Asia Frontier Capital (AFC) - August 2016 Newsletter |

|||||||||||||||

In this IssueAFC Asia AFC Iraq AFC Vietnam Fund

|

"Successful Investing takes time, discipline and patience.

AFC Funds Performance Summary

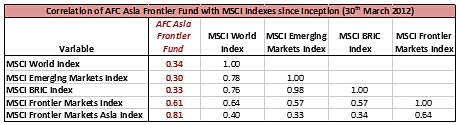

The AFC Asia Frontier Fund has recorded its 6th month of positive performance in a row and is now up +11.6% so far this year in USD terms while the MSCI World Index is up just +3.4%. The AFC Vietnam Fund gained +0.1% in August, its 7th consecutive positive month and is now up +18.4% YTD, outperforming its benchmark, the Ho Chi Minh City Index in USD terms, which is up by +17.5%. On a medium term basis, our funds’ performance is significantly better than that of the relevant indices. In numbers, this outperformance represents +7.7% p.a. for the AFC Asia Frontier Fund and +13.7% p.a. for the AFC Vietnam Fund, both since inception and in USD terms. In August 2016 we have again experienced increased investor interest, especially for our AFC Vietnam Fund, resulting in significant new subscriptions, bringing the AFC Vietnam Fund’s AUM to USD 29.5 million. Asia Frontier Capital’s AUM now stands at USD 46.7 million. Sophisticated investors have long invested internationally, but emerging markets have only been added to high net worth and family office portfolios in the last 25 years or so. Since then, the major emerging markets have become a well-established portion of many international investment portfolios. The markets that these portfolios have exposure to includes countries like China, India, Malaysia, South Korea, and Thailand. These countries have progressed through similar stages of development as frontier markets are experiencing right now. Growth in these countries has been strong and valuations have gone up, benefitting shareholders that own well-constructed portfolios of stocks which has resulted in superior risk adjusted returns. A number of countries in the AFC universe are now in a similar cycle. They are the frontier countries of today and could become the emerging tigers of tomorrow. These frontier markets have enjoyed a low level of interest from the investment community up to now (foreigners own only about 1% of the total stock market capitalization in Bangladesh), but after a prolonged time of GDP growth, expansion of the financial system, and stabilization of the political landscape, such markets graduate and become true emerging markets. This would make these markets instantly attractive and accessible to a broader range of investors, which typically results in a re-rating of these stock markets. For example, Pakistan was chosen to be included in the MSCI Emerging Markets Index in this past June. This upgrade of a frontier market to an emerging market is on the one hand a catalyst for growth for the companies in such countries and on the other hand a driver for a general re-rating of the entire stock market. It can give a significant performance boost to an investment portfolio consisting of quality stocks from such a market. This is a possibility for most of the markets we currently invest in, and we are looking forward to a possible elevation of the Vietnamese market in the next couple of years. Graduation to emerging market status won’t happen overnight, but in the long term, fundamentally good companies in these countries will benefit most. Few international investors – primarily family offices – are currently invested in frontier markets. However, more and more international investors are becoming aware of this relatively new asset class and are starting to consider investing in frontier markets in order to generate superior returns combined with manageable risk and as a result, we have noticed an increasing number of inquiries and allocations from family offices into our funds. To appreciate the size of the opportunities available, let’s consider the relative magnitude of the markets that we invest in. We have seen that the universe of current emerging markets has increased its market share from just 1% of the global market capitalization some 30 years ago to around 10% currently. We believe that a similar development will take place in the markets that currently are in the frontier space. Family offices consider diversification when making investment decisions, and investing in a basket of different frontier markets is true diversification. Frontier markets are less correlated with developed markets compared to the correlation between emerging markets and developed markets. Additionally, the correlation within developed markets is only becoming higher as a result of increasing globalization and new information technology (high speed internet).

Furthermore, correlation between individual frontier markets is very low (and in some cases even negative) as they all have their own set of opportunities and challenges. For example, a low oil price is negative for Iraq, while it is beneficial for Bangladesh as it imports all its oil, and therefore a low oil price will benefit companies in the form of lower costs and benefit consumers in the form of higher disposable income. Appropriate diversification across a range of frontier markets enables the construction of a portfolio with low volatility and healthy performance. The AFC Asia Frontier Fund, which has a correlation of only 0.34 with the MSCI World Index since inception, is a case in point, and it also has a very good performance of +10.5% p.a. with an annualised volatility of just 9.5% since inception. Another consideration sophisticated investors should make is that investing in frontier countries has long term viability. Just look at the development and growth of the middle class in frontier and emerging countries. Looking at the graphic below, we can understand the long term expectations for the quantity of middle class citizens in the world. Notable here is that most of these new middle class citizens are being ‘made’ in Asia: It is expected that the number of middle class citizens would grow by 1.2 billion until 2020 or by 2.7 billion by 2030 which is an increase of 6 times from just 525 million in 2009. This is one of the reasons we focus our attention on investing in Asian frontier markets for the medium and long term, as the opportunities right now are in Asia, and will be for a long time to come.

Second AFC Vietnam Investor TourJust in case you missed this in previous newsletters, AFC will hold its second investor tour to Vietnam from 26th March - 2nd April 2017, which will provide valuable insights about investing in frontier markets and in Vietnam in particular while enjoying interesting sights and relaxation during some extra time before and after the main programme of the tour. The tour will take us to several business centres and a few tourist spots. In Hanoi we will stay at the Sofitel and we will have several factory visits in and around Hanoi on the 27th and 28th of March 2017 and also go to see the Hanoi Stock Exchange. In Ho Chi Minh City we will have a number of presentations by industry experts, and visit several other companies from various industries from 29th to 31st of March 2017. There is also time for recreation and the 26th of March as well as the 1st and 2nd of April are set aside for tourist activities as well as for a few more optional site visits. If you are interested in learning more about this tour, please send an email to Thomas Hugger, email: Our contributing editor John Enos just returned from his journey to several Central Asian frontier countries (where we don’t invest currently): Kazakhstan, Kyrgyzstan, Uzbekistan, and Turkmenistan. We close this month’s newsletter with the second of a three-part series of articles in which he recounts his interesting experiences during this exciting trip. AFC in the Press

Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact Peter de Vries at

AFC Asia Frontier Fund - Manager Comment August 2016

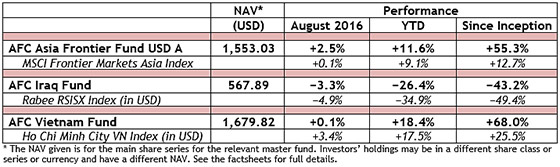

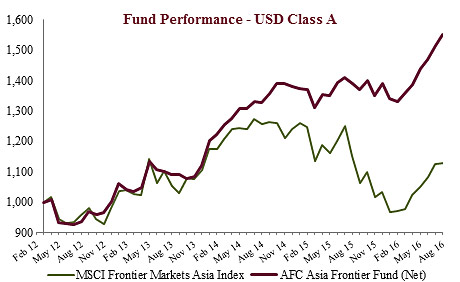

AFC Asia Frontier Fund (AAFF) USD A-shares gained +2.5% in August 2016, bringing the year to date performance to +11.6%. The fund outperformed the MSCI Frontier Markets Asia Index (+0.1%), the MSCI Frontier Markets Index (-1.3%) and the MSCI World Index (-0.1%). The USD A shares achieved an NAV of USD 1,553.03 which is a new all-time high (the previous high was in July 2016 with USD 1,514.42). The performance of the AFC Asia Frontier Fund A-shares since inception on 31st March 2012 now stands at +55.3% versus the MSCI Frontier Markets Asia Index which is up +12.7% and the MSCI Frontier Markets Index (+0.4%) during the same time period. The fund’s annualized performance since inception is +10.5%, which represents an annualized outperformance over the MSCI Frontier Markets Asia Index of 7.7% p.a. Positive performance for the fund continued during the month and the fund outperformed its benchmark due to positive moves in the fund’s largest holding, a Bangladeshi pharmaceutical company, and a +67% move in one of the fund’s larger Pakistani holdings, a beverage company. As pointed out in previous newsletters, it is the non-benchmark names which have led to out-performance since inception and this was the case during this month as well. The fund exited one of its largest Vietnamese holdings, a pipe company which supplies its products to residential as well as to commercial infrastructure projects. This position has been one of the fund’s top performers over the past two years and we had bought it initially due to the cyclical recovery in the real estate market as well as due to greater infrastructure spending. The company has a leading market position in Southern Vietnam and has the largest distribution network with a sound management team. Besides benefitting from a pick-up in real estate and infrastructure spending, the company received tailwinds to its margins from lower input prices, i.e. resin. We exited this position due to the entrance of a new competitor who has an existing distribution network for its existing product line and it also has the capability to increase its production. This was evident in the most recent quarter which saw price cuts even though demand remained strong. With product prices expected to stay at the current level and input prices not providing the benefit (due to higher oil prices) which they did in the past year, earnings growth may not see the same momentum which was seen in the past twelve months. The fund has consequently invested in a real estate developer which focuses on mid-range housing projects primarily in Ho Chi Minh City and an infrastructure player which manages toll roads in Northern Vietnam and is also developing its own real estate projects in Hanoi. Both companies trade at a discount to most other real estate/infrastructure companies in Vietnam and they both have upcoming projects which will help their earnings to grow over the next few years. Further, the fund has also increased its position in a cement company which has a strong presence in Southern and Central Vietnam and is expected to benefit from continued infrastructure spending. Though the fund outperformed its benchmark, Mongolia had a tough month and saw its currency depreciate by 6.8%. On 11th August, the Finance Minister disclosed that the country’s fiscal deficit was higher than previously anticipated. This was followed swiftly by credit downgrades on 19th August by S&P from B to B- and on 26th August by Moody’s from B2 to B3. Further exacerbating the currency’s rapid decline, in a bid to win votes during June elections the outgoing Democratic Party (DP) promised to re-purchase previously distributed shares of the SOE (State Owned Enterprise), Tavan Tolgoi, which is Mongolia’s largest coal producer. The DP also agreed to repurchase Russia’s 49% stake of the SOE, Erdenet Copper for USD 390 million. Both of these dealings put significant strain on Mongolia’s finances. This culminated in the newly elected Mongolian People’s Party (MPP) providing shock therapy to the economy on 18th August through an increase in the Central Bank policy rate of 450bps to 15% and deep salary cuts for civil servants, including a 30% cut in the Prime Minister’s salary. With early signs of a possible bailout from the IMF, the MPP has set expectations low and can now position to outperform by working through its financial challenges while simultaneously continuing to liberalize the economy to attract foreign investment. The best performing indexes in the AAFF universe in August were Vietnam (VN-Index) (+3.4%), Sri Lanka (+2.1%), and Pakistan (+0.7%). The poorest performing markets were Laos (-7.6%) and Mongolia (-6.3%). The top-performing portfolio stocks were a Pakistani beverage company (+67.4%), followed by a Mongolian junior oil exploration company (+67.1%), a Mongolian leather producer (+30.9%), and a Mongolian retail store (+30.4%). In August we added to existing positions in Laos, Mongolia, Pakistan, and Vietnam and we reduced our existing holding in a Sri Lankan and a Pakistani company. We newly added a holding company which invests in Myanmar, a Vietnamese property developer, and a Vietnamese infrastructure/real estate company. As of 31st August 2016, the portfolio was invested in 95 companies, 1 fund and held 8.3% in cash. The two biggest stock positions were a pharmaceutical company in Bangladesh (7.1%) and a Pakistani pharmaceutical company (5.5%). The countries with the largest asset allocation include Vietnam (29.4%), Pakistan (25.4%) and Bangladesh (15.5%). The sectors with the largest allocation of assets are consumer goods (36.7%) and healthcare (19.5%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 19.22x, the estimated weighted average P/B ratio was 1.37x and the estimated portfolio dividend yield was 2.56%. For more information about Asia Frontier Capital’s Asia Frontier Fund please click the following links: AFC Iraq Fund Manager Comment August 2016

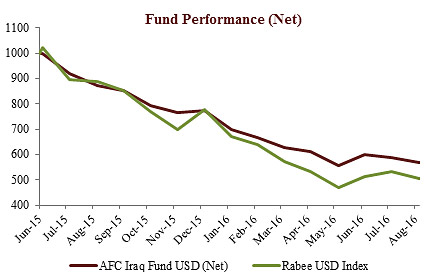

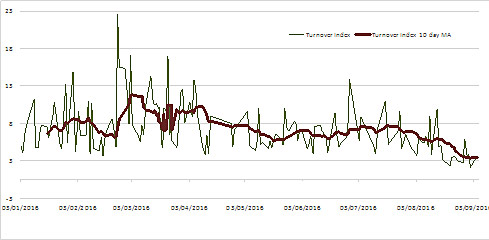

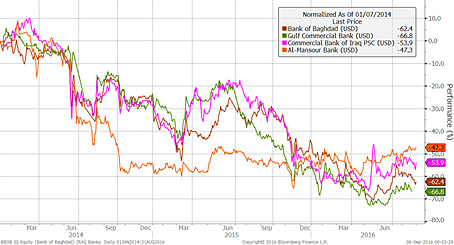

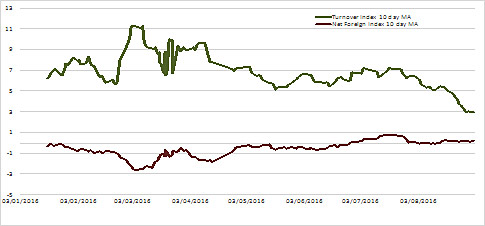

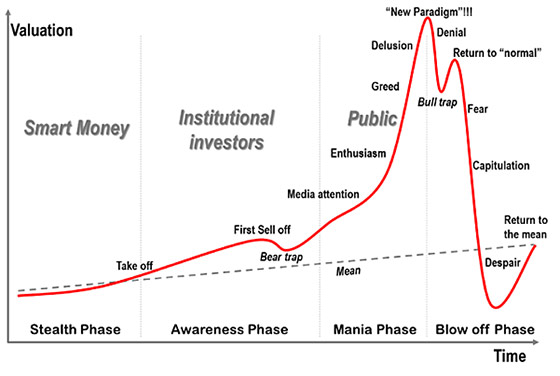

AFC Iraq Fund Class D shares returned -3.3% in August 2016 with an NAV of USD 567.89, an outperformance of +1.6% vs. the Rabee RSISX USD Index (RSISUSD) which returned -4.9% in USD terms. The fund has outperformed the RSISUSD by +8.5% year to date and +6.2% since inception. Coverage of Iraq from the doom & gloom that dominated over the last couple of years has started to shift to one of opportunity and potential. Business publications such as The Wall Street Journal in mid-August reported on the return of foreign companies & capital to Iraq just as the end of the conflict is becoming increasingly likely. While not new news as such, their significance is in moving from specialist coverage into the business media and will likely be a theme that will be featured by more mainstream publications much as it was during the investment boom in 2010-2013. If these developments are borne out fully, they would represent a sea change from 2015 & so far in 2016 as highlighted in last month’s newsletter. Parallel to this shift is a similar change of the conflict’s coverage by mainstream media from focusing on ISIS’s invincibility that characterized prior coverage into focusing on its internal disintegration and eventual military defeat. The continued combination of both shifts will serve to change Iraq’s overstated risk perception and understated opportunity into a more balanced perception. That this thinking is entering mainstream can be seen from S&P’s decision on 27th August in affirming Iraq’s credit rating with stable outlook believing that its financial and military challenges will be contained. The liberation of Mosul is progressing ahead of schedule with the continued encirclement of the city by the Iraqi army & Kurdish Peshmerga forces backed by the international coalition. However, political squabbling in Iraq resulted in parliament’s impeachment of the defence minister which could negatively affect this battle. This is mitigated by reports that interim Chief of Army Staff is acting in the capacity as an interim Defence Minister until a new minister is appointed providing continuity. Another mitigating factor is that the fight is coordinated by Iraq’s international sponsors and therefore should continue as planned. Market turnover shrunk over the month to almost half of the year’s average as can be seen from the turnover chart below (excluding actions by strategic holders whether foreign or local) Turnover on the Iraq Stock Exchange (ISX) A number of factors contributed to the lower turnover: holiday season, trading suspensions as part of the AGM season or due to delays in publishing annual reports which this year have taken longer than usual for companies to release and for auditors & regulators to sanction. Finally, and most importantly, the trading suspension since mid-June of the market’s bell weather, Baghdad Soft Drinks (IBSD), as the regulator is reviewing its proposed merger with a private company holding PepsiCo’s Aquafina license. In a retail driven market with limited liquidity, any capital tied up while stocks are suspended, esp. IBSD, has a dramatic effect on liquidity and on the performance of the remaining shares. This was the case this month with prices mostly drifting lower. Most trading activity was concentrated in banks with some declining such as Bank of Baghdad (-10.3%), Investment Bank of Iraq (-10.2%), Gulf Commercial Bank (-2.5%) while others were up such as Mansour Bank (+6.7%) and Commercial Bank of Iraq (+2.5%). It is worth noting that these moves seem to be consistent with a bottoming process as the chart below shows. Rebased price performance in USD of selected Iraqi Banks Improvement in foreign inflows continue from last month, with foreigners as marginal net buyers but, as noted last month, it still is more of a function of an absence/exhaustion of selling as opposed to any significant new inflows. As the only, for the time being, source of new liquidity and crucially the institutional nature of ownership vs. speculative retail their effect can be meaningful on overall turnover as the chart below shows (excluding actions by strategic holders whether foreign or local) Turnover on the Iraq Stock Exchange (ISX) vs net Foreign trading With Iraq’s improving financial position, local liquidity will improve but with a time lag and so the opportunity for long-term investors continues to be to acquire assets and build positions during this time. It can be argued that the market is in the Stealth Phase of the “four phases of a Bubble” as identified by Dr. Jean-Paul Rodrigue at Hofstra University, New York (first discussed here by the AFC Vietnam Fund a couple of months ago) whose work is often referenced in discussing market cycles.

Investors in the Stealth phase are characterized as “Those who understand the new fundamentals realize an emerging opportunity for substantial future appreciation, but at a risk since their assumptions are so far unproven”. The next stages are: Awareness in which “Many investors start to notice the momentum, bringing additional money in and pushing prices higher”; Mania as “Everyone is noticing that prices are going up and the public jumps in for this investment opportunity of a lifetime”, Blow-off when “A moment of epiphany (a trigger) arrives and everyone roughly at the same time realize that the situation has changed”. The blow-off phase ends with the despair part when investors think of the market as "the worst possible investment one can make" and Dr. Rodrigue argues “There is even the possibility that the valuation undershoots the long term mean, implying a significant buying opportunity”. Quotes in Italic are from Dr. Rodrigue’s work. That the country, post conflict, represented a significant opportunity was the thesis behind the launching of the AFC Iraq Fund a year after the ISIS invasion of Mosul and the market’s bust and since the mainstream avoided it. Iraq’s market has not witnessed a Bubble in full bloom like other Bubbles as it was deflated by the ISIS invasion and then squashed by falling oil prices as the world obsessed over the slow-down of China and other emerging markets. Its Mini-Bubble went as follows: There was a great deal of excitement about Iraq’s rapidly gowning oil production and the massive reserves it had in 2010-2013, which saw the publication of the International Energy Agency’s (IEA) main work on Iraq in 2012 attract huge interest by oil companies and the investment world. At the time almost every investment bank published a major piece on Iraqi oil and the massive reconstruction cycle to rebuild the country after over 30 years of conflict. This was followed by fund flows into Iraq, and from the lows of mid-2012 to the peak in early 2014 many stocks saw significant gains with Baghdad Soft Drinks (+270%), Mamoura Real Estate & Gulf Commercial Bank (+140%), Kurdistan Bank & Credit Bank of Iraq (+100%), and Bank of Baghdad (+75%) (figures rounded). After a terrible 2½ years of declines in which the market was down about 65% (see banking chart above for specifics) the current phase feels very much like a stealth phase. Although the country might have tip toed into the awareness phase with the changing media coverage, low local and absent foreign liquidity places the market in the stealth phase. While oil prices will not revisit $100 any time soon, the theme for Iraq is the massive reconstruction cycle following the ISIS conflict powered by rising oil production and global investment in infrastructure to create and foster prosperity to defeat extremism and cement the end of conflict as discussed in prior newsletters. As of 31st August 2016, the AFC Iraq Fund was invested in 14 names and held 2.0% in cash. As the fund invests in both local and foreign listed companies that have the majority of their business activities in Iraq, the countries with the largest asset allocation were Iraq (94.1%), Norway (3.9%), and the UK (2.0%). The sectors with the largest allocation of assets were financials (61.9%) and consumer staples (18.8%). The estimated trailing median portfolio P/E ratio was 11.2x, the estimated trailing weighted average P/B ratio was 0.98x, and the estimated portfolio dividend yield was 2.62%. It would be appropriate to end this section by quoting Sir John Templeton “Bull markets are born in despair, grow amid scepticism, mature in optimism, and die amid euphoria”. For more information about Asia Frontier Capital’s Iraq Fund, please click the following links: AFC Vietnam Fund - Manager Comment August 2016

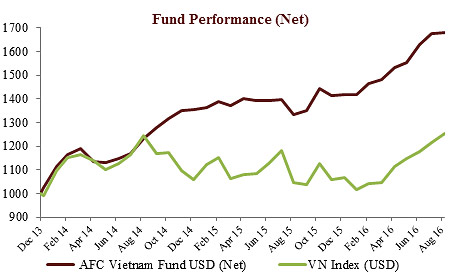

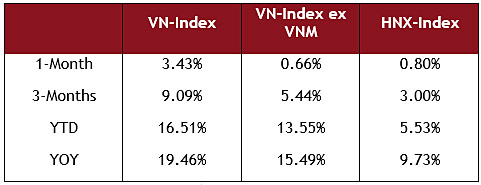

To read this month’s fund update in German please click here. The AFC Vietnam Fund gained +0.1% in August to a reach new high NAV of USD 1,679.82, bringing the year to date net return to +18.4% and the net return since inception to +68.0%, or +20.8% annualized. By comparison, the August performance of the Ho Chi Minh City VN Index was up +3.2% while the Hanoi VH Index decreased by -1.2% (in USD terms). Since inception, the AFC Vietnam Fund has outperformed the VN and VH Indices by +46.4% and +51.7% respectively (in USD terms). In the final weeks of August, we saw low volatility and minor index changes. Investors are still waiting for the ETF rebalancing which will take place on 16th September 2016. Like in July, the market was supported strongly by share price advances in Vinamilk and Vietcombank, which were equivalent to an index gain of 2.8%. With other stocks still in consolidation mood, the indices in Ho Chi Minh City and Hanoi were up +3.2% and down -1.2% respectively for the month of August. Market developments The Index hit a 5 year high on 14th July at 681.75 before starting to correct in the first week of August to a short term bottom of 622.14. Since then we saw a recovery of the market which was influenced heavily by the gains of Vinamilk (VNM). After the announcement to abolish the foreign ownership limit of VNM about three months ago, the stock increased sharply. Together with the second heavyweight Vietcombank, the current weighting is approaching 30% and therefore had a disproportional effect on the performance of the Ho Chi Minh City index (VN-Index) and as a result it did not represent the performance of the broader market and without those two stocks the valuation of the VN Index would have been more than 20% lower. Impact of VNM on VN Index This explains why the 1-month and the 3-month performance of the VN-Index is significantly different than the VN-index ex VNM. However, in our point of view, VNM is now trading on par with other companies worldwide in this sector and much less attractive after jumping +14.5% in July and +21.3% in August in anticipation of heavy buying by ETFs on their upcoming September rebalancing. It is now trading at 25.6x trailing earnings and pushing up the average P/E on the VN-Index to 16x as compared to only 10.7x on the Hanoi index (HNX-Index). Meanwhile the average P/E of our fund portfolio is still only around 9x. Of course we stick to our long-term investment philosophy to invest in a broadly diversified portfolio of undervalued stocks, rather than overweight a single heavyweight index stock although we do still hold a smaller position in VNM for quite some time.

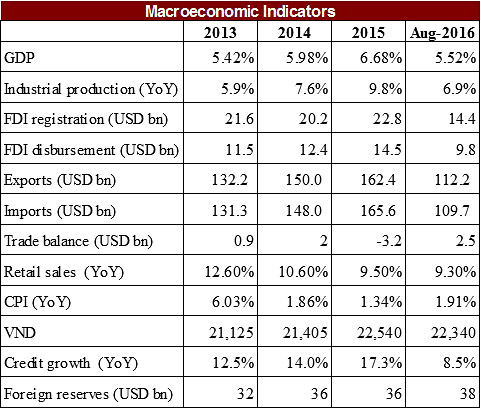

Economy Regarding the macroeconomic story in Vietnam, the country continues to attract strong FDI inflows and shows an improvement in the trade balance. In August, FDI, new and additional registrations, hit USD 14.4 billion, an increase of 7.8% compared to the same period last year. FDI disbursement reached USD 9.8 billion which also helps to improve the country’s foreign reserves. According to a recent article by the Financial Times, Vietnam ranks 1st in Asia in terms of FDI quality. New and additional FDI registrations continue to focus on industrial production with more than 70% of total capital, which is expected to boost industrial production in the coming years. The country's trade balance has improved a lot in the first 8 months, hitting a surplus of USD 2.5 billion compared to a deficit of USD 3.6 billion last year. The better trade balance and strong FDI inflows also result in a very stable Vietnamese Dong. Vietnam is currently one of the very few countries with increasing exports in Asia. In total, the export hit USD 112.2 billion in the first 8 months, growing by 5.5% compared to the same period last year. In August, CPI increased slightly to 1.91% compared to 1.82% in July. In the CPI basket, educational prices increased most by +0.47% against July because of the start of the new school year in August.

Other developments While the world is – like every single month of the past two years – still waiting for any hint of a possible interest rate hike in the US from close to zero, we see a further stabilization in emerging market economies. It seems to be already a long time back that investors and analysts were fearing a total collapse of the economies at former investor darlings like Brazil, China or Russia. With better than feared growth numbers in Brazil or Russia and relatively strong growth in countries like Thailand, Indonesia or Philippines, the pace in the economic upwards cycle in South East Asia could also accelerate. On a long term basis one has to remind themselves anyway, where the future growth and investment story is to be found. At the end of August, the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (2.5%) – a manufacturer of electrical and telecom equipment, Bao Viet Securities JSC (2.4%) – a securities brokerage company, Global Electrical Technology JSC (2.1%) – an electrical equipment manufacturer, PetroVietnam Fertilizer and Chemical JSC (1.7%) – a fertilizer manufacturer, and Vietnam Livestock Corporation JSC (1.6%) – a company involved in financial investment, technology transfer of livestock and poultry husbandry and animal feed production. The portfolio was invested in 88 names and held 5.7% in cash. The sectors with the largest allocation of assets were consumer goods (35.2%) and industrials (22.8%). The fund’s estimated weighted average trailing P/E ratio was 8.84x, the estimated weighted average P/B ratio was 1.18x and the estimated portfolio dividend yield was 5.04%. For more information about Asia Frontier Capital’s Vietnam Fund please click the following links: AFC Travel Report – UzbekistanThis is the second of a series of three reports by AFC contributing writer John Enos, who recently spent two months traveling by bicycle, train, and bus across Central Asia from Almaty to Ashgabat. To read the first part, click here. Feel free to reach out to him at My two friends and I arrived in Bishkek on our bicycles exhausted, unshaven, and quite tired of the mutton-and-vodka-heavy, vegetable-scarce cuisine we had been eating every day in rural Kyrgyzstan. Two weeks prior, we had arrived in Kazakhstan with an overly ambitious plan of bicycling to Turkmenistan. One bicycle was delayed a week, however, and we soon realized that we would have to take a flight and some trains and buses in order to complete the trip on time. Our Uzbekistan and Turkmenistan visas had fixed dates of entry and departure, and we were too far away to cycle there in time. Finding information on domestic and regional flights in Central Asia is difficult to do from afar, and although we hadn’t found any reliable sources online confirming that there were flights from Bishkek to Tashkent, we stumbled upon the ticketing kiosk for Air Kyrgyzstan. Although banned in the European Union, they had flights bound for Uzbekistan, and after some haggling and confusion over the price of shipping a bicycle, we departed for Tashkent, the capital of Uzbekistan. The arrival and immigration procedure at the airport in Tashkent was awful, and one of the most inefficient and bureaucratic arrival procedures I’ve encountered in my travels. The line to clear the security screenings stretched hundreds of people, almost entirely Uzbeks coming from Dubai lugging all sorts of TVs and electronics and yelling to each other about how to avoid paying customs tariffs (just a wild guess!) There were a few tired looking Korean expatriates with golf bags, a couple of old European tour groups, and us Americans pushing our bike boxes. Uzbekistan’s countless UNESCO World Heritage Sites and incredible relics from the Silk Road give it by far the greatest tourism potential of any of the ‘Stans, but the visa policy is incredibly complicated, expensive, and deters many people from visiting. A British friend living in Kenya told me he had planned a trip to Uzbekistan but eventually gave up when he realized how difficult it would be to get it all sorted from Africa. Luckily, I had been able to get my visa at the Uzbekistan embassy in Bangkok, albeit with a few days of delays. It was clear once we cleared customs and found a taxi driver how very different Uzbekistan was from Kyrgyzstan. While we had primarily been in high elevation on the vast, green steppe in Kazakhstan and Kyrgyzstan, Uzbekistan felt more like what I imagined the Silk Road would be – hotter, drier, and much more influenced by Islam. We spent a few days in Tashkent getting our bearings and wandering the city, which we very much enjoyed. Until Almaty launched its metro in 2011, Tashkent was the only city in Central Asia to have a metro. Opened in 1977, it was the 7th metro built in the former USSR, and each metro station had marvelous architecture, ornate tilework, and unique art centering on a different theme for each station, from cosmonauts to apricots to cotton. It was really spectacular to wander the metro stations and absorb the intricate level of detail of each station, and was also a welcome reprieve from the scorching Uzbek heat. Sadly, photography is strictly forbidden on the metro, as it is deemed a “military installation” and perhaps as a heightened security response to a 1999 terrorist car bomb attack in Tashkent. Entering each station almost felt like going through airport security, with the station police vigilantly opening all bags and not smiling. Someone braver than I managed to take some photos of the stations however.

We soon learned in Uzbekistan that getting money was not straightforward, and equal parts frustrating and exciting. The frustrating part was that ATMs were nearly impossible to find throughout the country, and most rejected Western cards or gave you Uzbek Som at the official government exchange rate. The exciting part was that this meant we got to change money on the black market which, while technically illegal, was something all Uzbeks and travelers seemed to do and our hotel offered to do for us in Tashkent. The official exchange rate when we were there was roughly 3,000 Soms = 1 USD, but on the black market, we could get 6,500 Soms. Such a huge spread, in fact, that a February article from Bloomberg called out the Uzbek Som for having the second highest premium between the black market and the official rate after the Angolan Kwanza, highlighting the difficulty of currency pegs for emerging market currencies. In practical terms, this meant that we had to carry pristine US dollar bills with us for our entire duration in Uzbekistan, and the moneychangers at Uzbek bazaars would spot us from a mile away as a few Westerners who likely were carrying a foreign currency they wanted. The funniest thing about changing cash on the black market is that you needed to bring shopping bags and rubberbands. The largest denomination of note is 5,000 Uzbek Som, worth USD 0.77 when we were there! It should also be noted that 5,000 Som notes were pretty rare, and in reality we almost always received shopping bag bundles of 1,000 Som notes (worth 15 cents each). Now you can imagine me changing USD 200 on my first day in Tashkent and being amazed when the moneychanger returned with 1,333 bank notes for me…1.3 million Som in 1,000 Som notes! Needless to say, I stopped using a wallet in Uzbekistan and instead walked around with rubberbanded stacks of bills and bulging pockets, feeling like a street level drug dealer from The Wire.

After a few days in Tashkent, we headed by train to Samarkand, the famed Silk Road site bursting with dazzling Islamic architecture and a vital stop on the Silk Road. We chose to travel there by train, and were all impressed by the Afrosiyob, Uzbekistan’s “bullet train” connecting Tashkent and Samarkand which reaches speeds of 250 km/h but was unfortunately sold out on our planned day of departure. Samarkand is one of those places like Zanzibar, Melaka, or Mandalay to which I had wanted to visit for ages due to the name alone. Once one of the greatest cities in Central Asia, many believe the city was founded in the 7th or 8th century BC and was a vital trade point for commerce between China and the Mediterranean on the Silk Road. It was conquered at various times by Alexander the Great, Genghis Khan, and Timur, and ruled by Persian, Turkish, and Mongol peoples, making the city a confluence of different cultures, religions, and people and contributing to the rich history and sights that make it such a stunning place.

Our three days in Samarkand were filled with wandering the dozens of mosques, madrassas, mausoleums, and other Silk Road ruins, the likes of which cannot be described in a few paragraphs. I found the sites at Samarkand as jaw-dropping as Angkor Wat, and completely empty of tourists – the only other people we found were young Uzbek couples flirting under 15th century Islamic architecture and the occasional elderly German or Japanese tour group. I hope some of my pictures help do it justice.

It is hard for me to write about a country without discussing its cuisine, and in Uzbekistan, plov is king. Plov is the Uzbek version of the pilau / pilaf I have had in India and Tanzania, a simple dish of rice, meat, a few vegetables, and a lot of fat. I couldn’t help but laugh at our Lonely Planet guidebook’s entry describing the importance of plov to Uzbeks, both as a staple dish and as an aphrodisiac: “Plov has been elevated to the status of religion in Uzbekistan. Each province has its own style, which locals loudly and proudly proclaim is the best in Uzbekistan - and by default the world. That plov is an aphrodisiac goes without saying. Uzbeks joke that the word for 'foreplay' in Uzbek is 'plov'. Men put the best cuts of meat in the plov on Thursday; not coincidentally, Thursday's when most Uzbek babies are conceived. Drinking the oil at the bottom of the kazan (large plov cauldron) is said to add particular spark to a man's libido.” Unfortunately, we never found the chance to drink the oil at the bottom of the cauldron, though we did savor many a tasty Uzbek plov.

From Samarkand, we continued west by train to Bukhara, another fabled Silk Road trading mecca teeming with impressive mosques and madrassas, and finally to ancient Khiva, before bidding farewell to Uzbekistan.

Uzbekistan was one of the most enchanting countries I’ve ever visited, and despite the difficulties of getting a visa, it was well worth it for the amazing two and a half weeks we spent travelling there.

In next month’s newsletter, I’ll write the last report from this trip detailing my experiences in Turkmenistan, often dubbed the “North Korea of Central Asia”. Stay tuned!

|

||||||||||||||

|

I hope you have enjoyed reading this newsletter. If you would like any further information, please get in touch with me or my colleagues. With kind regards, Thomas Hugger |

|||||||||||||||

|

Asia Frontier Capital Limited |

|||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Iraq Fund, AFC Iraq Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the funds in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. AFC Asia Frontier Fund is registered for sale to qualified/professional investors in Japan, Singapore, Switzerland, the United Kingdom and United States. AFC Iraq Fund in Singapore, Switzerland, the United Kingdom and the United States. AFC Vietnam Fund in Japan, Singapore, Switzerland and the United Kingdom. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||

GO TOP |

|||||||||||||||