Asia Frontier Capital (AFC) - March 2015 Newsletter |

|||||||||||||||||||

In this IssueAFC Asia AFC Vietnam Country Report: Fund

|

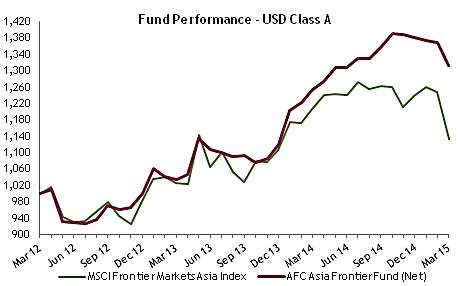

"My formula for success is rise early, In March 2015, the AFC Asia Frontier Fund returned –4.2% and the AFC Vietnam Fund returned -1.0%, bringing returns since inception to +31.1% and +37.3% respectively. Whilst both of our funds lost ground this month, March saw many stock markets around the world plummet to end the month in the red. The MSCI Frontier Markets Asia Index (-9.1%) saw a monumental slide due to strong selling pressure in the heavily index-weighted Pakistan. The MSCI Frontier Markets Index (-3.2%) and MSCI World Index (-1.8%) also saw a significant drop as equity markets pulled back after strong rallies in 2014. In Vietnam, the markets also took a tumble with both the Ho Chi Minh VN Index (-7.0%) and Hanoi VH Index (-4.1%) ending the month down after heavily index-weighted oil related stocks fell alongside oil prices. For the AFC Asia Frontier Fund, the biggest impact on performance was the drop in the markets in Pakistan as well as Sri Lanka. Pakistan has been undergoing a correction since the start of 2015 after local stocks saw a strong run up over the past 18 months. Corrections are part of any bull market and dips can offer buying opportunities. We see Pakistan still offering value and the Karachi Stock Exchange KSE100 Index currently has a P/E of 10.1x. In Sri Lanka there has been a pullback in markets with ongoing uncertainty around economic and investment policies after the change in government from recent elections. There have been continued investment inflows this month and we would like to extend a warm welcome to all of our new investors. Asia Frontier Capital’s AUM has now surpassed USD 25 million and this is expected to continue to grow even faster in conjunction with the upcoming launch of the AFC Iraq Fund on the 14th May 2015. AFC NewsAFC to Launch AFC Iraq FundAsia Frontier Capital is pleased to announce the launch of the AFC Iraq Fund, which will be open to initial subscription for investors at the end of April 2015 ahead of the official fund launch on the 14th of May 2015. The AFC Iraq Fund will build on AFC’s core strengths and excellent track record investing in frontier markets as well as our history of launching innovative, successful funds. There is more information on the fund launch in the AFC Country Report on Iraq later on in the newsletter and you can jump to this section by clicking (here). AFC in the Media

AFC Vietnam Fund collects Asia Asset Management Fund AwardThe AFC Vietnam Fund won ‘Most Innovative Product – Vietnam’ at this year’s Asia Asset Management Best of the Best Awards, and our Marketing Director Stephen Friel was on site to pick up this prestigious award in the last week of March. This award marks the latest height of success for our niche approach to investing in frontier markets, though it must be said that the apparent height of our Marketing Director is most likely due to the camera angle.

Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager Comment

AFC Asia Frontier Fund (AAFF) USD A-shares returned –4.2% in March 2015, outperforming the MSCI Frontier Markets Asia Index (-9.1%) whilst underperforming the MSCI Frontier Index (-3.2%) and MSCI World Index (-1.8%). This was one of the tougher months for AAFF since inception as most of the major markets saw a correction, but what stood out was the ability of the fund to not correct as much as its nearest benchmark, the MSCI Frontier Markets Asia Index. The major reason for this is that the benchmark is not very diversified, with heavy concentration in specific countries and stocks. For example, Pakistan has a weight of 46% in the index, while certain sectors like industrials and healthcare consist of just one stock i.e. 100% sector weighting. AAFF, on the other hand, runs a diversified strategy across countries and sectors. Furthermore, the fund has exposure to certain countries which are not part of the benchmark and has invested across both large and mid/small cap names which are not part of the benchmark. This ability of the fund to use a top down, bottom up benchmark-agnostic approach has held the fund in good stead when markets have been volatile, especially over the past few months. The major negative contributor for the fund this month was Pakistan, which saw the KSE-100 index correct by 10.1%, its biggest monthly decline since the August 2014 decline of 5.8% and the first time the index has dropped by more than 10% since May 2010. There were a lot of reasons as to why the market corrected during the month, ranging from the price running up to all-time highs,investigations by regulators into certain intermediaries and selling by certain foreign funds. Overall, however, nothing negative has occurred fundamentally in the economy. In fact there have been positives for the economy over the past few quarters such as lower oil prices, interest rate cuts, improving cement dispatches, and better GDP growth. However, we also observe that valuations for certain consumer companies have increased a lot and one would need to be selective in choosing such names. Cement and textile valuations are still attractive compared to consumer companies while banks have seen their valuations correct and this may provide an opportunity for the fund. In Vietnam, heavily weighted oil & gas and banking stocks corrected during the month as oil prices dipped while banks have rallied a lot in 2015. The fund has no exposure to oil & gas and banking stocks which helped reduce the decline for the fund. The fund’s Vietnam exposure at present is weighted toward consumer and infrastructure focused names. Valuations continue to be attractive in the companies we hold with P/E’s of less than 10x for most of the Vietnam holdings. In Sri Lanka, the continued uncertainty over the new government’s outlook on infrastructure projects led to retail investors selling an infrastructure company the fund holds. This holding continued to correct and the fund bought more of this holding as the revised order book projection appears to be factored in the valuations and it seems retail investors are selling on negative news. Bangladeshi banks corrected this month and the fund has no exposure to banks in Bangladesh. The fund has more weight towards consumer and healthcare focused companies in Bangladesh and these names held up well against a market decline. Iraq saw its market rally on the back of positive news of ISIS being pushed back and also because valuations have become very attractive. Our telecom and bank holdings did well during the month which led to positive returns from Iraq. In Laos, the power producer the fund holds also did well during the month. Overall it was the fund’s diversified approach as well as off benchmark exposure which helped it perform better on a relative basis than its benchmark. The best performing indices within the AAFF universe in March were Laos (+10.8%), followed by Iraq (+9.0%) and Cambodia (+1.9%). The poorest performing markets were Pakistan (-10.1%), Vietnam (-7.0%) and Sri Lanka (-6.6%). The top-performing portfolio stocks were a Mongolian oil exploration company (+64.3%), followed a Mongolian coal producer (+45.4%), an Iraqi mobile phone operator (+31.1%), and a Bangladeshi consumer product company (+30.1%). In March we sold three companies in Vietnam: a machinery company, a pharmaceutical company, and a software/IT company. Additionally we sold a Sri Lankan tile company. We also partially sold a small position in Vietnamese construction material company and added to existing positions in Laos, Mongolia, Pakistan, Sri Lanka, and Vietnam. As of 31st March 2015, the portfolio was invested in 118 shares and held 7.0% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.3%) and a shoe retailer in Bangladesh (3.7%). The countries with the largest asset allocation include Vietnam (27.8%), Pakistan (17.9%), and Bangladesh (14.4%). The sectors with the largest allocation of assets are consumer goods (41.2%) and materials (14.89%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 13.95x, the weighted average P/B ratio was 1.53x, and the dividend yield was 3.96%. AFC Vietnam Fund - Manager Comment

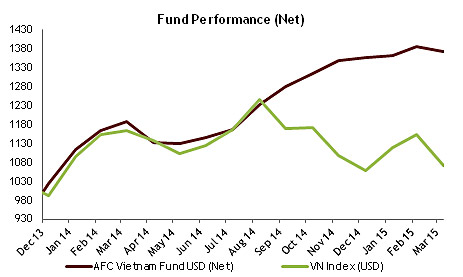

To read this month’s fund update in German please click here. In March 2015 the AFC Vietnam Fund returned -1.0%. This was a down month for the Vietnamese stock market with both the Ho Chi Minh Index (-7.1%) and Hanoi Index (-4.1) dropping significantly. For the first time in a long time, we have seen general tentative buying interests in a few selective stocks. Thanks to numerous asset inflows from several new and existing investors, we have looked to buy new mostly liquid shares from our buy list to take advantage of the current market weakness. From a technical point of view we are confident that the market will turn upwards from the current level. We hope that this will be a turnaround to a positive trend and will push through a technical rebound.

The reason for this market weakness of the past few weeks is not easy to clearly identify. Although the Frontier Asia index declined in March by approximately 9%, macroeconomic data is very good and the Vietnamese economy is progressing according to plan, as we were able to see firsthand on our investor tours last month. The GDP growth accelerated from 5.1% in Q1/2014 to 6.0% in Q1/2015. Although the trade deficit amounted to USD 1.8 billion, a lot of it is due to investments of machinery imports which will boost future exports. The main reason is probably the alleged margin calls of retail investors which are currently held (forced sellers of shares which were bought on credit). There were also larger redemptions in an ETF (exchange traded fund) which, given its size, had a strong influence on the current sell off in blue chips. After the steep increase in the first quarter of 2014, the Ho Chi Minh index declined by about 9% year on year in USD terms. During the same period, the share price of the Market Vectors Vietnam ETF, which manages around USD 400 million, fell by about 24%. Nevertheless for many Vietnam interested investors, this exchange traded fund still remains first choice!

As a comparison, it should also be mentioned that the AFC Vietnam Fund increased by approximately 15% over the same period. While we already expect the first quarterly results, we are in the midst of the shareholders' meeting season and are learning from the management teams about their financial targets for 2015 as well as investments and dividend payments. We are very glad that, due to our more quantitative approach, we do not need to rely on these statements as much. In the past, there has been a tendency for management teams’ projections to be unrealistic, irrational, and/or over-cautious, as seen recently with some slightly irritating management announcements. Two companies in the oil and gas sector, for example, have announced a large share buyback program a few weeks ago. This announcement was certainly very comprehendible given that both shares had recently experienced a heavy sell off of up to 50% in a very short period. Unfortunately, both companies didn’t execute this share buyback program as announced and when they did it was only to a very small extent. In the case of Petrovietnam Gas JSC (GAS), a company which is a heavyweight of the Ho Chi Minh Index, about 15% of all tradable shares should have been bought back within only one week up to almost 40% above the current share price. This was an unprofessional announcement considering that the buyback program was not performed and this type of behaviour is shaking the market’s confidence in the individuals responsible as well as companies. Should the implementation never have been planned despite the further fall in the stock price during this period, then this would make things even worse from a reputational aspect. This event highlights one of the frustrating sides of frontier capital markets to those who are not yet familiar: dealing with companies that do not always adhere to western requirements of transparency. Regardless of the size of the company, we see these weaknesses in many businesses which of course implies that there is a huge potential for improvement in the coming years as changes in corporate governance are improved and enforced. Precisely for this reason, we have a very well diversified portfolio in smaller companies which have simpler corporate structures which we expect to be a great advantage for generating returns in the coming years. In March, the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (4.9%) - a manufacturer of electrical and telecom equipment, Thuan An Wood Processing JSC (2.1%) – a household furniture manufacturer, Gypsum and Cement JSC (2.1%) – a gypsum and cement company, Thanh Hoa Beer JSC (2.0%) – a beer producer and Viet Thang Feed JSC (1.9%) – a livestock feed manufacturer. As of 31st March 2015, the portfolio was invested in 76 shares and held 14.3% in cash after a significant inflow of new funds at the end of the month. The sectors with the largest allocation of assets were consumer goods (33.0%) and industrials (19.9%). The fund’s weighted average trailing P/E ratio was 7.56x, the weighted average P/B ratio was 1.10x and the average dividend yield was 5.92%. AFC Country Report: Iraq – The post conflict opportunityTo mark the upcoming launch of the AFC Iraq Fund and to follow up on our recent in-depth coverage of Iraq in our previous newsletter (click here), this month we will be covering the post-conflict opportunity of Iraq.

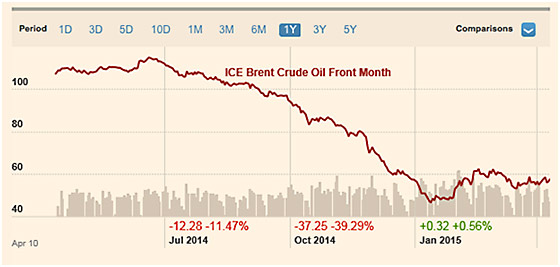

Country snapshots for all of AFC's markets can be found on our website at www.asiafrontiercapital.com In the past few months there have been a number of significant local/regional developments that are taking place that bolster our positive stance on Iraq and support our thesis of the impending end of the recent conflict. This should then begin the multi-year wholesale reconstruction of the country and economy of Iraq after 35 years of conflict. Recent Key Developments The Iraqi forces (made up of the regular army, popular mobilization units (militias organized under the command of the government) and local tribal fighters) recently liberated Tikrit with the help of some unlikely bedfellows in the form of Iran & the US (see below). This is the first military major victory for Iraq’s new inclusive government in rolling back ISIS and is a precursor for the liberation of Anbar (which fell in early 2014) and Mosul (which fell in mid 2014). Another incredibly important breakthrough was the solidification of the US-Iran détente in the form of the preliminary nuclear accord. The interests of the US & Iran have recently become significantly aligned, not only with the emergence of ISIS as a military threat, but also in addressing the conditions that gave rise to extremism. While the two are vocal in expressing their differences and non-cooperation, the actions on the ground show a high degree of de-facto coordination: the formation of the inclusive Federal Government of Iraq (FGI), the reconciliations between the autonomous Kurdish Regional Government (KRG) and the FGI, the containment of ISIS, and now the liberation of Tikrit. This alignment is in stark contrast to the conditions after 2003, in which the two sides fought a bitter proxy war in Iraq that contributed a great deal to the instability of the country. This détente extended further to relations with Turkey with last week’s visit of Turkish president Tayyib Erdogan to Iran and the drive to increase bilateral trade between the two from USD14bn to USD30bn. Moreover, the Turkish president argued that the two should resolve their differences and work together toward resolutions of conflicts in Syria and Iraq. The two countries are significant powers in the region and in spite of trade relations they fought bitter proxy wars in Iraq and Syria. Billions of dollars are pouring into Egypt, notably from the GCC, for the country’s reconstruction (a parallel Suez canal, a new proposed administrative capital city of up to 7m residents over 700 sq km plus a large number of mega housing projects). Many of these projects are intended to address the deep rooted needs of resource poor Egypt, with a young population of 85m people, 50% of whom are under the age of 25 whose needs for jobs and housing are extreme. These unaddressed needs gave rise to the Arab spring and were fertile grounds for the rise of extremism. This Marshall plan for Egypt is the region’s response to roll back the tide of extremism and would very likely be repeated in Iraq. Closer to home, our previous Iraq country report from November 2014 (click here) focused on the significance of the deal between the KRG and the FGI as a game changer and a precursor for unlocking the country’s potential. The agreement was forged as both parties realized, with the help of the international coalition, that they needed each other both in the fight against ISIS and for the eventual reconstruction of the country as a whole. The deal has faced many challenges since being signed, as neither side appears capable of delivering on all of its commitments. Production from the Kurdish controlled areas has fallen short of the agreed levels, while FGI doesn’t have enough cash to keep up with all the payments owed to the KRG. However, both parties are fully committed to the agreement and continue to collaborate. These challenges are unavoidable given the recent history of mistrust in Iraq and the actual logistical challenges of implementing both parts of the agreement in the difficult operating environment in the country. Further impetus for both parties to continue to work together is the stronger mutual benefits within the framework of détente in the region vs. the prior conditions which encouraged and fed their differences. Lower oil prices have proved to be a blessing in disguise for the Iraqi private sector, as they are forcing the government to adopt market friendly policies to encourage much greater private sector involvement in the economy with the most far reaching policies benefiting the private banking sector which will be the subject of a future report on Iraq. Finally, oil price prices, after collapsing in 2014, seem to have made a noteworthy bottom in early 2015. Although the short term rallies in Feb and early April were mostly for technical reasons and not sustainable, they have nevertheless established the floor for oil prices, as can been in the chart below.

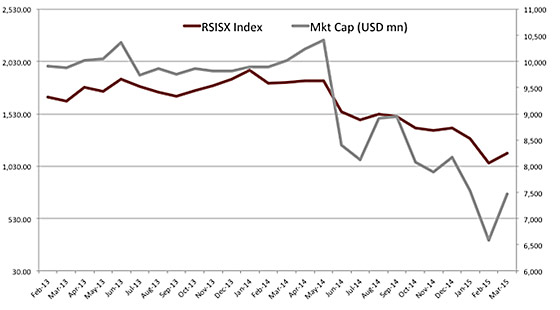

The cuts announced by the oil majors and most US shale companies should be felt in decreased supply towards the later part of the year while world demand should look better as we look towards 2016. However, the Iranian nuclear accord will tentatively see Iranian oil return to the world market in 2016 and increase supply meaningfully. Overall developments are likely to keep medium and long term oil prices in a range of USD60-70 as measured by ICE Brent Crude. The positives cited above bode well for the medium to long term outlook for Iraq, however near term challenges loom as the economy faces a number of hurdles in 2015 as it deals with multiple conflicting challenges. Chief among them is sharply increased military spending, which is forcing a diversion of economic resources, which are already strained by the significant drop in the budget as a result of lower oil prices. At the same time, the non-oil economy is struggling to deal with sharply decreased government spending, as it is the largest player in economy, while the need is for increased spending. In response the underdeveloped equity market has undergone a significant correction of around 27% as measured by the drop in total market capitalization from pre-crisis high as it discounts the near term effects on corporate earnings with the result that current depressed market valuations fail to reflect the medium and longer term potential of the country.

Iraq’s Stock Market

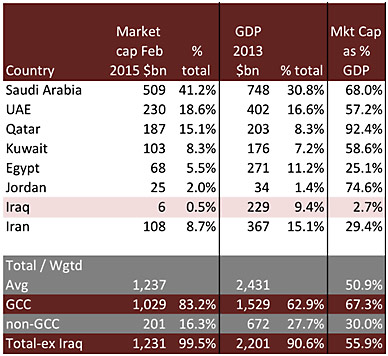

Total market capitalization was USD 7.5 billion as of March 2015 and the market cap to GDP ratio is under 4%. This is significantly lower than countries in the MENA region which have the same ratio at levels between 25%-90%, which highlights the scope of potential developments for Iraq’s capital markets over the coming years.

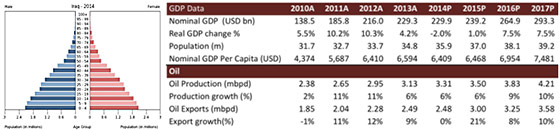

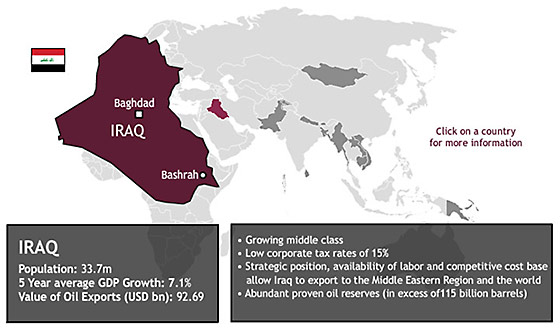

Iraq’s Economy Iraq’s economy witnessed significant growth following 2003, contracted by 2% in 2014, and is now on track to recover in 2015 with 1% growth and projected growth above 7% until 2018. Iraq is still a country with enormous potential for wealth in spite of the devastation of over 35 years of terrible conflicts, crippling sanctions, ugly civil strife, and the ISIS conflict. Energy lies at the heart of the Iraq’s wealth and this will be a key impetus for growth in the future. It has the world’s 5th largest proven oil reserves at approximately 9% of total reserves, which could potentially rise to as much as 15% as further oil fields are explored and developed. Iraq also has world’s 12th largest gas reserves with about 2% total resources. On top of this there is also a wealth of minerals resources including phosphate, crucial to modern agriculture, in which it has the world’s second largest reserves at 9% of total resources. When this is combined with its significant human capital advantages when compared regionally, Iraq’s population of 35.9 million will certainly benefit. The local population is growing by over 3% per annum and is extremely young, with 56% under 25 years of age, which will be a key driver of growth.

About AFC Iraq Fund All of the aforementioned factors have created a situation in which current market prices in Iraq are significantly below their future potential offering an incredibly opportunity for forward looking investors. The AFC Iraq Fund will execute an actively managed niche strategy that gives investors access to the upcoming recovery in Iraq via a compliant fund structure that offers monthly liquidity to investors. The AFC Iraq Fund will be launched on the 14th May 2015 and will build on AFC’s core strengths, excellent track record investing in frontier markets as well as our history of launching innovative, successful funds. The AFC Iraq Fund is managed under the executive leadership team of Thomas Hugger (CEO & Fund Manager) and Ahmed Tabaqchali (CIO) who between them have more than 47 years of investment experience as well as extensive background covering emerging, frontier, and MENA markets. AFC is a strong advocate for the potential of frontier markets and our new Iraq offering holds incredible value for risk-conscious investors looking for high long-term investment returns. Our core thesis is that post-conflict countries are unique phenomena for investors offering large potential returns as the countries begin to reap the benefits of the peace dividend as they transition from conflict to economic growth with the peace dividend proportional to the resources at hand and the rebuilding required. Iraq’s attractiveness within these phenomena is its vast resources (hydrocarbons, minerals, agricultural & sizeable human capital) and the rebuilding required after over 35 years of conflict as the country has gone through wars, crippling sanctions, civil strife, and the ISIS conflict. Moreover, we are positive about the confluence of major regional developments that are currently taking place just as Iraq emerges from conflict, chief among them being the detente between the West and Iran, that will boost and sustain Iraq’s transformation. The AFC Iraq fund will be positioned to take advantage of this situation to capture the upside of Iraq’s wealth of natural resources and strong underlying fundamentals. The fund will invest in companies leveraged to Iraq’s recovery and seek to arbitrage the perceived risk gap, which we see as being significantly higher than the actual risk. Equity markets in post-conflict Sri Lanka saw a rally of +250% in the 18 months after the end of its civil war even without the significant resources to rebuild that Iraq has on offer. Other post-conflict country stock markets have also seen significant rallies in the immediate years after conflict. Iraq’s equity markets are at their infancy, at under 4% of GDP, with potentially a significant catch up to peers in the region in years to come. The underlying fundamentals for Iraq are strong and improving, and any slowdown or halt to conflict will have a significant positive impact on the domestic market in the next economic cycle. Being positioned to capture the opportunities of post-conflict Iraq could mean a potential increase of several hundred percent in local terms and even greater upside when coupled with extremely depressed valuations that exist at present. AFC’s Asia Frontier Fund has been building its Iraqi expertise through its equity investments in Iraq for over two years and has significantly expanded this expertise with the addition of Ahmed Tabaqchali, an Iraqi/British national, who has extensively covered the MENA & global equity markets for over 22 years and leveraged this experience through coverage of Iraq’s investment prospects from the ground. If you would like to find out more about investing in Iraq, please contact our Iraq team at AFC Travel Report: Vietnam Investor TourIn line with our process of being on the ground in the countries we invest in, AFC's research team of Thomas Hugger, Andreas Karall, Andreas Vogelsanger, and Scott Osheroff spent a week visiting companies across Vietnam in March 2015. During the final week of March, Asia Frontier Capital organized a five day Investment Tour to Ho Chi Minh City (HCMC) and Hanoi, Vietnam. We held this tour to showcase to existing and prospective investors the reality and great prospect of Vietnam’s economic prowess and the real possibility of it becoming the next “Tiger Economy”. Our gathering started on a Sunday’s eve where we had drinks followed by dinner at the Majestic Hotel, a luxurious French colonial hotel overlooking the Saigon river and the city’s new metro project under construction. Since Vietnam is a former French colony, there still exists plenty of French colonial architecture all over the country making Vietnam a unique place to visit. In addition to the Majestic Hotel, a dinner several days later was held at La Villa French Restaurant in a refurbished French Villa in the outskirt of Saigon – the colonial name of Ho Chi Minh City.

At the onset of the business leg of our trip, Michel Tosto, Head of Institutional Sales & Brokerage of VietCapital Securities, provided us with valuable insights about the general state of the economy and its future outlook. The majority consensus is that the economy will continue to expand at a pace of over 6% in 2015 due to a low inflation environment and stable currency. Non-performing loans (NPL) on bank’s balance sheets will continue to decrease as the government purchases additional NPL’s through the state owned Vietnam Asset Management Company. Additionally, mergers in the banking sector and the first signs of a recovery in the real estate sector will lead to increased foreign investment and an easing of the current strain on banks. Andy Karall, Fund Manager of the AFC Vietnam Fund, briefed the participants in detail about the fund’s investment strategy and investment outlook. The fund strategy is – contrary to big fund houses – to search for undervalued and overlooked companies in the small- and mid-cap space, which are normally not researched by brokerage houses and global institutions. Andy has successfully demonstrated during the last 16 months that this strategy can provide a significant investment return. We also invited Marc Townsend, Managing Director of CBRE Vietnam, to provide an overview about the real estate market. While it is mainly the affordable housing segment showing robust signs of improvement, there are other positive indicators including the rise in newly registered real estate companies increasing 88% during 2014. Increasing discretionary spending will lead to an absorption of excess real estate supply and also see international retailers enter the market. Some of the more recent entrants to Vietnam include Gucci, Prada, Brooks Brothers, etc. According to CBRE, approximately 80% of foreign direct investments in the first 2 months of 2015 went into the manufacturing sector while the next biggest allocation was real estate at roughly 9%. Several listed companies also showcased their operations to us. Some of the companies we met, such as Mobile World (MWG), an electronics retail chain with a strong focus on mobile phones, demonstrated their ability to control a significant market national share as they have developed an in-house logistics network and have paid particular attention to customer service. This has helped drive growth and will enable the company to move into new industries with their integrated network and understanding of the Vietnamese consumer. Another listed company from the consumer sector was Phu Nhuan Jewelry (PNJ), a jewellery company producing for their domestic brand as well as offering OEM to select major international retailers like Tiffany & Co. PNJ outlined their strategy for continued robust growth by offering customer friendly service together with a high quality product portfolio at competitive prices. Having also visited several factories, one of the standouts was Vinamilk (VNM), the largest dairy company in Vietnam. Visiting a state-of-the-art facility, our group suited up with food safety uniforms providing a fun photo opportunity. During the tour we saw a highly mechanized operation comprised of multiple ABB robots and high-tech Swedish packaging equipment.

We also visited Thien Long Group (TLG), a leading office supplies manufacturer with an international reach. Their main product is the fabrication of pens, something we all use in our daily lives and which won’t be disappearing even as we enter this digital age, a point the CEO of the company highlighted pointedly. Having seen their vertical integration from dye manufacturing to pen production, a pen is a sophisticated object TLG has become an expert at producing. This is a company with a bright future as they continue to grow rapidly.

Mid-week we flew north to Vietnam’s capital, Hanoi, where we visited several other companies. Comparing the North and South is always interesting as of today, there still exists a divide between the two due to historical reasons dating back to when the US supported the South in the Vietnam War. While the South hosts a larger population and thus more manufacturing, the North is home to a significant portion of the country’s wealth and elite. This wealth is quite prevalent as we stayed in the Old Quarter of Hanoi where not more than a few meters from our hotel were Vertu, Prada, Pandora, and several other luxury stores. On the last day of our trip we decided it best to take a break from company visits and reflect on our experiences from the past four days. We therefore drove four hours north-east of Hanoi to Halong Bay, a UNESCO World Heritage site, where we boarded a junk and absorbed the beautiful landscape over a wonderful seafood lunch. Boating through the waterways between over 1,000 limestone islands was an ideal way to conclude our journey and discuss the real potential Vietnam has to become a regional economic powerhouse.

|

||||||||||||||||||

|

I hope you enjoyed reading our monthly newsletter. If you would like any information about our funds or markets please let me know. With kind regards, Thomas Hugger |

|||||||||||||||||||

|

Asia Frontier Capital Limited |

|||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||

GO TOP |

|||||||||||||||||||

Source: VietCapital Securities

Source: VietCapital Securities Source: Yahoo.com

Source: Yahoo.com

Source: Financial Times

Source: Financial Times ISX total market cap vs the RSISX Index developed by Rabee Securities

ISX total market cap vs the RSISX Index developed by Rabee Securities