitment by providing substantial amounts of financial support with nearly USD 13bn as reported in the last few weeks. The IMF set the pace with a $5.4bn aid package which could unlock $15bn more in international assistance over the next three years. Followed by the Paris Club’s postponement of about $800m in debt repayments, the Islamic Development Bank announced $3bn of loans and the G7 will provide $3.6bn in bilateral assistance and other financial support. These would be separate from the announced plans for the reconstruction of the ISIS liberated territories.

Ultimately, the funds will work their way through the system and with higher oil revenues should relieve the strains on local liquidity. Moreover, the fundamentals of supply and demand for oil are coming into balance quicker than expected after the excess supply of the year with demand being stronger than anticipated from emerging markets especially India. The upshot is likely to be either stable or higher oil prices which would encourage foreign fund flows into Iraq. The combination of improving local liquidity and potential foreign inflows will arrest and reverse the market’s downtrend; however, the exact timing continues to be elusive but in the meantime the opportunity is to acquire quality assets at attractive prices while the focus of the market is only on the negatives.

The fight against ISIS has accelerated with coordinated actions by the international coalition, Kurdish & Iraqi forces in Syria & Iraq by attacking ISIS on multiple fronts. In Syria, the focus has been on surrounding & isolating the capital of Raqqa while cutting ISIS lifelines through the Syrian-Turkish border. In Iraq on the other hand, Kurdish forces with US support are surrounding and pressuring Mosul while Iraqi troops with aerial support from the international coalition are doing the same to the city of Fallujah which was the first city to fall to ISIS in early 2014. Irrespective of the speculation of whether, how and when the cities are liberated the real story is the combined actions are bound to take a significant toll on ISIS, draining its declining resources and accelerating its fall from within. In all, the end of the conflict could happen sooner than expected and with it the massive investment cycle to rebuild and create prosperity as a long-term solution to the original crisis that was fertile grounds for the rise of extremism.

Looking at the portfolio, as of 31st May 2016, the AFC Iraq Fund was invested in 14 companies and held 1.1% in cash. As the fund invests in both local and foreign listed companies that have the majority of their business activities in Iraq, the countries with the largest asset allocation were Iraq (92.9%), Norway (5.5%), and the UK (1.6%). The sectors with the largest allocation of assets were financials (47.2%) and consumer staples (26.1%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 17.44x, the estimated weighted average P/B ratio was 1.00x, and the estimated portfolio dividend yield was 4.56%.

For more information about Asia Frontier Capital’s Iraq Fund, please click the following links:

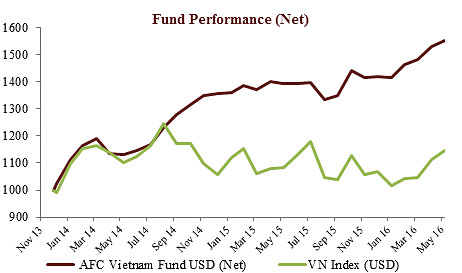

AFC Vietnam Fund - Manager Comment May 2016

To read this month’s fund update in German please click here.

The AFC Vietnam Fund gained +1.4% in May to a NAV of USD 1,551.69, bringing the year to date net return to +9.3% and the net return since inception to +55.2% or +19.2% annualized. By comparison, the May performance of the Ho Chi Minh City VN Index was up +2.9% while and the Hanoi VH Index increased by +1.1% (in USD terms). Since inception the AFC Vietnam Fund has outperformed the VN and VH Indices by +40.6% and +42.1% respectively (in USD terms).

Despite some minor corrections, the month of May had some very inhomogeneous market developments. Some blue chips increased significantly, while the majority of the shares hardly moved. For the entire month the indices advanced by +3.4% in HCMC and +1.5% in Hanoi. The Vietnamese Dong lost about half a percent versus the USD, in line with the decline in other emerging market currencies.

The VN30-Index, which consists of 30 liquid and large companies from both exchanges, showed a similar picture to the HCMC index, described in the last interim report. Recent political decisions for example on lower than expected liquidity requirements for banks had a very positive impact on some stocks in this sector. The strong increase in the four weeks from mid-April to mid-May was followed by an equally strong correction, but the broader market hardly took notice of it. Volatility (= risk) of larger stocks, which is mostly driven by foreign in- or out-flows, is often higher than the volatility of companies that do not appear on foreign investors’ radar screens.

VN 30 Index

(Source: Bloomberg)

Contrary to the opinion of some experts, who believe that the upward movement in the stock market ends as soon as this increase starts spilling over to smaller firms, we argue the opposite. Only when local investors are beginning to have trust in the long term recovery of the economy and stock market, without trying to follow or to anticipate the often erratic investor behaviour of foreign investment funds, will we see a continuation of the multi-year stock market upturn. Positive political and economic developments are the fuel for the stock market engine; even the fastest Ferrari needs somebody to continuously push the accelerator pedal (= buy orders) in order to advance. A stock market boom ends after a while when it is no longer supported by a broad base - and not showing strength if 10% of the market participants (current foreign investor participation) push the index up for a few days or weeks. Such striking differences between the index and the broader market, in small markets such as Vietnam are rather unusual. In more developed markets such as the US, where divergences in the market breadth are almost always a precursor of a change of direction, such as in 2007 before the bursting of the Internet bubble in 1999, are enormously important as medium-term indicators for stock market developments. Vietnam is currently rather in a consolidation phase as in a boom phase, and we therefore don’t expect any negative consequence of the current market behaviour.

In our case - and hence we regularly refer to the market breadth (advance/decline ratio) in Vietnam – this ratio has even a higher impact on our performance. For example, on a positive day where roughly 700 shares are traded, and the index increase is only due to the largest 5-10 stocks and in balance there are more shares declining than advancing, we will hardly make any money with our diversified portfolio of 80+ stocks, even if we are also invested in three of the largest companies. Unfortunately, we have to admit that the market breakout we were hoping for last month has not yet occurred but fortunately the technical picture still looks OK.

The fact that we were still able to achieve a positive performance over the past few months despite a weaker market breadth, is due to the positive development of many of our holdings where the expected re-rating slowly but surely continues. On the one hand, there are more and more companies from our portfolio which are gradually discovered and recommended by analysts. This has led to increased interest from local investors who are looking to buy share blocks in our investments. A recent example of this happened last week, where we could have sold the entire position of our smallest company within seconds, as 50% of all outstanding shares (!) appeared as a buy order at market price in the trading system. Obviously there are other investors who think that a profitable, debt-free company, trading at 50% below book value looks attractive.

The economic recovery of Vietnam is now also reflected in lower risk premiums. With a trade surplus of USD 1.8 billion in the first four months, record investments and a fairly stable development of the currency (YTD +0.4% versus USD), fears which have led to uncertainties at the beginning of the year, allayed again. The current slight weakening of the currency is therefore rather a consequence of the recent expectations of a rate hike in the US. The periodically emerging realization that interest rates will not stay at zero forever led to the now somewhat boring "risk-off" reversal, even with the new European Super Mario’s economic doctrine where countries will save more money the higher their debt is due to negative interest rates. In other words, we now see a - necessary - countermovement, after the FED postponed in panic mode an imminent rate hike back in February, which led to an upswing in emerging markets and commodities while the USD fell. It is interesting and certainly positive to note that important industrial raw materials such as copper and oil didn’t correct and that the Emerging Markets ETF EEM, which serves as a good indicator for investors’ appetite for emerging markets experienced only a healthy correction.

By now we would have loved to see a stronger stock market indeed, but from a perspective of our numerous new customers it is at least providing them with a still excellent entry point. We are also observing a significantly higher interest in Vietnam through international conferences and in the media compared to just a few months ago. We hope this spark will soon catch local investors who hopefully were positively affected by the increased media presence thanks to the recent visit of President Obama.

At the end of May the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (2.9%) – a manufacturer of electrical and telecom equipment, Bao Viet Securities JSC (2.3%) – a securities brokerage company, Nui Nho Stone JSC (1.7%) – a stone mining company, Taya Vietnam Electric Wire and Cable JSC (1.7%) – a electric wire manufacturer, and Thien Long Group Corp (1.7%) – an manufacturer of office supplies.

The portfolio was invested in 85 names and held 7.8% in cash. The sectors with the largest allocation of assets were consumer goods (33.8%) and materials (13.7%). The fund’s estimated weighted average trailing P/E ratio was 8.29x, the estimated weighted average P/B ratio was 1.15x and the estimated portfolio dividend yield was 5.57%.

For more information about Asia Frontier Capital’s Vietnam Fund please click the following links:

Vietnam Travel Report – May 2016

In line with our process of being on the ground in the countries we invest in, Senior Investment Analyst Ruchir Desai travelled to Vietnam last month.

This was my second visit to Vietnam for the year as there are yet many more companies to meet and also much to learn from being on the ground. This time my visit focussed on meeting newer companies which we have not met before, as well as carrying out site visits to some of the listed port companies in Northern Vietnam and check out the factories of the fund’s existing holdings.

I started my trip from Hanoi and as mentioned in our previous newsletters, the infrastructure in terms of travelling from the airport to the city has improved tremendously since my first visit to Vietnam almost three years ago. My first day was full of company visits; a toll way operator/real estate developer, a consumer company and a company which manufactures glass, ceramic floor tiles and sanitary ware. The next day I traveled to Hai Duong, which is a 90 minute drive from Hanoi, to visit the factory of one of the funds existing holdings, an industrial pump manufacturing company. Since this is a smaller company there is a lot of room for improvement in terms of manufacturing capability and efficiency. Positively, the company management is keen to improve on this in the coming years. Afterwards, we travelled (the local analyst and myself) for another 45 odd minutes onto the new highway which connects Hai Duong to Haiphong. This new highway actually connects Hanoi to Haiphong but we just took it from Hai Duong. The new highway was opened recently, but I was told the fare to use it is quite high relative to the older highway so a lot of traffic is still using the older highway. Though in in terms of quality the newer highway seemed to be worth the higher fare.

Haiphong is located about 120 km east of Hanoi. A smaller city than Hanoi and Ho Chi Minh City it is much quieter, but it is the leading port area in North Vietnam and is home to more than a dozen port companies, some of which are listed. Understanding the location of these ports is important as this affects their throughput as well as the size of ships which they can berth. Also, these ports are all currently river ports which are located next to the sea and hence cannot accommodate vessels of the size that Hong Kong and Singapore can accommodate. As can be seen in the map below, location is paramount as the ports closer to the mouth of the river can accommodate larger ships compared to some of the ports which are further upstream. Besides location, another development which could impact the dynamics of the ports is the new deep water port under construction up on Cat Hai Island, to the east of Haiphong. This deep water port will be connected to the mainland by a bridge and is expected to have a capacity of 1.1 million TEUs (twenty foot equivalents) in its first phase. It will accommodate much larger vessels and is expected to begin operations in 2019. The development of this port could be a threat to the ports along the river as their utilisation levels fall and one cannot rule out some sort of consolidation amongst the smaller ports in the near future.

Location of ports in Haiphong is important

(Source: Rongviet Securities)

The port companies I met ranged from smaller players having capacity of around 200,000 TEUs to larger players having capacities of 1 million TEUs. The management teams of all three ports companies did mention that the new deep water port could be a threat going forward. From what I saw on the ground all the ports are pretty much lined up one after the other. I did manage to take some pictures although at one point we were stopped by a security officer saying that “foreigners” need permission to be in the port premises.

On the ground visit to ports in Haiphong

(Source: Asia Frontier Capital)

In between meetings, we had lunch at a local seafood restaurant. This is a plus about visiting other parts of Vietnam besides just Hanoi and Ho Chi Minh City, as one gets to taste the regional cuisine.

Local delicacies for lunch in Haiphong

(Source: Asia Frontier Capital)

Since I was going to be spending most of the day in Haiphong I decided to fly to Ho Chi Minh City (HCMC) from Haiphong’s international airport.

It is always refreshing to visit Ho Chi Minh City as it always has a good buzz to it. My meetings in HCMC kicked off with the largest fertilizer company, a ferry company and a tire manufacturer. Interestingly, most of the commodity focussed industries in Vietnam are facing a threat of cheaper imports from China and this has impacted prices negatively over the past year, being the case for both the fertilizer and tire company.

The next day I headed to Binh Duong province, which is about an hour’s drive from HCMC, to meet with a real estate company which develops residential projects primarily in Binh Duong. Though it has some other business such as a toll way project and some commercial real estate projects its, main business activity is in the construction of residential real estate projects. Since Binh Duong and the surrounding areas are seeing a lot of industrial activity due to the economic development of the region and this company can see its real estate projects benefit.

Following this I visited the factory of a local cold drinks manufacturer in District 1 which is a prime location in HCMC. Yes it is surprising to see a factory operation in District 1, but this company is sitting on very valuable land. The company manufacturers a local brand of cold drinks but it does not necessarily compete with Coke and Pepsi as its drinks are not cola but of a different flavour (somewhat like Dr. Pepper in the U.S).

The next day I headed to Dongnai province to meet some more companies. Dongnai is about an hour and a half north of HCMC and on part of the drive I drove parallel to the metro project which is under construction. In Dongnai I met with an infrastructure company, a detergent company and visited the factory of an automotive battery company. The fund holds the automotive battery company and on seeing the factory we continue to be positive on this company given their expansion plans at the existing factory location.

Visit to automotive battery company’s factory

(Source: Asia Frontier Capital)

This was a very informative and educational trip to Vietnam as I got to meet newer companies as well as conduct site visits. Being on the ground is the best way to get a feel of what is going on in a company or the country and where it can be in the long term as we are very positive on Vietnam.

I hope you have enjoyed reading this newsletter. If you would like any further information, please get in touch with me or my colleagues.

With kind regards,

Thomas Hugger

CEO & Fund Manager

Asia Frontier Capital Limited

89 Nexus Way, Camana Bay

Grand Cayman KY1-9007

Cayman Islands

Disclaimer:

This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Iraq Fund, AFC Iraq Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved.

The representative of the funds in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative.

The AFC Asia Frontier Fund and the AFC Vietnam Fund are registered for sale to investors in Japan, Switzerland (qualified investors), Hong Kong & UK (professional investors), Singapore (accredited investors) and USA (accredited investors and qualified purchasers). The AFC Iraq Fund is registered for sale to investors in Switzerland (qualified investors), Hong Kong & UK (professional investors), Singapore (accredited investors) and USA (accredited investors and qualified purchasers)

By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions.

GO TOP