Asia Frontier Capital (AFC) - December 2016 Newsletter |

|||||||||||||||||||||||||||||||||

In this IssueAFC Asia AFC Iraq AFC Vietnam Fund

|

"Know what you own, and know why you own it."

AFC Funds Performance Summary

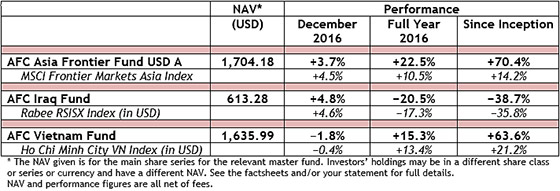

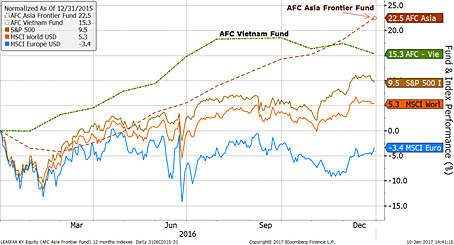

The team at Asia Frontier Capital would like to wish all of our readers a happy, healthy, and prosperous 2017! 2016 was generally considered a difficult year with many surprises, but for Asia Frontier Capital, we overcame these challenges and delivered strong performance. The AFC Asia Frontier Fund closed the year up +22.5% compared with the MSCI Frontier Index which was down -1.3% and the MSCI Frontier Markets Asia Index, which was up +10.5%. The fund is now up +70.4% since inception. The AFC Vietnam Fund returned +15.3% in 2016 compared with the VN-Index in USD, which increased by +13.4%. The fund is now up +63.6% since inception. The AFC Asia Frontier Fund and AFC Vietnam Fund outperformed their benchmarks significantly as well as other major and global indices such as MSCI World, Dow Jones, S&P, DAX, FTSE, MSCI Europe, and the MSCI Emerging Markets Index. Volatility of the AFC Asia Frontier Fund and the AFC Vietnam Fund remained low in 2016, as shown by healthy Sharpe ratios of 1.28 and 1.79 respectively. Performance of the AFC Asia Frontier Fund and AFC Vietnam Fund versus leading indices, all in USD Both funds’ outperformance is sustainable as shown by significant outperformance since inception. The AFC Asia Frontier Fund and the AFC Vietnam outperformed their benchmarks by 9.0% p.a. and +12.2% p.a. respectively since inception. Both funds’ low volatility and absence of losing years shows sustainable, outstanding risk management. Asia Frontier Capital has grown up as the AFC Asia Frontier Fund and AFC Vietnam Fund now have significant track records of 4 years + 9 months, and 3 years respectively. AFC received top accolades for its achievements in 2016:

Asia Frontier Capital increased assets under management “AUM” from USD 35.6 million to USD 49.9 million at the end of 2016, an increase of 40%. Still a small fund management company, we are testament to the well-known view that “small managers perform best”. Asia Frontier Capital was on the “move” in 2016: we moved into a bigger office in the same building in Hong Kong and opened a representative office in Ho Chi Minh City, Vietnam.

BarclayHedge recognized us this month with their Top 10 Award. This award is based on the performance of the AFC Asia Frontier Fund. We won this Top 10 Award in two categories, namely “Emerging Markets Equity – Asia”, as well as “Emerging Markets – Asia”. These accolades further confirm our outstanding abilities as a frontier fund manager, that are proven by great performance at low volatility, but are only possible because of a team of dedicated experts with thorough investment and risk management processes complemented with a superb nose for quality investments, and of course the tireless leg work of being on the ground in the countries we invest in. All in all, 2016 was a great year for a great company with the backup of a professional setup and best-of-breed service providers such as DBS as custodian, Custom House as fund administrators, Ernst and Young as auditors, and Ogier as legal advisors. Asia Frontier Capital is well positioned to be your partner in Asia to help your or your client’s investment portfolios with return enhancement and true diversification through excellent exposure to Asian frontier markets. In this newsletter, we will first have a look at the performance of the AFC Asia Frontier Fund and the manager comments for the month. Then we review the salient events of the past year that have influenced the portfolio. Subsequently we have a more detailed look at the year ahead in the 2017 Outlook. Lastly, we publish the manager comments for the AFC Iraq Fund and the AFC Vietnam Fund. The outlook for each of the funds is positive, for different reasons, but we are confident that we will continue to perform well, and offer our investors a very valuable product that asset managers and individual investors alike can use for the purpose of performance enhancement and reduction of risk in globally diversified investment portfolios. AFC in the Press

Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact Peter de Vries at

AFC Asia Frontier Fund - Manager Comment December 2016

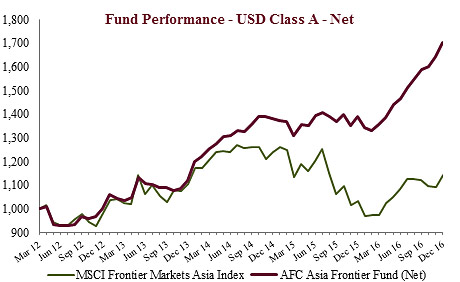

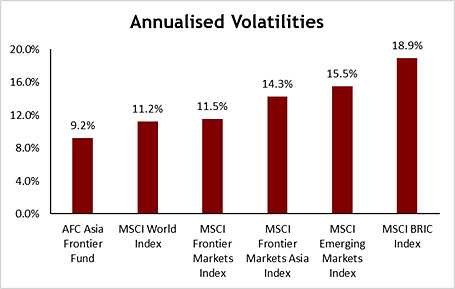

AFC Asia Frontier Fund USD A-shares gained +3.7% in December 2016. The fund outperformed the MSCI Frontier Markets Index (+2.7%) and the MSCI World Index (+2.3%) but underperformed the MSCI Frontier Markets Asia Index which was up +4.5%. The USD A shares achieved a NAV of USD 1,704.18 which is a new all-time high (the previous high was in November 2016 with USD 1,643.60). The performance of the AFC Asia Frontier Fund A-shares since inception on 31st March 2012 now stands at +70.4% versus the MSCI Frontier Markets Asia Index which is up +14.2% and MSCI Frontier Index (+2.8%) during the same time period. The fund’s annualized performance since inception is +11.9% p.a. while its YTD performance stands at +22.5%. The broad diversification of the fund’s portfolio has resulted in lower risk with an annualised volatility of 9.19%, a Sharpe ratio of 1.28 and a correlation of the fund versus the MSCI World Index USD of 0.34, all based on monthly observations since inception. The year ended with another month of positive performance led by Pakistan and Mongolia. Pakistani equities continued their stellar run during the year and the fund’s Pakistani holdings saw a good all-round performance during the month with gains being led by a pharmaceutical company, an oil & gas company, and a cement company. In Mongolia, gains were led by a junior copper producer, a construction material company, a coal producer and a junior oil & gas producer. Besides Pakistan and Mongolia, Bangladesh also aided with performance during the month, with gains led by a consumer food company and a pharmaceutical company. Vietnam was a drag on performance due to a correction in some of the beer-related companies the fund holds. These stocks had rallied well until November due to the listing of Sabeco and Habeco, the parent companies of the beer subsidiaries the fund holds. Though these stocks have corrected, their valuations are still low relative to their parent companies and other consumer companies in Vietnam. Macro numbers in Vietnam still remain healthy with good 4Q16 GDP growth of 6.68%, faster than the 5.93% growth in the first nine months of 2016. Manufacturing continues to grow strongly at 11.9%, the highest growth in the past seven years while foreign direct investment into the country was USD 15.8 billion, a growth of 9% over 2015. These numbers suggest that growth going into 2017 should be steady. The best performing indexes in the AAFF universe in December were Mongolia (+12.3%), Cambodia (+11.4%), and Pakistan (+11.0%). The poorest performing markets were Laos (-1.2%) and Vietnam (-0.6%). The top-performing portfolio stocks this month were all from Mongolia: a gold exploration company (+52.2%), a construction materials company (+51.7%), a coal mining company (+44.0%), and an oil exploration company (+36.6%). In December, we added to existing positions in Mongolia, Pakistan, and Vietnam and partially sold a Mongolian consumer company. We newly added a Mongolian department store and sold a Pakistani meat distributor, a Vietnamese truck producer, and a Mongolian coal company. As of 31st December 2016, the portfolio was invested in 105 companies, 1 fund and held 5.1% in cash. The two biggest stock positions were a pharmaceutical company in Bangladesh (8.7%) and a Pakistani pharmaceutical company (6.4%). The countries with the largest asset allocation include Pakistan (27.0%), Vietnam (26.0%) and Bangladesh (17.8%). The sectors with the largest allocation of assets are consumer goods (30.8%) and healthcare (21.0%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 23.99x, the estimated weighted average P/B ratio was 3.91x and the estimated portfolio dividend yield was 3.11%. For more information about Asia Frontier Capital’s Asia Frontier Fund please click the following links: AFC Asia Frontier Fund – 2016 Performance OverviewThe year began in a very volatile manner as global markets sold off in January 2016 on the back of the first increase in interest rates by the US Fed which finally occurred in December 2015. Besides the worry over rising rates, markets were also panicky about slower growth in China, as well as the impact of significantly lower commodity prices on Middle Eastern economies which led to an equity sell-off mainly driven by sovereign wealth funds from oil producing countries in the first quarter 2016. With slower global growth, especially in developed markets, being a concern going into 2016, the worries over further rate hikes subsided and this position was further strengthened with the shock result of the UK Brexit in June. The Brexit result was the outcome of pent up tension amongst the population due to lack of economic growth and unemployment. These emotions have given rise or strengthened the hand of pro-protectionist, anti-trade, and anti-immigration politicians, which led to Brexit and similarly-aligned political parties gaining strength in other parts of Europe such as France and Germany. Such sentiments were quite prevalent across the Atlantic as well, and this was reflected in the election rally speeches of Donald Trump and Hillary Clinton. These pent-up emotions and sentiments led to the unexpected victory of Donald Trump as US President elect in November. Politically, 2016 was a year of surprises and these events such as Brexit and the election of Donald Trump will have a significant impact on global markets as we move into 2017 and beyond. The other major events during the year were the rally in commodity prices of oil, nickel, copper, and coal as well as another rate hike by the US Fed in December. Commodities started the year weak but the end of 2015 appeared to be the bottom for major commodities such as crude oil and coal which have rallied in price over the past year. Crude oil prices strengthened on the back of expectations of a production cut agreement between OPEC and non-OPEC members which was finalised on 30th November 2016. In this deal OPEC members agreed to cut their oil production by 1.2 million barrels a day, while non-OPEC members, such as Russia, would cut production by 600,000 barrels per day. These cuts took effect from 1st January 2017 and will last six months. Whether all OPEC and non-OPEC members remain committed to these production cut pledges is something to be seen but the fact that this deal was passed could lead to firmer or more stable crude oil prices in 2017 relative to the past two and a half years. Coal prices have also rallied in 2016 as China put in curbs in the first half of the year to cut production by reducing the number of days a mine is allowed to operate, however there has been some relaxation in these restrictions in the past few weeks and coal prices have retreated from their November 2016 highs.

After the election of Donald Trump as US President, it was widely expected that the US Fed would raise rates in December 2016 as Donald Trump had pledged a loose fiscal policy in order to fund new infrastructure projects leading to expectations of higher inflation and interest rates. The Fed raised interest rates by 25 basis points in December 2016 and it is generally expected to raise rates by another three-quarter points in 2017 compared to two expected in September 2016. Rising interest rates would be a concern going into 2017 especially for emerging and frontier market economies with significant amounts of USD debt. That means once again emerging and frontier market currencies would come into focus, similar to the beginning of 2016, on the back of rising US rates. We will discuss more about this in our outlook below. Though there were several uncertainties in the global economies, Asian frontier economies did relatively better than the rest of the world. Amongst the fund’s larger markets, Bangladesh, Pakistan, and Vietnam did well both economically as well as in terms of stock market performance. Bangladesh is expected to show GDP growth of 6.9% in 2016 which is higher than its five-year average of 6.4%. GDP growth has accelerated last year as the political situation has improved over the past eighteen months. The political situation between 2013 and the first half of 2015 was not stable given the animosity between the ruling party, the Awami League, and the main opposition, the Bangladesh Nationalist Party. Blockades or “hartals” were quite common during this period. However, stability has returned in the past eighteen months and this is reflected in better economic growth.

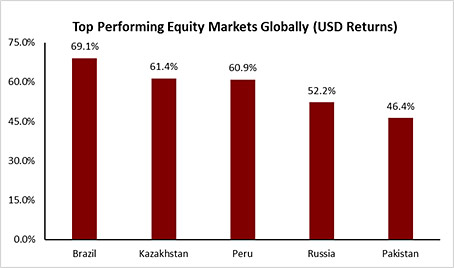

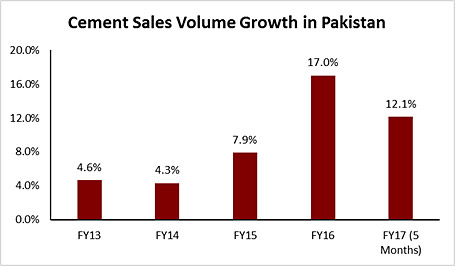

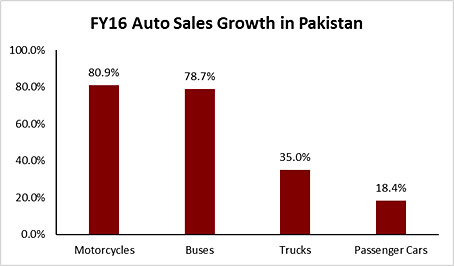

Pakistan has also done well last year, as GDP growth is expected to hit 4.7% in 2016. Though this number does not look very high at a first glance relative to other frontier and emerging markets, it needs to be seen in context of an average growth rate of only 3.6% between 2010 and 2015. Continuing the positive trend from 2015 there was a marked improvement in various indicators such as cement dispatches and automobile sales which were backed by improved law and order. Historically low interest rates, lower commodity prices, and the execution of the China Pakistan Economic Corridor “CPEC” has led to improved economic prospects over the past year and this was reflected in the stock market performance as well, with the KSE 100 rallying by 46%, making it one of the top performers globally.

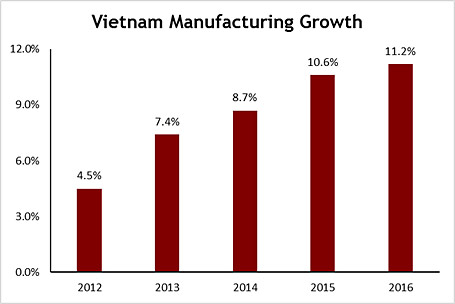

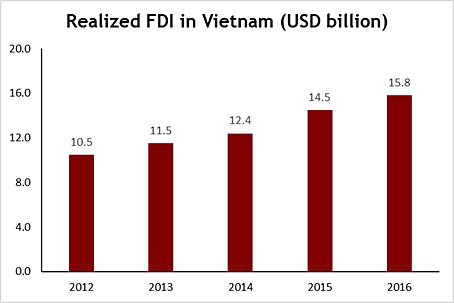

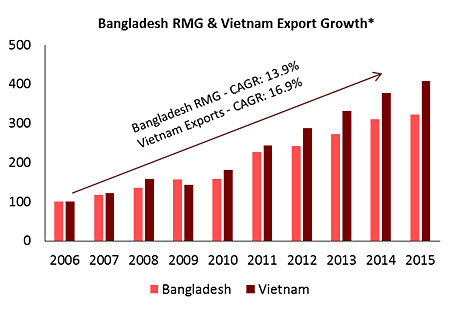

Vietnam continued to deliver robust economic growth and, had it not been for lower crude oil prices, GDP growth for the year would have been higher than 6.2%. The manufacturing sector was the major growth driver in 2016 and grew by 11.9%. The growth of the manufacturing sector over the past few years reflects the attraction of Vietnam as a low-cost manufacturing base backed by a stable political environment and a young, educated, and highly motivated workforce. This is reflected in the FDI numbers which clocked in at USD 15.8 billion, with the largest contribution from South Korea. This is not surprising given that Samsung and LG now have large manufacturing facilities in Vietnam, with Samsung producing 50% of its mobile phones in Vietnam. Samsung has so far invested USD 15 billion into the country. The Trans Pacific Partnership (TPP) would have increased foreign investment into the country even further, but it was widely assumed that this agreement would not go through given the anti-trade pre-election speeches by Hillary Clinton and Donald Trump. Despite TPP not going ahead, Vietnam still attracted sizeable FDI inflows and this is because it offers a lower cost alternative to China which has significantly higher wages compared to Vietnam. The end of the year also saw listings by Sabeco and Habeco, the number one and number three breweries in Vietnam by market share. 2016 saw quite a few new listings of state owned companies and the same is expected in 2017 as the government looks to reduce its ownership in various companies in order to raise capital to finance its budget deficit. Given the stable economic performance for the year, the Ho Chi Minh VN Index was up 14.8% during the year.

Given the stable to improving economic performance of Bangladesh, Pakistan, and Vietnam, these markets were already the fund’s top three markets by weight at the end of 2015 with Vietnam having the highest weight, followed by Pakistan and Bangladesh. The year ended, however, with Pakistan having the highest weight in the fund due to a combination of price appreciation and new stocks added. However, price performance was the main reason for Pakistan becoming the largest country allocation by the end of 2016. The major contributors to price appreciation within the Pakistani portfolio were a pharmaceutical company which is now the second biggest position in the fund, an oil & gas explorer, a consumer beverage company (which we sold in September 2016), a cement company, and a motorcycle company. The fund’s other Pakistani holdings also did well but the above were the top 5 performance contributors within Pakistan. In our review and outlook for 2016 we wrote that we were positive on the prospects for Pakistan and therefore we invested in 10 new positions. These positions were across the consumer staples, consumer discretionary, and financials sectors which gave the fund exposure to the potential cyclical upturn in the economy as well as exposure to some strong consumer franchises. We also exited three positions in Pakistan: a consumer beverage company, a media company, and a textile company. We exited the consumer beverage and media companies due to corporate governance issues and we sold the textile company due to poor textile export numbers for Pakistan. In hindsight, this was an error, as the stock was cheap in terms of its P/E multiple. The stock has rallied since we sold. We win some, we lose some, but more importantly we live and learn from our mistakes. Vietnam continued to have the highest weight in the portfolio for the majority of 2016 and we have been positive on Vietnam since the inception of the fund. In the review and outlook for 2016 we had mentioned that Vietnam was going through a cyclical upturn and therefore we had increased the weight of cyclical companies in 2015 and continued to do so in 2016. This helped with performance as the three of the top six contributors to performance in Vietnam were cyclical companies: a construction company, a plastic pipe manufacturing company, and a manufacturer of automotive batteries. We exited the plastic pipe manufacturing company in 2016 on valuation grounds as well as due to increasing competition in this segment which could impact profit margins in the coming few years and expected higher oil prices. Within the cyclical space, we also increased our weight in a cement company and a construction services company. Other top performers within Vietnam were a pharmaceutical company, a stationery company (which the fund exited during the year on valuation grounds), a consumer food company, and a beer company. The beer company did well for the fund in the last quarter of the year due to the listing and divestment news of its parent company. The fund has been accumulating this position since the fund’s inception as its valuation was extremely attractive and this long-term thinking has led to solid gains from this stock in 2016. During the year, we also bought four new companies, namely a real estate developer, a toll road/real estate developer, a general insurance company, and an industrial parks developer. With consistent GDP growth expected over the next few years for Vietnam, we expect these cyclical names to also do well. Besides the pipe company and stationery company that the fund exited, we also sold an agricultural seed company, a cement company based in North Vietnam, a consumer beverage company, a commercial vehicle producer, a pesticide company, and a retail jewellery chain. We exited some of these names due to deteriorating fundamentals or due to the position becoming very small and not adding value to the portfolio anymore. In Bangladesh, we did not make any changes to our large positions in the country but bought into a paint company and a housing finance company, both which have good long term potential given increasing disposable income levels and urbanisation in Bangladesh. The two leading performers in Bangladesh were a pharmaceutical company (the fund’s biggest holding) and a consumer food company which the fund entered into in December 2015. We exited four companies: a hair oil distributor, a textile company, a consumer goods company, and a shoe manufacturer. These exits were made due to either deteriorating fundamentals or high valuations. One country where we reduced our positions significantly was Sri Lanka where the fund’s holding in the country has come down from 9.8% at the end of 2015 to 1.9% at the end of 2016. The macro situation in Sri Lanka was not very positive in 2015 itself and we felt that it would not improve significantly in 2016 as well due to the issues surrounding balance of payments, foreign reserves, and policy making. Hence, we gradually reduced most of our positions in Sri Lanka and now hold only three companies: a consumer-focused conglomerate, a tobacco company, and a consumer beverage company. Reducing our weight in Sri Lanka has helped with overall performance as the Sri Lankan market fell by 10% in USD terms in 2016. These funds were allocated to more attractive opportunities in Pakistan and Vietnam. Within Mongolia, the fund’s exposure to commodity-focused Mongolian companies has paid off on the back of increasing commodity prices and some of these names generated handsome returns in 2016 led by a junior gold explorer, a junior copper explorer, and a coal mine. The fund has also slightly increased its exposure to Myanmar by investing in two investment holding companies which are making investments across diverse sectors in Myanmar. Overall, it was sound country, industry, and stock allocation that led to significant outperformance over the benchmark. The fund returned 22.5% in 2016 compared to 10.5% for the MSCI Frontier Markets Asia Index. Stock selection over the past 24 months has led to this outperformance as many of the stocks which drove performance in 2016 were also part of the portfolio in 2015. On a stock specific basis, performance was driven by stocks which were part of the Top 20 positions in 2015 and 2016 as well as other positions which came into the Top 20 due to price appreciation. This reflects our strategy of holding onto stocks for the long run and not changing the portfolio every few weeks. In terms of industry allocation, healthcare became the sector with the highest weight and this was due to the price appreciation of the fund’s pharmaceutical company holdings in Bangladesh, Pakistan, and Vietnam while we also added a hospital chain in Pakistan, which increased the weight of the healthcare sector. The weight of the consumer staples sector came down during 2016 as we exited a Pakistani consumer beverage company which was a large holding for the fund. We also reduced the exposure in two Sri Lankan companies, a consumer-focused conglomerate and a tobacco company. The weight of the consumer discretionary sector has come down as we sold a Vietnamese stationery company which was one of our larger positions in Vietnam. The weight of the materials and industrial sectors decreased as we sold a Vietnamese plastic pipe company, an agricultural seed company, and a Sri Lankan construction company. The fund’s weight in the financial sector increased due to the purchases of one commercial bank, one insurance company, and one leasing company in Pakistan, while in Bangladesh we bought a mortgage finance company. In Vietnam, the fund entered into two real estate companies and a general insurance company whilst also increasing its exposure to a Myanmar focused investment holding company. The fund’s exposure to the energy sector has also increased slightly as we increased exposure to a Pakistani oil & gas explorer. In terms of country allocation, as mentioned previously there was no significant change in the top 3 markets. Therefore, we did not make any significant changes to the country allocation over the past year but used a top down approach to identify the more attractive markets and selected stocks which we believe will deliver outperformance over the long term. It is important to note that we have followed a benchmark and market cap agnostic approach since the fund’s inception and this has led to outperformance since inception. We are constantly looking for new investment ideas which brokers and/or other institutional investors either ignore or overlook. This is backed by continuous on the ground research which we believe is important as it helps us to find new ideas as well to keep our ears to the ground. In 2016 we conducted 198 face to face meetings with management teams in Bangladesh, Cambodia, Iran, Papua New Guinea, Pakistan, Laos, Mongolia, Myanmar, Sri Lanka, and Vietnam. Also, the fund has managed to exhibit lower annualised volatilities relative to MSCI indices and this is due to our diversified approach to managing the portfolio. Though the portfolio appears to hold a large number of positions, we would like to add that we are not just focusing on diversifying, since the fund’s top 30 positions account for 68% of the portfolio which also reflects our approach of taking larger positions in the companies we have a higher level of conviction in.

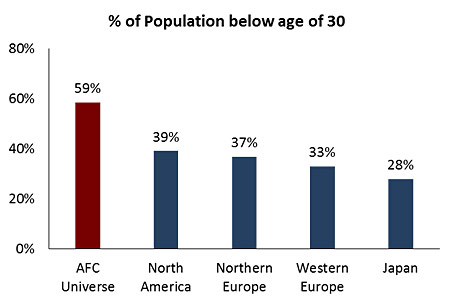

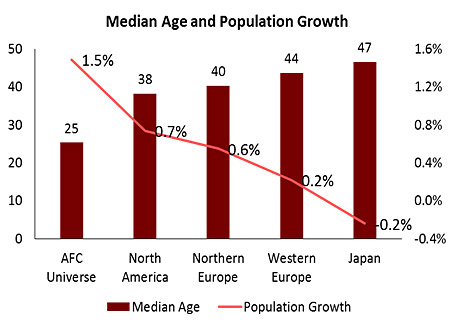

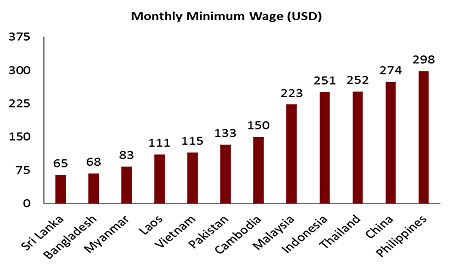

It was stock selection and country/industry allocation that led to outperformance in 2016 and we hope to get those factors right or at least in the right balance in 2017, as well as in the future in order to deliver consistent returns to our fund holders. AFC Asia Frontier Fund – 2017 Outlook2017 begins with concerns similar to those at the start of 2016: rising interest rates in the US and the impact on emerging and frontier market currencies. Added to these concerns is the start of Donald Trump’s presidency, which has raised some worry given his comments about free trade. The US Fed raised rates by 25 basis points in December 2016 and another three hikes are expected in 2017. Similar to 2016, these rate hikes raise the issue of currency depreciation in emerging and frontier markets and will also raise financing costs of USD debt held by corporates and sovereigns. In our fund universe, most of the companies the fund holds do not have any USD debt on their balance sheets and from a government debt perspective most of the USD debt is long term in nature so the impact will not be that significant. Besides rising US rates which could lead to some pressure on currencies, possible trade issues between the US and China could lead to a depreciation of the Chinese Renminbi and this could lead to depreciation of regional currencies similar to August 2015. Besides trade and US interest rate related currency risks, higher crude oil prices could impact current accounts which could also impact currencies. From our larger markets, Pakistan and Sri Lanka are expected to close 2016 with a current account deficit of ~1.5% which could put some pressure on their currencies, while Bangladesh will close 2016 with a slight deficit and Vietnam should close 2016 with a current account surplus. Therefore, given the combination of rising US interest rates, trade issues, and pressure on current account deficits, 2017 could see some pressure on currencies for our larger markets but it should not be significant as their current account deficits are not severe and they are not expected to face any major flight of capital. One of the major drivers of foreign reserves for our larger markets has been remittances, and most of these remittances, especially for Bangladesh, Pakistan, and Sri Lanka, are coming from the Middle East which is facing the impact of lower crude oil prices. Given the economic slowdown in the Middle East due to lower oil prices, a significant decline in remittances going forward to Bangladesh and Pakistan would be negative not only for the current account but also for disposable incomes, which could impact consumer spending. Geopolitically, a major issue which could flare up once Donald Trump becomes President is the South China Sea issue and this could create tensions in the region. It is too early to say what steps the new President will take regarding the extremely delicate situation in the South China Sea and generally towards China and Taiwan. Since we are generally positive on the three top country allocations in our portfolio, we do not expect to make any significant changes unless we turn very positive on Sri Lanka. Having said that, we will also watch the evolving near term macro environment and make changes accordingly. Though 2017 has started on an uncertain note surrounding the policies of the new US President, our conviction in the long-term story of Asian frontier markets is not diminished as these countries have very favourable demographics backed by rising disposable incomes, are going through political reform, and are benefitting from increased foreign investment due to lower wages relative to China. Further, companies in the Asian frontier markets are still relatively under-researched relative to larger emerging markets and therefore offer convincing long term opportunities. Compared to developed markets, the AFC Frontier Universe has a much younger population, growing at a faster rate:

Low wages in Asian frontier economies offer

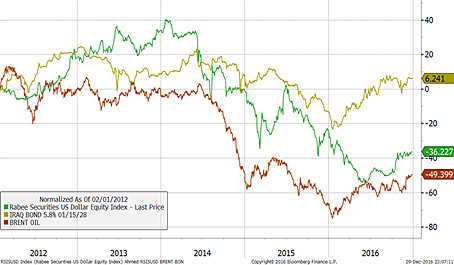

Outlook for Key MarketsBangladesh 2016 was a much more politically stable year for Bangladesh relative to the last few years which saw numerous road blockades “hartals” and this stability has led to better economic performance. We continue to like the consumer related story in Bangladesh due to favourable demographics backed by rising income levels (which are still lower than India, Pakistan, and Sri Lanka) and increasing urbanisation. As a result, all of our holdings in Bangladesh are currently consumer or consumption related and we do not expect any significant change in these holdings. The macro scenario for Bangladesh is also stable with a manageable fiscal deficit of ~4% of GDP and foreign reserves of USD 31 billion which is ~9 months of import cover. Further, the government is planning to undertake infrastructure projects which should also aid economic growth as such infrastructure investments are badly needed. One sore point for the year was the extremist related incidents, but the government will look to control this situation given the importance exports play with respect to employment as well as economic growth. 2017 should also be stable but, with elections expected to be held in the beginning of 2019, some amount of political noise in 2018 would not be surprising. These kinds of situations do not change our long-term view on Bangladesh and we remain positive on the country. Cambodia Cambodia continues to see an increase in FDI with construction being the most dynamic engine to growth, where USD 7.2 billion in commercial construction was approved in the first eight months of the year, double the level of 2015. China has become an important investor in the country and is also largely responsible for bolstering the tourism industry. During the year, 900,000 Chinese visited the Kingdom, a 20% increase versus 2015. The country continues to increase connectivity with its neighbours as recent direct flights from Phuket, Thailand to Siem Reap and from Ho Chi Minh City, Vietnam to Sihanoukville have been established. This is in addition to a third undersea telecommunications cable being proposed and the government encouraging the largest conglomerate in Cambodia to launch the nation’s first satellite. The Kingdom also signed its first ever double taxation treaty with Singapore and one with China has been drafted. During the year, the Cambodian Stock Exchange saw one new IPO, the Phnom Penh SEZ, leaving the exchange with 4 listed companies. We currently have a small exposure to Cambodia via a resource explorer listed in Australia. Iraq The fall of Mosul and a third of the country in June 2014 to ISIS was a major factor behind the brutal bear equity market over the last two years. The double whammy of the cost of war and collapse in oil prices battered the economy and led to a market decline of around 68%, as measured by the Rabee Securities' RSISUSD Index, from the January 2014 Peak to the May 2016 bottom. The last leg of the decline, i.e. the first five months of 2016, was relentless especially after oil prices hit multi-year lows in late January 2016, with persistent local & foreign selling including the liquidation of a major Iraq dedicated equity fund. The last leg was so savage that it accounted for over a third of the total decline from the peak in 2014. Plus, it was in sharp contrast to the rallies of +84% & +36% respectively in oil prices and Iraq’s Euro Dollar Bond (USD 2.7 billion, issued 2006, due 2028 with a 5.8% coupon) by the end of May after hitting the January multi-year lows. The historical correlation, however, reasserted itself with a sharp bounce in June followed by a period of consolidation during the summer months and a sharper bounce in October. Going forward, with a recovery in oil prices and gains being made by the Iraqi military against ISIS, the outlook for Iraq could see an improvement. Laos Not much has changed in Laos over the past year. The government still runs a fiscal deficit of 3% and a current account deficit of 18%. These deficits are being run due to higher government spending and increasing imports of petroleum products and consumer goods while experiencing lower commodity exports, namely electricity and base metals. On 25th December 2016, Laos officially began construction of the 427 km Laos-China railway project linking the Laotian capital, Vientiane, with the Chinese border. The USD 5.8 billion construction cost is being subsidized by a soft loan from the Chinese government, but with a GDP of only $12.5 billion it remains to be seen how profitable the rail will be for Laos and how the country intends to service its debts. We do not expect to increase our equity exposure to Laos (only 5 stocks are still traded in Laos) unless there is clarity on how the government expects to decrease its deficits. Maldives Political unrest has been an issue for the Maldives since 2015 and this continued to negatively impact tourist arrivals from certain countries such as China which accounts for 27% of arrivals. During the year, we sold two of our Sri Lankan hotel listings which get the majority of their revenues from the Maldives. Given the political instability, the fiscal situation of the country is also not in the best shape and the outlook for the country will depend on improved political stability. Mongolia Mongolia experienced a turbulent year in its economic and political landscape whereby the opposition Mongolian People's Party (MPP) won Parliamentary elections on 29th June 2016, winning 65 of 76 seats, followed by a landslide in provincial elections on 19th October. The MPP being more pro-business than the previous Democratic Party, they followed their Parliamentary win by raising the Policy Rate by 450bps on 18th August to stem the Mongolian Tugrik's decline. The government has also re-engaged negotiations with a consortium comprised of Mongolian Mining Corp. (listed in Hong Kong), Sumitomo, and Shenhua to develop the 7.5 billion ton Tavan Tolgoi coal basin. A deal with the consortium will result in a new source of FDI for the country which is desperately needed. This next year will be telling as the country continues the process of bottoming out, Oyu Tolgoi Phase II gets going and Mongolia executes a rollover of its sovereign debt. This past year also saw the establishment of the "Economic Corridor" between China, Mongolia, and Russia where 32 projects were approved to be implemented. We have exposure to consumer, industrial, and junior mining stocks in Mongolia and especially the mining stocks helped with performance in 2016 and we expect to hold on to most of them. Myanmar On 1st February 2016, Myanmar began a new era with the opening of a new session of Parliament with Aung San Suu Kyi's National League of Democracy in control. The new government has been successful in restructuring government ministries and enforcing strict measures on civil servants regarding corruption. Due to the NLD's actions, Myanmar saw the US lift all remaining sanctions on 7th October which should benefit growth going forward. On the economic front, GDP growth has remained robust, estimated to be 7.8% while there is an increasing housing stock in Myanmar's major cities and 3G cell coverage is becoming ubiquitous nationwide. However, the year also saw the NLD focus on creating stability in the semi-autonomous regions which backfired as fighting increased in Shan, Kayin, and Kachin States, while the situation in Rakhine State increasingly degraded. The year also saw the Myanmar Kyat (MMK) depreciate by 3.6% as the country experiences a current account deficit due to a continued rapid increase in imports. Of course, these are signs of a young democracy and Myanmar's positives far outweigh the negatives. A long-term growth story, Myanmar is an increasingly attractive investment destination which we believe will continue to offer new opportunities listed on overseas exchanges while we anxiously await passing of the Companies Act and new Foreign Investment Laws which should pave the way to enable foreigners to begin trading on the Yangon Stock Exchange (there are currently three stocks listed) and this will enable us to increase our exposure to the growth opportunities in Myanmar. Pakistan Pakistan became the fund’s largest country weighting as of December 2016, and this was due to price appreciation as well as the addition of new holdings. In last year’s annual outlook, we had written that we are positive on the outlook for Pakistan and hence we increased the number of positions in the country. Our weights in the consumer discretionary, healthcare, and cement industries performed very well in 2016 and we are positive on the outlook going into 2017 as well due to stable interest rates, positive consumer sentiment, a pickup in loan growth, and an improving security situation. China Pakistan Economic Corridor (CPEC) related investments are also underway and this will improve the power situation in the country going forward which can increase GDP growth as the current power deficit is cutting 1-2% from GDP growth. If the power situation improves and there is continued security and political stability, GDP growth can be greater than the 5% it is projected to be over the next few years. We do not expect to change our existing positions in Pakistan significantly, and we could look to increase our exposure to Pakistani banks in the future as interest rate increases backed by loan growth should help their profitability going forward. Politically there could be some more noise in 2017 as national elections are due in 2018 which could lead to some nervousness in the market. Though the incoming US President has not made any adverse remarks towards Pakistan, any significant change in US foreign policy could lead to near term uncertainty. Last year we had written that Pakistan could be the dark horse over the next few years and we still maintain that position. Papua New Guinea Lower commodity prices continued to impact the macro economic outlook for the country and GDP growth is expected to be soft in 2017. Lower commodity prices have also had a negative impact on the current account and the country’s foreign exchange woes continued with help being sought from the IMF, but no deal has yet been announced. On a positive note, Exxon Mobil made a new gas discovery which is in addition to its existing gas project which commenced operations in 2014. We do not expect to increase our exposure to Papua New Guinea in 2017 given its fiscal and especially monetary situation. Sri Lanka As we had expected, 2016 was a tough year for Sri Lanka due to the macro environment, as well as the policy issues it was facing. The new government was faced with a large fiscal and current account deficit and therefore had to take strong measures to improve this situation via increases in taxes and duties which could impact consumer discretionary spending in the first half of 2017. These tax measures were also required under the agreement to receive IMF funding in order to overcome the balance of payments related issues. The government also came down heavily on the tobacco and alcoholic beverage sectors by increasing duties and this is now beginning to have a negative impact on the organised tobacco sector in terms of growth rates. On the positive side, infrastructure related projects which were stalled when the new government came to power were kickstarted again. Valuations of certain companies in specific sectors are looking attractive which warrants another look at the country later this year. Vietnam Positive economic momentum continued in Vietnam as GDP growth clocked in at 6.2% led by manufacturing growth of 11.9%. It is not surprising to see these strong growth numbers given the cyclical upturn the economy has been going through over the past few years, backed by healthy foreign direct investment. As a result, we continued holding and increased our weight of cyclical companies and this helped with performance. Despite slower global growth Vietnam exports have still done relatively well with growth of 8.6% in 2016 but there will be some amount of uncertainty until Donald Trump lays out his trade plans since the US is Vietnam’s biggest export market. Exports and foreign direct investment have been one of the important factors for strong manufacturing growth in Vietnam and any significant deterioration in global trade due to extreme US trade policies could lead to a drop-in exports and foreign investment which can be a risk to economic growth. This obviously is a worst-case scenario but until the new US administration lays out its plans for trade the uncertainty would persist. Besides this near-term uncertainty, Vietnam is still amongst our favourite markets due to the attractive demographics, lower cost of labour relative to China, and attractively valued companies across the small, mid, and large cap space. New listings at the end of 2016 as well as in 2017 will increase the investment universe. AFC Iraq Fund - Manager Comment December 2016

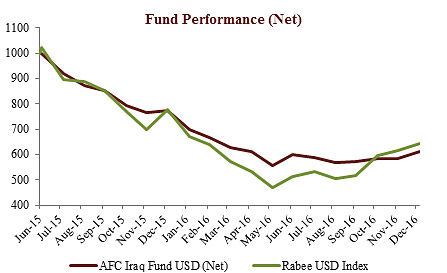

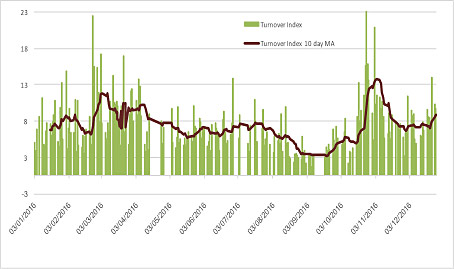

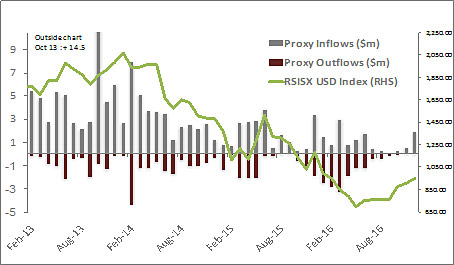

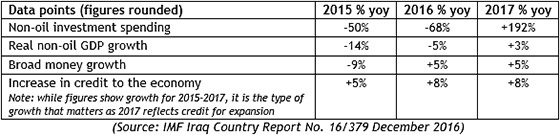

AFC Iraq Fund Class D shares returned +4.8% in December, in-line with the Rabee RSISX USD Index (RSISUSD), which returned +4.6% in USD terms. The fund has underperformed the RSISUSD by -2.9% since inception. The market continued to recover with turnover slowing somewhat but still at the higher end of the range for 2016 (see chart below of turnover net of trades by strategic investors and insiders). The improvement in market sentiment that started a couple of months earlier was evident through the ease of absorbing the giant auction of Asiacell at over 4 times the average daily turnover after the courts mandated that North Bank, a bank that is being unwound, liquidate its holding of Asiacell (valued at the time of announcement at about USD 4.8 million, in an auction in mid-December to satisfy debts of a creditor). Index of turnover on the Iraq Stock Exchange (ISX) (green), Foreign inflows turned decidedly positive with some funds seeing inflows for the first time in over two years, reflecting the changed sentiment towards Iraq as the chart below of proxy portfolio flows indicates. However, this is still early in the process and just a fraction of the levels of 2013 and 2014. The change in sentiment extended to international media coverage which has shifted from the overstated risk perception of the last two years into one highlighting opportunities and investment potential that the country presents post-conflict. Proxy portfolio flows on the Iraq Stock Exchange (ISX) AFC Iraq Fund Performance Review 2016 "What we call the beginning is often the end. And to make an end The year started ominous enough for the Iraqi equity market and the AFC Iraq Fund in that the backdrop to financial markets was weak with fears of China’s economic slow-down and its effects on global markets, commodities, and commodity producing countries. Oil price declines of the last months of the prior year intensified with fears that it would hit USD 10 a barrel and stay there for an indefinite period. Such fears were fed by reports from the International Energy Agency (IEA) that the world was drowning in oil with decreasing demand and increasing supply. Iraq, highly dependent on oil, was faced with collapsing revenues for the second-year running while its expenditures were increasing by the demands of the war against ISIS. The government’s consistent response was to underspend on wages and pensions, goods, and services and investments. In particular, non-oil investments contracted by -68% on the back of -50% contraction in 2015 resulting in non-oil GDP contracting by -5% following a -14% contraction in 2015. The effects on the economy were huge as: (1) the government is the largest employer in the country, directly or in-directly through State Owned Enterprises (SOEs), employing over 50% of the working population; and (2) it is the largest player in the non-oil economy with its orders/contracts driving multiple industries. Consequently, liquidity in the economy dried up through 2015 and 2016 with negative consequences on local liquidity in the stock market. The equity market, having ended the prior year down -23%, as measured by Rabee Securities RSISUSD Index, was under severe pressure from the lack of local liquidity with forced selling while foreigners were mostly net sellers which was magnified by two un-related events that accelerated the market’s collapse in the first 5 months of the year. The two events were: (1) a liquidation of a sizable Iraq Fund (about USD 12 million by end of January); and (2) the sale of HSBC’s 9% holding in Dar Es Salaam Bank as part of its regional retrenchment (about USD 8 million by the end of 2015). The first 5 months of the year accounted for a third of the market’s total decline of -68% from the peak in 2014 until the multi-year lows in May 2016. Ultimately, the market’s historic correlation with Brent prices and Iraq’s Euro Dollar Bond (USD 2.7 billion, issued 2006, due 2028 with a 5.8% coupon) reasserted itself with a sharp bounce in June followed by a period of consolidation during the summer months and a sharper bounce in October as the market started to discount the end of conflict with the launch of the battle to liberate Mosul (see chart below). The market continued its recovery and building momentum to year end. Rabee Securities’ RSISUSD Index (green), The year also marked the effective end of ISIS as an occupying force with coordinated actions by the international coalition and Kurdish & Iraqi forces in Syria & Iraq. Momentum picked up in early summer with the liberation of the city of Fallujah, ISIS’s first stronghold in early 2014, and culminated in the battle to liberate Mosul in October. The Mosul offensive started better than expected from both military and humanitarian standpoints with civilian casualties, mercifully, far less than feared. However, the battle entered the ugly phase as it progressed toward the heavily populated city center with intense street fighting and increased casualties. However, neither the fears of fierce destructive battles nor sharply inflamed sectarian tensions materialized which is positive for the future of the country. The government, which performed better than feared over the last two years given the inherent conflicts at its formation, still faces significant challenges on two fronts. The first is the stalled reform process and the unmet demands of nationwide demonstrations, while the second is continued political instability which intensified with parliament’s impeachment of the Finance and Defence ministers. As odd as it might first seem, this has sown the seeds of future political stability for the country: these impeachments were only possible because the sectarian alliances since 2003 of Kurds, Sunnis and Shias have begun to unravel in the last few months leading to potential cross-sectarian alliances. While these are still tenuous and far from stable, nevertheless they are promising going forward. Countering the government’s challenges is the support that the country is getting from its international sponsors anchored by the IMF’s Stand-by Arrangement (SBA) of USD 5.4 billion as part of USD 11+ billion of loans/aid to the country. These would be on top of aid announced for the reconstruction of the ISIS liberated territories. The AFC Iraq Fund outperformed the market since launch initially, yet the same attributes that helped it outperform were behind its underperformance later on, during the market's initial recovery phase characterized by sharp rallies in lower priced and lower quality but high beta stocks. However, this should dissipate as high-quality stocks resume market leadership. The fund's holdings are high-quality companies whose earning power/assets/franchises held well during the last two years while the growth in their earnings and asset values is expected to outpace the economic recovery post-conflict, which should lead to a sustainable long-term out-performance of the market by these companies. AFC Iraq Fund Outlook 2017 "You can only predict things after they have happened" The catalyst for a new bull market in the Iraqi equity market was set by the battle to liberate Mosul in October. The market, as measured by the RSISUSD Index, with the worst behind it, started the long process of discounting the end of conflict and the associated significant economic benefits with the reallocation of military spending to the local economy and the investment spending to rebuild. The economic benefits will unfold through the substantial expansion in non-oil capital investment spending estimated to be up +192% yoy in 2017 after contractions of -68% in 2016 and -50% in 2015. While, from a low base and below trend, it nevertheless will have a substantial impact on the market down the road and will provide the fuel that will drive it further and in the process provide the rationale for reasserting its historic correlation with Iraq’s Euro Dollar Bond and Brent Crude (chart in earlier section). In 2016 Brent was up +63.1%, the Bond up +23.3% while the market was down -17.3% implying significant catch-up potential medium-term. Ultimately, the Bond’s +6.2% rise above the early 2012 levels suggests that the catch-up process has a meaningful multi-year recovery potential. These figures are provided by the latest IMF Iraq Country Report (December 2016). As the government is the biggest player in the economy and its investment spending drives non-oil GDP, the recovery in non-oil capital investment spending will drive a growth of non-oil GDP of +3% in 2017 vs. contractions of -5% & -14% in 2016 & 2015 respectively. The same is forecasted for the expansions in broad money & credit to the economy as the table & charts below illustrate.

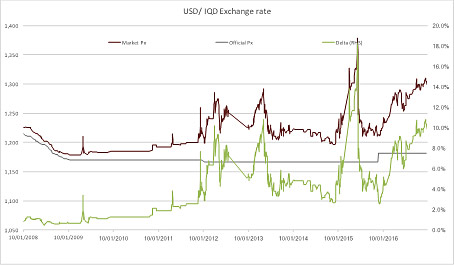

These figures assume zero growth in oil production & exports for 2017-2021 and oil prices of USD 42 in 2017, increasing by an average of USD 2 a year in 2018-2021 (Iraqi oil is sold at a discount to Brent). Hence, there is significant room for expansion in non-oil GDP should Brent prices sustain levels of above USD 50 for 2017. Once again, while the figures are modest in absolute terms, it is the rate of change from negative to positive that will have the greatest impact on liquidity in the economy and ultimately the stock market. The expansion in non-oil spending will likely be bolstered by the reversal of net outflows of FDI’s and foreign portfolio investments. While figures for 2016 are months away from being published, Moody’s reported in June that “In 2015, year-over-year net foreign direct investment inflows declined by -30% to USD 3.2 billion, and net portfolio inflows dropped by -86% to about USD 630 million. Net other investment outflows nearly doubled to about USD 8.5 billion”. (Note: the definition used by Moody’s of portfolio inflows encompasses a wider universe than the equity market). The same data points were likely to have been neutral at best throughout 2016 with a pick-up towards year end. As reported in the December review section earlier, foreign portfolio inflows turned decidedly positive with some funds seeing inflows for the first time in over two years (see chart of proxy portfolio flows). Furthermore, strengthening oil prices and government finances should lead to a recovery in the market price of the Iraqi Dinar (IQD) vs the USD. The spread between the exchange rate for the market price of the IQD vs the official price increased from the normal 2-4% premium to about a 10% premium due to lower oil revenues and the pressures on government finances. Official IQD/USD rate (grey), Market IQD/USD rate (red), However, the old saying “bull markets climb a wall of worry” applies to Iraq, but with many such walls to climb. To name a few: delayed execution of investment spending, continued political squabbling and instability, weakening oil prices, and potential new regional conflicts. Hence, the recovery will likely be in fits and starts with plenty of zig-zags along the way as liquidity is still scarce with a time lag before it can filter down into the economy. But, a change of direction is at hand with the opportunity to acquire attractive assets that have yet to discount a sustainable economic recovery. As of 31st December 2016, the AFC Iraq Fund was invested in 14 names and held 3.4% in cash. As the fund invests in both local and foreign listed companies that have the majority of their business activities in Iraq, the countries with the largest asset allocation were Iraq (97.2%), Norway (2.4%), and the UK (0.4%). The sectors with the largest allocation of assets were financials (52.9%) and consumer staples (23.2%). The estimated trailing median portfolio P/E ratio was 13.11x, the estimated trailing weighted average P/B ratio was 0.96x, and the estimated portfolio dividend yield was 2.20%. For more information about Asia Frontier Capital’s Iraq Fund, please click the following links: AFC Vietnam Fund - Manager Comment December 2016

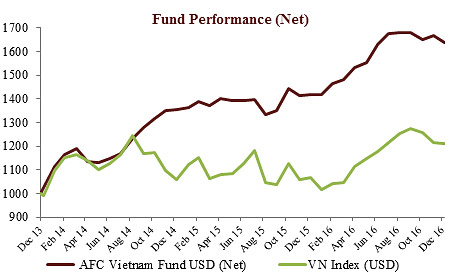

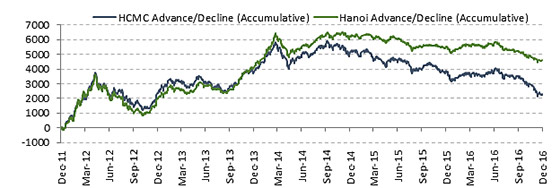

The AFC Vietnam Fund returned -1.8% in December with an NAV of USD 1,635.99, bringing the year to date net return to +15.3% and the net return since inception to +63.6%. This represents an annualized return of +17.3% p.a. By comparison, the December performance of the Ho Chi Minh City VN Index was down -0.4% while the Hanoi VH Index decreased by -1.0% (in USD terms). Since inception, the AFC Vietnam Fund has outperformed the VN and VH Indices by +42.4% and +54.9% respectively (in USD terms). The broad diversification of the fund’s portfolio resulted in a low volatility with a standard deviation of 9.37%, a Sharpe ratio of 1.79, and a correlation of the fund versus the MSCI World Index USD of 0.30, all based on monthly observations since inception. The past few weeks have proven to be very difficult. Like many other currencies around the globe, the Vietnamese currency lost around 2% against the US dollar since Trump’s victory and has been trading on its upper limit for some time now. Despite the listing effect on the index from Sabeco, the Ho Chi Minh City Index hardly changed with -0.4% while the index in Hanoi declined by -1.0%. Foreign selling affected some of our holdings which resulted in an underperformance for the month. Market developments 2016 was an interesting year for emerging and frontier markets, Vietnam included. Despite a positive turning point of the relative performance to developed markets earlier in the year and strong performing Vietnamese shares in general in the first six months, the stock market went into a long period of consolidation in the second half of the year. But if we take into account two isolated special situations which impacted the main index in HCMC by about 10%, then 2016 was a rather unimpressive year without any significant gains. The broader market was even negative, with Hanoi, where mostly smaller stocks are listed, down 0.9% for the year in USD terms as the advance / decline ratio on both exchanges showed a strong deterioration, which means that only a limited number of stocks gained while the majority lost ground. After Trump’s victory, foreigners were selling more than USD 100m within a few weeks and we saw some forced selling in many stocks, including some of our holdings, which brought especially small caps into extreme oversold territory, which is usually a very good sign for an imminent upturn. Over the last few days we saw this selling already fading and foreigners were already net buyers for the first time in weeks. If this will continue, we are quite confident that we will see a strong recovery in 2017.

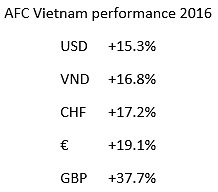

Despite the difficult market environment, we were able to achieve a solid return for our investors for the third consecutive year. Like last year, due to the strong USD, the performance is even better for our non-USD investors as this overview shows:

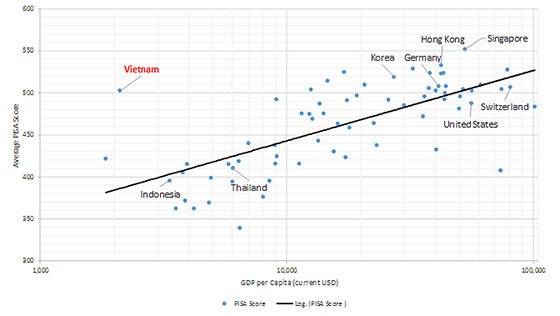

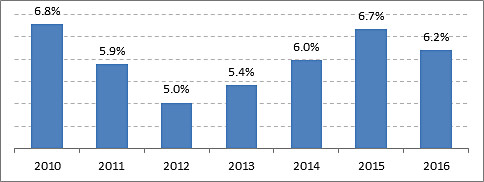

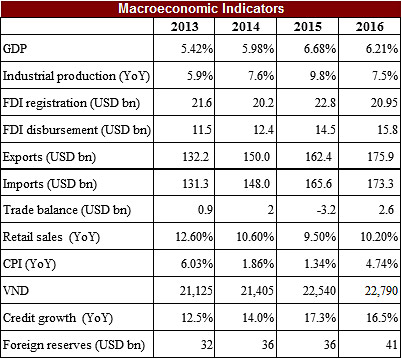

The fundamental story in Vietnam has not changed with mostly encouraging economic numbers for 2016. Even with TPP not happening as planned, Vietnam and the region are actively working on numerous trade pacts as previously reported. The positive economic development and rising income levels should lead to an increased interest in the local stock market as more brand names are being listed. The stock market offers one of the few legal ways to make investments, or better said, one of the few legal ways to gamble, as we can regularly observe, based on the often erratic movements in single stock prices. Pisa Score in 2015: Vietnam - The Outlier The results show that countries with a higher GDP per capita seem to have a relatively higher score in the Programme for International Student Assessment, a so-called PISA score, even though correlation does not imply causation. The GDP per capita only reflects the potential of the country to divert financial resources towards education, and not how much is actually allocated to education. Vietnam is an outlier with the 18th highest score out of the 72 countries, and a relatively low GDP per capita of only around USD 2,200. This compares very favorably to other ASEAN countries, for example Thailand or Indonesia. Vietnam has a much higher score than many of its regional neighbors, and even some of the wealthy European countries such as the UK, Luxembourg, and France. The reason for Vietnam’s high score is probably due to sizeable government and private investments in education and the strong discipline of students and the uniformity of classroom professionalism which can be found across the whole country. Students in Vietnam are often full of energy and very dynamic, eager to learn as much as possible. Knowledge in their eyes is the only way out to achieve a better living standard, given that Vietnam still can be considered as a relatively poor country. This is of course a powerful driver for a country which is among the fastest growing economies in the world. Vietnam small & mid-caps The investment strategy of AFC Vietnam Fund is to focus on undervalued companies, including many small and medium cap stocks, which offer superior valuations relative to other shares within the same sector, for example stronger balance sheets, lower P/E ratios (usually around or below 10), discount to book value or stronger earnings growth. We are not only investing in those stocks because of low valuations but also because they often have hidden assets, such as properties. As we mentioned in the December interim report, we visited many of our holdings. These meetings confirmed our view that many of these companies, especially in the small cap field, have hidden values which are often much higher than their market capitalization. Despite being profitable and having strong balance sheets, they are frequently trading at only half their publicized book value. Some of the properties they own are often valued next to zero in the balance sheet while their estimated market value actually represents multiple times of their total market cap. We are confident that we will continue to find such deeply undervalued companies, which will eventually reflect in the fund performance and hence benefit our investors. Vietnam’s economy expands at 6.2% in 2016 Vietnam's economy grew 6.2% in 2016 according to the General Statistics Office. Although less than the government’s target of 6.7% and the 2015 growth rate of 6.68%, but still higher than the four years’ prior (2011: +5.89%, 2012: +5.03%, 2013: +5.42%, 2014: +5.98%). Vietnam economy was bottoming out in 2012 The government managed to keep inflation below 5% in 2016. According to the General Statistics Office, 2016 inflation was 4.74% YoY with healthcare and education increasing most, 55.7% YoY and 10.8% YoY, respectively. Domestic consumption: Retail sales of goods and services reached USD 150.6 billion, up 10.2% YoY vs 9.8% recorded in 2015. Industrial production: The index of industrial production increased 7.5% YoY vs an increase of 9.8% last year. The manufacturing and processing sector accelerated at a faster rate of 11.2% YoY, while the mining sector declined 5.9% YoY, subtracting 1.3 percentage points from overall growth. Trade: total export revenue for the year increased 8.6% YoY to USD 175.9 billion while import revenue grew at a lower rate of 4.6% YoY to USD 173.3 billion, leading to a trade surplus of USD 2.6 billion. Foreign investment: disbursed FDI hit a record high and rose 9.0% YoY to USD 15.8 billion, while registered and additional FDI slowed 8.1% to USD 21.0 billion. Nevertheless, Investment Law 2014 has encouraged foreign investors to pour USD 3.42 billion via capital contributions and share purchases last year. Thus, foreign investment has totalled USD 24.4 billion. Foreign reserves hit the record high of USD 41 billion by the end of 2016. This was mainly due to the increasing disbursed FDI, remittances, trade surplus and capital inflow.

Other developments - Vietnam market cap increased strongly Despite the mute performance of the overall stock market, 2016 was quite a special year for Vietnam. A lot of state owned companies were listed on the market which helped to increase the market cap substantially. At the beginning of 2016, the total market cap of Vietnam was about USD 58.9 billion (HCMC, Hanoi and UPCoM). This number surged to USD 74.4 billion by the end of 2016, growing at 26.3%. Some of these large listings were for example Sabeco (USD 5.6 billion), Habeco (USD 1.3 billion), Vietnam Aviation Corporation (USD 4.7 billion) and Quang Ngai Sugar (USD 0.8 billion). This trend is expected to continue and other companies with more than USD 1 billion market cap will be listed soon, such as Vietnam Airlines, Vietjet Air and Dung Quat oil refinery. At the end of December, the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (2.9%) – a manufacturer of electrical and telecom equipment, Bao Viet Securities JSC (2.0%) – a securities brokerage company, Agriculture Bank Insurance JSC (1.9%) - an insurance company, Pharmedic Pharmaceutical Medical JSC (1.9%) – a pharmaceutical company, and Vietnam Sun Corp JSC (1.6%) – a travel services company. The portfolio was invested in 84 names and held 2.3% in cash. The sectors with the largest allocation of assets were consumer goods (35.0%) and industrials (26.0%). The fund’s estimated weighted average trailing P/E ratio was 9.44x, the estimated weighted average P/B ratio was 1.57x and the estimated portfolio dividend yield was 6.39%. For more information about Asia Frontier Capital’s Vietnam Fund please click the following links: I hope you have enjoyed reading this newsletter despite the absence of the travel report this time due to the length of this newsletter. We will have another travel report (Myanmar) in our next issue again. If you would like any further information, please get in touch with me or my colleagues. |

||||||||||||||||||||||||||||||||

|

With kind regards, Thomas Hugger |

|||||||||||||||||||||||||||||||||

|

Asia Frontier Capital Limited |

|||||||||||||||||||||||||||||||||

Disclaimer:This Newsletter is not intended as an offer or solicitation with respect to the purchase or sale of any security. No such offer or solicitation will be made prior to the delivery of the Offering Documents. Before making an investment decision, potential investors should review the Offering Documents and inform themselves as to the legal requirements and tax consequences within the countries of their citizenship, residence, domicile and place of business with respect to the acquisition, holding or disposal of shares, and any foreign exchange restrictions that may be relevant thereto. This newsletter is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law and regulation, and is intended solely for the use of the person to whom it is intended. The information and opinions contained in this Newsletter have been compiled from or arrived at in good faith from sources deemed reliable. Opinions expressed are current as of the date appearing in this Newsletter only. Neither Asia Frontier Capital Ltd (AFCL), nor any of its subsidiaries or affiliates will make any representation or warranty to the accuracy or completeness of the information contained herein. Certain information contained herein constitutes “forward-looking statements”, which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of Funds managed by AFCL or its subsidiaries and affiliates may differ materially from those reflected or contemplated in such forward-looking statements. Past performance is not necessarily indicative of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the funds in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. AFC Asia Frontier Fund is registered for sale to qualified /professional investors in Japan, Singapore, Switzerland, the United Kingdom and the United States. AFC Iraq Fund in Singapore, Switzerland, the United Kingdom and the United States. AFC Vietnam Fund in Japan, Singapore, Switzerland and the United Kingdom. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||||||||||

(

(