Asia Frontier Capital (AFC) - April 2016 Newsletter |

|||||||||||||||||||||||||||||||||||

In this IssueAFC Asia AFC Iraq AFC Vietnam Fund

|

"Most people get interested in stocks when everyone else is.

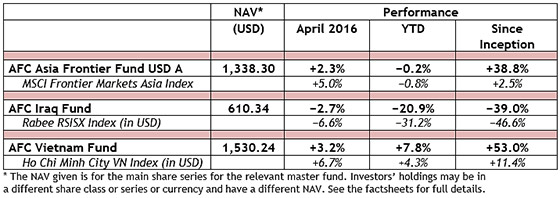

AFC Funds Performance Summary

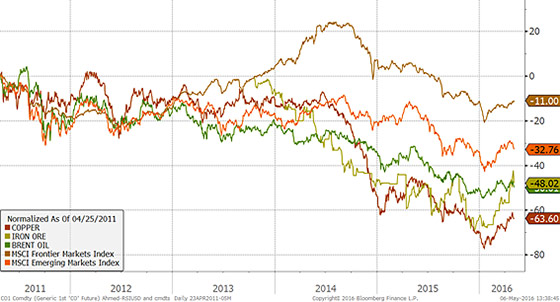

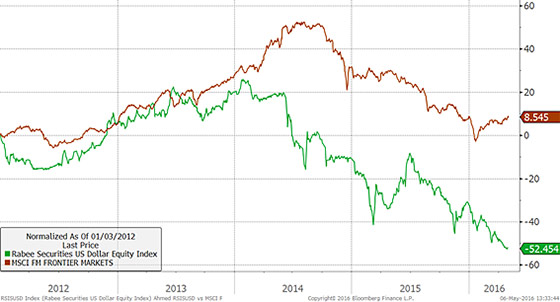

World markets started weak this year with a big drop in January and February 2016, and most of them have not recovered completely as of yet. At the end of April 2016, most major indices were still in negative territory such as Euro Stoxx (-7.3%), Nikkei (-12.4%), CAC40 (-4.5%), DAX (-6.6%), HSI (-3.9%), and MSCI Asia Pacific (-0.6%). Also interest rates have not been attractive for investors and there are even banks that charge for deposits, and the Euro interbank interest rate is at –0.2% while even JP Morgan Chase started to charge a negative interest rate in the form of a 1% “balance sheet utilization fee” on USD deposits. Corporate bonds that pay a reasonable return are perceived as being risky. It is no surprise then that people look for more alternative investments in these times, including real estate, hedge funds, and investments in frontier economies. Even though markets have been volatile over the past year, all of AFC’s funds have outperformed their relevant indices year to date and over the long term and it is not surprising that we have seen a greater number of enquiries regarding our funds, which has led to a large number of new investors into AFC Funds this month. While the performance of the AFC Iraq Fund has been negatively impacted by slumping oil prices and country-specific events, the fund has been able to outperform its benchmark since inception and given the recent stability in oil prices and the push back against ISIS, the current environment offers a good entry level to the fund. Investors who follow Baron Rothschild, who said "Buy when there's blood in the streets, even if the blood is your own", could consider investing in Iraq now as “when the dust settles”, the recovery in the economy and especially the stock market will be swift and strong. With the known problems in Iraq already discounted, the opportunity has only been getting cheaper and more attractive. No one knows exactly when the fortunes will turn around for the Iraqi market but it looks like it could be very close. This month there is a special offer for new investors in our AFC Iraq Fund (see further details below). AFC Iraq Fund celebrates its first birthday with a 3 month fee waiver on new subscriptionsThe AFC Iraq Fund will be one year old on the 26th June 2016 and to celebrate this event, all subscriptions received from today until 26th June 2016 will have management fees and performance fees waived for 3 months. The timing could be attractive considering that the market, as measured by the RSISX index in USD terms, is down over 31% YTD and over 46.6% since the Fund’s inception, which among other things tracked the collapse in oil prices (given their high correlation), but the fund has yet to experience the same recovery that oil prices have seen from January lows. For a figure showing this correlation and further information on the AFC Iraq Fund, please see the AFC Iraq Fund Manager Comment section further down below. AFC in the Press

Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact Peter de Vries at

AFC Asia Frontier Fund - Manager Comment April 2016

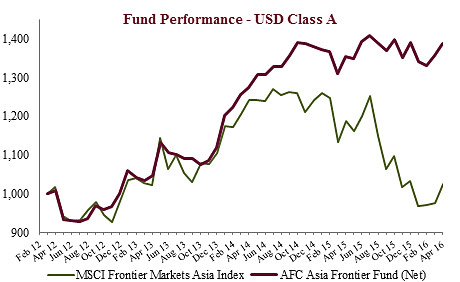

AFC Asia Frontier Fund (AAFF) USD A-shares gained +2.3% in April 2016. This month, the fund underperformed the MSCI Frontier Markets Asia Index (+5.0%), was in line with the MSCI Frontier Markets Index (+2.7%), and outperformed the MSCI World Index (+1.4%). The performance of the AFC Asia Frontier Fund A-shares since inception on 31st March 2012 now stands at +38.8% versus the MSCI Frontier Asia Index which is up just +2.5% and the MSCI Frontier Index (+4.3%) during the same time period. This was the second month in a row of positive performance for the fund and though the fund did underperform the benchmark, this was primarily due to the underweight position that the fund has in banking and oil & gas stocks, which rallied during the month in Pakistan and Vietnam where these sectors have a higher weighting. Performance was driven by Mongolian junior mining stocks, which rallied during the month, while the fund’s largest holding, a Bangladeshi pharmaceutical company, posted excellent profit growth for the last quarter of 2015 which led to a good performance in Bangladesh. Sri Lanka was a positive contributor to performance as the government decided not to impose the previously proposed capital gains tax and this helped improve investor sentiment. Furthermore, the IMF has reached an agreement with the Sri Lankan government to provide USD 1.5 billion in loans to help overcome the balance of payments issues that it is expected to face this year. The government also plans to raise USD 3 billon in sovereign bonds in the near future. Though these are positives, one can expect further fiscal consolidation measures from the government as it will need to bring down its fiscal deficit, and these measures could be in the form of further tax increases. This may not be good for market sentiment. We also believe that consumer spending could begin to be impacted later this year as the rupee depreciation would make imports more costly and a rise in interest rates would dampen consumer spending. The fund’s largest Pakistani holding, a pharmaceutical company, declared good quarterly results while the two cement companies the fund holds also declared strong domestic cement sales growth for the recently ended quarter. The main drivers of performance in Pakistan, however, were an oil & gas company and a media company. In Vietnam, the fund benefited from an automobile battery company which declared a higher dividend payout. So far, a majority of the fund’s top 10 holdings have shown good quarterly results and we are positive on their respective outlooks and valuations. Though the fund did underperform the benchmark during the month, it has been a conscious decision to avoid the banking and oil & gas names within the fund’s key markets and this has led to an outperformance over the index in the past year. The best performing indexes in the AAFF universe in April were Sri Lanka (+7.3%) and Vietnam (VN-Index) (+6.7%). The poorest performing markets were Iraq (-4.9%) and Bangladesh (-3.7%). The top-performing portfolio stocks were an oil exploration company from Mongolia (+223.5%), followed by a Mongolian junior copper mining company (+66.7%), a Mongolian coal mining company (+53.6%), and an Iraqi junior oil producer (+28.6%). In April we added to existing positions in Bangladesh, Mongolia, Pakistan, and Vietnam. We added (for the third time in the history of the fund) a Cambodian entertainment company to the portfolio and we completely exited a Sri Lankan / Maldivian hotel chain. Furthermore, we reduced our holdings in a Sri Lankan motor company, a Vietnamese stationery company, and a Mongolian consumer product company. As of 30th April 2016, the portfolio was invested in 101 companies, 1 fund and held 5.4% in cash. The two biggest stock positions were a pharmaceutical company in Bangladesh (6.5%) and a Pakistani pharmaceutical company (4.8%). The countries with the largest asset allocation include Vietnam (31.4%), Pakistan (20.6%) and Bangladesh (15.7%). The sectors with the largest allocation of assets are consumer goods (37.8%) and healthcare (17.4%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 14.86x, the estimated weighted average P/B ratio was 1.62x and the estimated portfolio dividend yield was 3.07%. For more information about Asia Frontier Capital’s Asia Frontier Fund please click the following links: AFC Iraq Fund Manager Comment April 2016

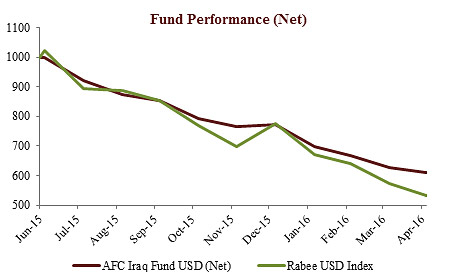

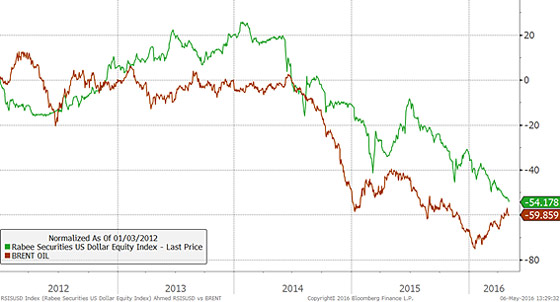

AFC Iraq Fund Class D shares returned -2.7% in April 2016 with an NAV of USD 610.34, an outperformance of +3.9% vs. the Rabee RSISX USD Index (RSISUSD) which returned -6.6% in USD terms. The fund has outperformed the RSISUSD by +10.3% YTD and +7.6% since inception. The massive summer protests, provoked by the failure of past governments to provide essential services, continued in response to unimplemented promised reforms. The reforms were thwarted continuously by vested interests and by the prior administration. Protests took on new life with the active involvement of a prominent cleric, who has pushed for replacing party appointed ministers with technocrats and culminated in demonstrators occupying the parliament building on 30th April. The size, strength, and peaceful nature of the demonstrations and the ability to repeat the process will likely force the formation of a government capable of implementing reforms. The precedent was the pressures of the ISIS occupation in June 2014 that forced the formation of the present compromise government replacing the previous divisive, polarizing one. Then it took the sponsorship of both the US and Iran to usher in a new administration. In a replay, the US reiterated its support for the leadership and the process of reforms through consecutive visits by Secretary of State John Kerry, Defence Secretary Ash Carter, and finally Vice President Joe Biden. Iran, on the other hand, reiterated its support for the integrity of the country and the democratic process during a visit to Tehran by the UN Special Representative for Iraq Jan Kubis. In a further development of the capital investment cycle for post-conflict Iraq, the International Finance Corporation (IFC) announced USD 375 million in financing for an Iraqi power company to expand electricity generation in Baghdad and Kurdistan. Financing was a combination of debt and equity with USD 250 million from IFC and USD 125 million from Lebanon's Bank Audi. The IFC has been an active investor in Iraq since 2003 to help diversify the economy away from oil, accelerate job creation, and encourage regional investment in the country. The participation of Bank Audi in such a size is a positive development highlighting the disparity between actual risk and perceived risk in Iraq and demonstrates a success for the IFC in encouraging such investments. Interest in emerging markets has resumed after the last traumatic nine months that seems to have marked the bottom for the five-year bear market in emerging markets and industrial commodities including oil. All of which, even after the significant rallies from January's lows, are still at the same multi-year lows of last year, as the chart below demonstrates. Copper, Iron ore, Brent crude, and the MSCI Emerging Markets Index are still between 31-64% below the peak of early 2011. The well-known problems are genuine and real but this was why stocks were declining for all these years while the fears that gripped the markets since August of last year were an irrational reaction to well-known and already discounted negative factors. In hindsight, it could almost be a textbook example of fear gripping markets that accompanies significant bottoms. Copper, Iron Ore, Brent Crude, MSCI EM & FM indices rebased to 2011 If this reading is correct, then the rallies since the January lows could be part of a bottoming process and consequently the MSCI Frontier Markets Index, which peaked in 2014, could likely see a similar bottoming process over the next few months. This analysis extends naturally to Iraq, which started witnessing meaningful foreign fund inflows since 2012 and as such started to correlate more with the MSCI Frontier Markets Index as can be seen from the chart below. MSCI Frontier Markets Index & RSISUSD Index, rebased since early 2012 The close correlation with the MSCI Frontier Markets Index has been lock step in direction and magnitude from 2012 until early 2014, when Iraq’s conflicts accelerated, causing the magnitude of the RSISUSD declines to be far larger. Nevertheless, it followed the MSCI’s Frontier Markets Index which makes sense in that it is affected by the same inflows/outflows influencing frontier markets in general. However, the technical factors cited last month (the liquidations of the sizable Iraq Fund and HSBC’s final stake in an Iraqi bank) drove the uncorrelated price action of the RSISUSD Index year to date. Finally, the recovery in oil prices since January is significant for the market given the economy’s leverage to oil prices and the effect on local liquidity, however, with a time lag as the chart below shows. Brent Crude & RSISUSD Index, rebased since early 2012 The combinations of resumption of interest in frontier markets and further recovery or stabilization of oil prices should lead to a recovery of foreign inflows into the Iraqi equity market. Looking at the portfolio, as of 30th April 2016, the AFC Iraq Fund was invested in 14 companies and held 1.2% in cash. As the fund invests in both local and foreign listed companies that have the majority of their business activities in Iraq, the countries with the largest asset allocation were Iraq (92.4%), Norway (5.9%), and the UK (1.7%). The sectors with the largest allocation of assets were financials (47.4%) and consumer staples (25.8%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 23.53x, the estimated weighted average P/B ratio was 1.14x, and the estimated portfolio dividend yield was 4.35%. For more information about Asia Frontier Capital’s Iraq Fund, please click the following links: AFC Vietnam Fund - Manager Comment April 2016

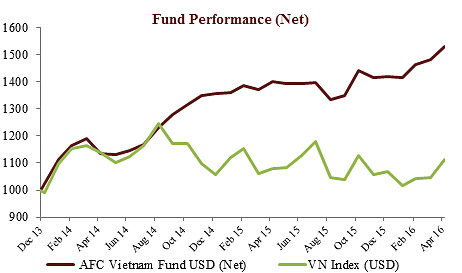

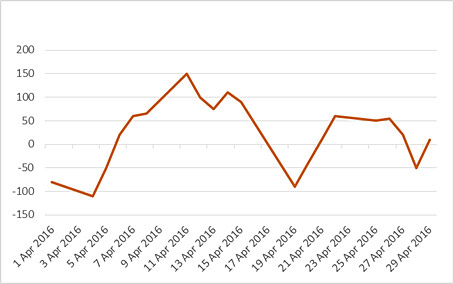

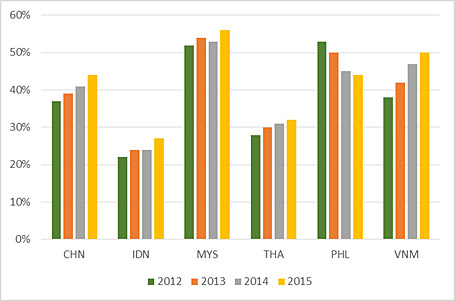

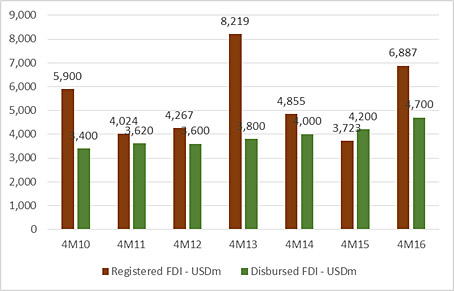

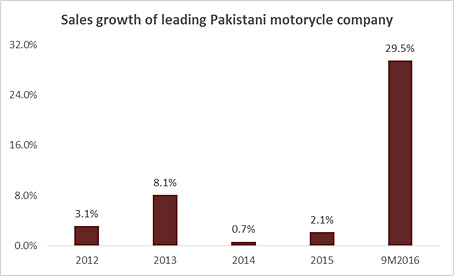

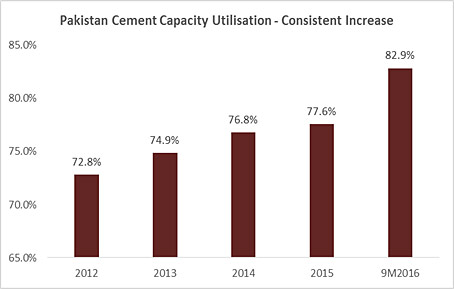

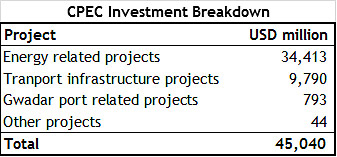

To read this month’s fund update in German please click here. The AFC Vietnam Fund gained +3.2% in April to a NAV of USD 1,530.24, bringing the year to date net return to +7.8% and the net return since inception to +53.0% or +19.2% annualized. By comparison, the April performance of the Ho Chi Minh City VN Index was +6.7% while the Hanoi VH Index increased by +2.1% (in USD terms). Since inception the AFC Vietnam Fund has outperformed the VN and VH Indices by +41.6% and +41.2% respectively (in USD terms). Although the month of April could still not provide absolute certainty about the recently mentioned interesting technical constellation, the last few weeks confirmed the positive developments of the stock market and on the macroeconomic front. In the second half of April, only the exchange of Ho Chi Minh City (HCMC) was able to advance significantly and therefore created a very divergent picture for the entire month. While the index in HCMC increased by a whopping +6.6%, the gains of the Hanoi exchange (+2.1%) and our portfolio (+2.9%) were much more modest. Even the market breadth on the well-performing HCMC stock market was virtually unchanged this month. It is interesting to note that the main reason for it was the short term behaviour of market participants and the working practice of ETF’s in Vietnam. April-Comparison Hanoi (HNX) vs Ho Chi Minh City (VN) Advance/Decline Ratio Ho Chi Minh City The slowly but surely improving sentiment towards emerging markets among international investors created strong inflows which we haven’t seen for a long time. As usual, these inflows mainly targeted the liquid blue chips which still have foreign room left to invest and these stocks therefore increased in a very short period up to 25%. While foreign trading volume is about 10% on average, recent market action brought this ratio to 25%, and in some of these blue chips, foreign participation increased to an impressive 40-70%. These investors didn’t seem to care that some of these stocks, with P/E's of 20-30, are among the most expensive in Vietnam. We have seen this kind of behaviour before, but we do not act on these short term movements as our buying decisions are still strictly based on valuations. One can now only hope that local investors are infected by this positive mood and will trigger a broad market upturn, and that we therefore would finally break out of the 2-year sideways pattern. Also our fund has seen strong interest recently and we recorded the highest number of subscriptions since inception in the month of April. These new investors should see an appreciation of their investments soon, as positive Vietnamese macro-economic data paired with a weaker dollar and thus stronger commodities should fuel an emerging markets rally which could go on much longer and further than most people think right now. In the first months of 2016, the real estate vacancy rate has fallen by around 10% and a perennial recovery of the sector is therefore likely to continue. However, it was this sector that was primarily responsible for the economic problems in the last cycle and the effects are still being felt today. Banks and the government are still struggling with non-performing loans and their consequences. In addition to the relatively low foreign reserves, the level of debt is an issue which the government needs to get a grip on during this economic upswing. In recent years, the debt level has increased due to various economic stimulus packages and infrastructure investments to the level of Malaysia and the Philippines, while the most affected countries during the Asian crisis of the 90’s, Thailand and Indonesia, have obviously learned their lesson. Due to economic growth prospects, Vietnam is in a much better position than many other countries and regions in this global debt spiral, especially when compared to Europe, where the government debt to GDP ratio has reached around 90%. Government Debt, percent of GDP On the other hand, the latest figures on foreign direct investments and the PMI (Purchasing Manager’s Index) confirmed a further improvement of the activity level of the Vietnamese economy. FDI Vietnam When looking at the current PMI numbers, the sub-component for new orders was very positive; certainly a strong driver to support economic development in 2016. Recent Apple numbers showed for the first time an apparent saturation of global mobile phone sales, which impacted many suppliers in South East and North Asia. Also in Vietnam the growth of exports in this sector was much lower than in the previous year, yet the total exports were up significantly, indicating that the economy is already more broad and structured than many observers have previously suspected. The Q1 interim results and AGM season will come to an end in the coming weeks. As usual, it shows a very mixed picture, and most management forecasts are extremely conservative. For our analytical model these interim reports are the least important of the year, but we hope to see first estimates for earnings growth in 2016, although we are very much aware of the quality of these estimates. At the end of April the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (3.1%) – a manufacturer of electrical and telecom equipment, Bao Viet Securities JSC (2.5%) – a securities brokerage company, Nui Nho Stone JSC (1.9%) – a stone mining company, Petrovietnam Fertilizer and Chemical JSC (1.9%) – a fertilizer manufacturer, and Doan Xa Port JSC (1.6%) – a logistics company. The portfolio was invested in 84 names and held 4.2% in cash. The sectors with the largest allocation of assets were consumer goods (34.5%) and industrials (24.2%). The fund’s estimated weighted average trailing P/E ratio was 8.18x, the estimated weighted average P/B ratio was 1.15x and the estimated portfolio dividend yield was 5.54%. For more information about Asia Frontier Capital’s Vietnam Fund please click the following links: Dubai/Pakistan Travel Report – April 2016In line with our process of being on the ground in the countries we invest in, Thomas Hugger and Ruchir Desai travelled to Dubai to attend a Pakistan Investment Conference. Though we usually write travel reports when we visit a country we invest in, this time we travelled to Dubai to meet Pakistani companies. Not that we would not like to visit Pakistan (which we have done in the past), but the investor conference presented a good way to meet a number of companies in a span of two days. Before writing more about Pakistani companies or about the country, a few lines about Dubai first. Dubai is quite a well organised and modern place (think Singapore) and the Dubai International Financial Centre (DIFC) - where the conference was held - is very conveniently located since it is only about a twenty minute drive to the airport. The DIFC has attracted a fair number of financial institutions to set up shop there and one can see a pretty big expat population at the DIFC. Dubai gets a large number of tourists, so there are more than enough hotels to choose from. The Burj Khalifa and the adjoining Dubai Mall are among the major attractions, the former because it is the tallest building in the world and the latter because it is so huge! Also, construction activity on new buildings was quite evident in the areas close to the DIFC. The Dubai Metro seems to be a good and convenient way to get around although we did not get a chance to use it since our hotel was within walking distance of the venue and luckily at this time of the year the weather was extremely pleasant to walk in. Quite a bit of construction activity in Dubai We met a diverse set of thirteen companies across the automotive, banking, cement, consumer staple, insurance, media, and power sectors and the mood amongst the corporates and other investors regarding the Pakistani economy in general was very positive. There are a few reasons for this positive mood. Lower crude oil prices have been a huge positive for Pakistan as crude oil accounted for ~26% of total imports before the drop in oil prices and this has helped bring down the country’s import bill and strengthen its foreign reserves position. Foreign reserves currently stand at about USD 20.3 billion which is an import cover of ~5.5 months. This is a much more healthy position than mid-2013 when foreign reserves covered only around 2 months of imports. Lower crude oil prices and that of commodities in general has helped bring down inflation and interest rates to record lows and this has led to an increase in sales of consumer discretionary goods as consumer disposable incomes have improved. Furthermore, the low interest rate environment has led to a pick-up in construction activities, which supported double digit growth in cement volumes over the past nine months. Macro Positives for the Pakistani Consumer Discretionary Sector Macro Positives for Pakistani Cement Companies Besides these positive tailwinds for the economy, another long term positive for Pakistan could be the China Pakistan Economic Corridor (CPEC), which will eventually connect Gwadar in Southwest Pakistan with Xinjiang province in Northwest China. The CPEC is a part of China’s One Belt One Road initiative and it consists of investing a total of USD 45 billon over a fifteen year period in power, road, and port projects. The majority of investments are expected to be in the power sector with a total of ~USD 34 billion to be spent on putting up new power capacity primarily using coal-based power plants. These new power projects are expected to lead to an increase of ~17,000 megawatts in generation capacity and this can go a long way in resolving the power deficit that Pakistan currently faces. Any improvement in the power situation will only be a positive for economic growth as there is a power deficit at present due to the mismatch between generation capability and demand. The other CPEC related investments are linked to infrastructure projects such as highways, rail networks, and ports. An important infrastructure initiative within the CPEC is the Gwadar port related project which besides further developing the port also includes an international airport and a highway. The CPEC could be a big positive for the Pakistani economy and though there is execution risk, the project is expected to be incredibly important geopolitically for both China and Pakistan.

Some of the companies we met were existing holdings and some we were meeting for the first time. From our existing holdings, we met with a pharmaceutical company which focuses on generic products which is currently the fund’s largest holding in Pakistan. It is among the top 10 pharmaceutical companies in the country in terms of revenue and it has a strong presence in the cardiovascular, gastro, and cough syrup space. Revenues and profits for the company have grown at a CAGR of 17% and 30% over the last five financial years respectively. This company is the fund’s second biggest position overall and has been among the top performers for the fund over the past two years. The other sector which we find interesting is the cement sector and both the cement companies we met were extremely positive about the outlook, which is not surprising given the growth in cement sales as mentioned previously. The fund is currently invested in two Pakistani cement companies and one of them has been a leading contributor to performance over the past year. Another interesting company we met was a hospital company which currently operates a hospital in Islamabad and Faisalabad and plans to expand capacity into Lahore. In addition to hospitals, the company also has a laboratory business which it could expand in the future. The fund is currently invested in this company. There was one bank present at the conference and the outlook for the Pakistani banking sector is soft as net interest margins are expected to come under pressure due to the reinvestment risk the banks face as a large portion of their government bonds are expected to mature in 2016. Having said that, most Pakistani banks are fundamentally sound in terms of loan loss coverage ratios and capital adequacy ratios. We also met with one of the leading auto companies and their sales growth over the past year has been in double digits. This has led to capacity constraints which they plan to overcome in the short run but they will need new capacity in the long run. The Pakistani automobile market does hold a lot of potential, as car penetration in Pakistan at 13 per 1,000 people is lower than India, which is 18 per 1,000 people. A new auto policy recently passed by the government could bring more investment into the country and may also lead to more competition which could possibly lead to new model launches by the existing players. This could be positive for overall growth in the industry. The government appears to be keen to reform as it looks to privatise certain state run entities, improve the law and order situation, and reduce the power deficit through greater investment via the CPEC. Though these are longer term themes, in the near term the country is in a better position relative to 2013 given low commodity prices and low inflation and interest rates which are expected to have a positive impact on the cement and consumer discretionary sectors. We do worry though about the impact of overseas worker remittances from the Middle East, as these account for ~65% of total remittances. Pakistan receives ~USD 19 billion of remittances and a significant slowdown would be negative not only for its current account deficit but could also dampen consumer spending.

|

||||||||||||||||||||||||||||||||||

|

I hope you have enjoyed reading this newsletter. If you would like any further information, please get in touch with me or my colleagues. With kind regards, Thomas Hugger |

|||||||||||||||||||||||||||||||||||

|

Asia Frontier Capital Limited |

|||||||||||||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Iraq Fund, AFC Iraq Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the funds in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. The AFC Asia Frontier Fund and the AFC Vietnam Fund are registered for sale to investors in Japan, Switzerland (qualified investors), Hong Kong & UK (professional investors), Singapore (accredited investors) and USA (accredited investors and qualified purchasers). The AFC Iraq Fund is registered for sale to investors in Switzerland (qualified investors), Hong Kong & UK (professional investors), Singapore (accredited investors) and USA (accredited investors and qualified purchasers) By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||||||||||||