Asia Frontier Capital (AFC) - May 2015 Newsletter |

||||||||||||||||||||||||||||||||||||||||||||||

In this IssueAFC Asia AFC Vietnam Fund

|

"Negotiate a river by following its bends, In May 2015, the AFC Asia Frontier Fund returned -0.3% bringing YTD returns to -2.1%. This month the MSCI World Index (+0.1%) remained relatively steady whilst the MSCI Frontier Asia Index (-2.2%) and MSCI Frontier Markets Index (-4.1%) both dropped significantly in May. It has been a difficult start to the year for frontier markets but the AFC Asia Frontier Fund has remained resilient during the recent downturn. Since the recent NAV high on 31st October 2014, the fund has given up only -3.1% (net) whilst the MSCI Frontier Asia Index and MSCI Frontier Markets Index have lost -7.8% and -13.4% respectively over the same period. Looking at Vietnam, the AFC Vietnam Fund returned -0.5% bringing the YTD returns to +2.7%. The Ho Chi Minh VN Index (+1.3%) and Hanoi VH Index (+0.6%) were both in positive territory in May after a rally during the month but they are still significantly underperforming versus the AFC Vietnam Fund. Since the fund’s inception the indices’ returns have underperformed by 30.1% and 21.4% in USD terms over the same period. Across Asia there was a combination of both good and not so good news for our markets in May. One of the positives was the long awaited news out of Mongolia with the government has finally reached an agreement with Rio Tinto to restart the USD 5-6 billion Oyu Tolgoi (OT) project. Over the past 18 months, the continued disagreement between OT and the Mongolian government acted as a catalyst for a significant drop in FDI, as well as government revenue, and the dispute generated a great deal of uncertainty around the ability to execute investments as a foreign investor. During this period the dispute was seen as a canary in the coal mine for FDI, causing many companies to put projects on hold or withdraw Mongolian expansion plans as the ability to work easily with the government on issues such as licencing, project financing, and taxation became much less clear. With the drop in global commodity prices, the impact on the Mongolian economy was quite severe, with the balance of payments dropping into the red and the currency falling more than 30%. Taking a contrarian view, the AFC Asia Frontier Fund had already accumulated Mongolian equities that we saw pushed to undervalued levels and had positioned its Mongolian holdings (currently 9.1% of the portfolio) to capture the upside of a turnaround in the markets when one or both of these issues causing supressed markets were eventually resolved. Since the announcement of the OT project on the 18th May, the MSE Top 20 Index has climbed +7.1% and the currency has recovered +3.6% as of 8th June. Looking at one of the negative events in Asia in the past weeks, the earthquake that struck Nepal has been a continuing tragedy with the country being hit by an aftershock causing even further destruction to the now fragile nation. Nepal is one of the poorest countries in the world and the immediate damage was devastating, with more than 500,000 homes destroyed and more than 8,000 people killed as well as tens of thousands injured. The ongoing consequences of this event will continue to put the limited resources available in the country under stress in the months to come as the country and economy try to recover. The earthquake also halted markets with some of the Nepal Stock Exchange buildings being badly damaged, causing the exchange to be closed for one month after the April 25 earthquake. The exchange is now running well given the circumstances and they even have had time to release an update explaining how each listed company was impacted (available here). Natural disasters are very difficult to predict and their dramatic effects represent an external shock to the local markets where they strike. This type of event can happen across global geographies without warning and can impact livelihoods (particularly in developing countries) as well as investment holdings which highlights why a disciplined approach to diversification is needed. There have again been strong investment inflows this month and we would like to extend a warm welcome to all of our new investors who have helped to grow Asia Frontier Capital’s AUM since Thomas’ MBO in June 2013. Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact our Marketing Director Stephen Friel at

AFC Iraq Fund UpdateAsia Thus far the launch of the AFC Iraq Fund has received a warm welcome with many new investors looking to get in ahead of the first NAV. As with many things in frontier markets, however, administrative processes can move slowly from time to time and as a result there has been a slight delay in the launch date for the fund. We expect the final small pieces to fall into place over the coming days and then initial investments to commence immediately afterwards. With this in mind, it is still possible to come on board as one of the initial investors in the fund. If you have any questions or would like any more information please contact Market Commentary

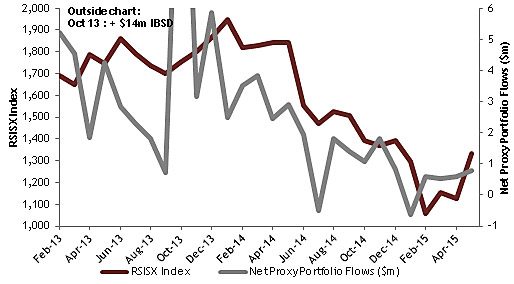

*Note: the disconnect between the market cap and the price index is due to the exclusion of market cap heavy weight AsiaCell with 31% of total market cap from the price index due to low liquidity and which was down 10% during the month. Such anomalies are and will be the case for illiquid markets such as Iraq and will be the subject of a future newsletter. So what gives? The negative news is far from a good sign but it is nowhere near as bad as reported by the media which is not surprising considering the underlying realities in Iraq. These realities are a reflection of the state that Iraq has found itself in after the past year and although it has embarked on a course of recovery, with the aid of the unprecedented international collation, this course requires significant time to implement. This will be far from a linear process, but progress is progress, and we are confident in an ultimately successful conclusion and brighter prospects for Iraq. To put this in context, Ahmed Tabaqchali, CIO of the AFC Iraq Fund, has given insight to provide a highly relevant synopsis of Iraq’s unique history and political situation, available by clicking on the following link: (click here) The ABC has also released interesting news report on the rebuilding of Iraq focussing on one of the new mega-projects outside of Baghdad. The video is available by clicking on the following link: (click here) The outlook for the equity market: As significant as this development is, the mechanism of implementation has not been decided as of yet. Crucial lending policies as well as the ultimate responsibility for risk has also not been decided and this will probably be subject to debate over the next few months. These and other developments in Iraq are long term positive forces that will bear fruit in the future but will require a long term patient approach. The investment strategy of the AFC Iraq Fund aims to take advantage of this interim period to acquire attractive assets at depressed valuations. Taking this approach, we expect that markets will push these assets to be fairly valued in time and will yield significant returns for patient investors. Finally, the chart below shows that the market’s action was mostly driven by local investors while international portfolio flows, as tracked by our proxy for them, seemed to have stabilized for the first time in many months. Time will tell if the positive price action in the market will encourage short run foreign flows into the Iraq stock market. Our belief is that the timing of the launch of the AFC Iraq fund is at a very attractive entry point as the inflection point is near but not discounted yet.

*Note: Net Portfolio Proxy Flows is developed by AFC as a proxy for portfolio flows taken from IDC monthly reports. The Net Proxy Portfolio Flows figure outside the chart represents a significant unique inflow into Baghdad Soft Drinks (IBSD) AFC Asia Frontier Fund - Manager Comment

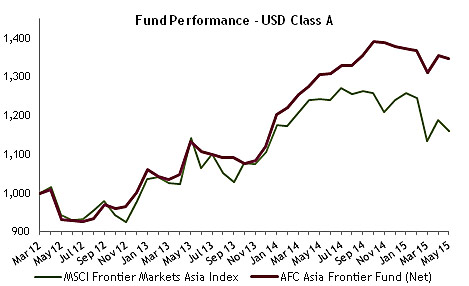

AFC Asia Frontier Fund (AAFF) USD A-shares lost –0.3% in May 2015, outperforming the MSCI Frontier Asia Index (-2.2%) and the MSCI Frontier Index (-4.1%) but underperforming the MSCI World Index (+0.1%). The month did not see any major events or market impacts but the fund did better than the benchmark because, as mentioned in previous newsletters, the diversified and non-benchmark approach has helped the fund during times of market volatility. There was no major negative news from Bangladesh in the past month, helping the market to rally despite the tense political situation since beginning of the year. The rally was led by certain companies in the banking and oil sectors. Overall, the fund’s consumer and healthcare holdings did fairly well, with the fund’s largest position up +16% during the month. Pakistan saw a slight correction as banks and cement companies experienced some dips. Though Pakistani banks have shown good numbers in 2014 and in 1Q2015, the outlook post 1H2015 is a mixed picture as there is uncertainty on earnings growth and net interest margins (NIMs). Overall, certain banks are well managed and some are cheap relative to peers, which could provide an attractive entry point but the fund has not made any new investments in bank holdings besides the one bank that it holds. The government also passed a bill in the assembly which will implement a new gas related tax which will have an impact on the cement, fertilizer, and power sectors. Overall, this tax is good for the economy as it will help the government manage its deficit, but sentiment turned negative for the affected sectors during the month. The fund holds two Pakistani cement companies which are the lowest cost producers in the sector, and in the past, given the structure of the industry, cost increases have been passed on to customers. Furthermore, domestic dispatches over the past few quarters have been showing good numbers. Automobile sales have also picked up over the last few months due to new model launches, government schemes, and the low interest rate environment. Motorcycle sales for the largest motorcycle company were up 20% year over year in April 2015. The fund holds one company in the Pakistani automobile sector. On the macro front, with inflation coming under control due to low oil prices, the central bank cut benchmark interest rates by 100bps to 7%, the lowest in the past 24 years. Market sentiment in Sri Lanka continues to be dependent on signs from the new government regarding their future economic agenda as well as the upcoming parliamentary elections in the next few months. Vietnamese banks rallied during the month which led the upward market movement. There was some heightened tension in the retail market as the South China Sea territorial dispute picked up again due to the U.S. moving military aircraft and ships close to the Spratly Islands. Last year China moved an oil rig into the disputed waters which led to a large correction and protests in Vietnam so any news related to this issue has had an impact on market sentiment. This could create a good opportunity to buy if there is another correction due to this issue, as there was last year, as economic numbers coming out of Vietnam continue to be positive. In Mongolia, the fund has been invested in the country since inception with a current exposure of 9.1%. This should help the fund given the positive developments surrounding the resolution of the Oyu Tolgoi project which can be a positive trigger for Mongolian equities going forward. The best performing indices within the AAFF universe in May were Iraq (+18.0%), followed by Bangladesh (+13.8%) and Vietnam (+1.3%). The poorest performing markets were Cambodia (-4.6%) and Laos (-4.6%). The top-performing portfolio stocks were a Bangladeshi holding company (+57.7%), followed by an Iraqi insurance company (+37.5%), a Cambodian mining company (+23.7%), and a Sri Lankan consumer goods company (+22.8%). May was a busy month as we shifted various positions: we partially sold three Pakistani companies, three in Vietnam, and one each in Bangladesh and Mongolia. We added to existing positions in Iraq, Laos, Mongolia, Pakistan, Sri Lanka, and Vietnam. We completely exited a Pakistani power producer, a Sri Lankan bank, and a Sri Lankan tile company. We added new positions to the portfolio in a Sri Lankan tile company and a Mongolian coal mine. As of 31st May 2015, the portfolio was invested in 116 shares and held 6.5% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.6%) and a Pakistani pharmaceutical company (3.5%). The countries with the largest asset allocation include Vietnam (27.9%), Pakistan (17.6%) and Bangladesh (13.5%). The sectors with the largest allocation of assets are consumer goods (41.2%) and materials (14.9%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 13.88x, the weighted average P/B ratio was 1.59x and the dividend yield was 3.69% AFC Vietnam Fund - Manager Comment

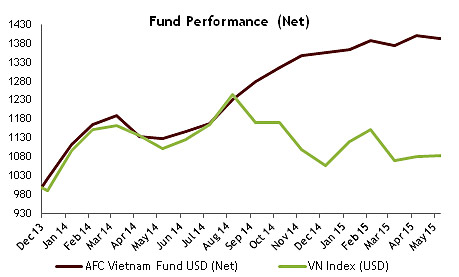

To read this month’s fund update in German please click here. In May 2015 the AFC Vietnam Fund returned -0.5%. Similar to the same time last year, the market was quite weak at the beginning of the month and then recovered strongly towards the end of the month mainly due to a rally in banking stocks. The Ho Chi Minh Index closed the month up +1.3% and the Hanoi Index closed the month up +0.6%. In local currency terms, we managed to close the month in positive territory, but in USD we closed slightly negative, mainly due to the Dong devaluation, our low beta, and the high index weighting of some of the banks. The fund’s extremely low beta of 0.6 means that will participate only +/- 0.6% with a daily index move of +/- 1%. In the longer term however, we expect to outperform the market with our stock selection as we have successfully demonstrated in the past. The Q1 earnings season has now been completed and we can draw several conclusions for our portfolio. As in recent quarters, the business results of our invested companies are quite diverse, but overall we see at least the same growth as in Q1 2014 and expect all of them to be profitable this year. The recently purchased oil and gas stocks show, in contrast, small but solid earnings growth. Nevertheless, they are now attractively valued after their recent stock price decline of almost 50%. During the recent market weakness, we added a few larger companies to our buy list. Adding more and more larger companies to our portfolio is in line with the growing assets in our fund, in order to ensure appropriate liquidity of our underlying positions in relation to the fund size. With around 100 current investible companies, we are able to easily absorb large fund inflows, without diluting the return expectations.

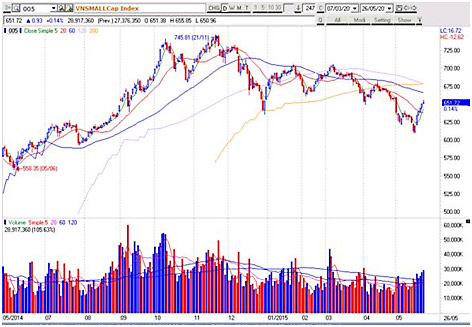

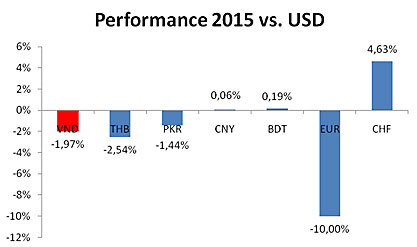

The chart above shows the current upside potential of small caps, which are still trading around 10% below their peak in November 2014, whereas large caps have already started trending upwards. In early May, the Vietnamese currency was devalued by another percentage point. Thus, the currency band is (+/- 1%) to USD at an average of 21,673 to 21,458 VND/USD and is currently trading at around 21,800 VND/USD. This measure is designed to maintain the competitiveness of Vietnam against its main trading partners. In order to further develop the export power of Vietnam, a competitive exchange rate development versus the US, but also versus Japan and China, in particular, are of immense importance. The graph below, comparing some of Vietnam’s competitors as an export country, clearly shows that only Bangladesh and China’s currency were stable versus the USD. The State Bank of Vietnam (SBV) reaffirmed last week that it will not depreciate the VND any further from now until the year end.

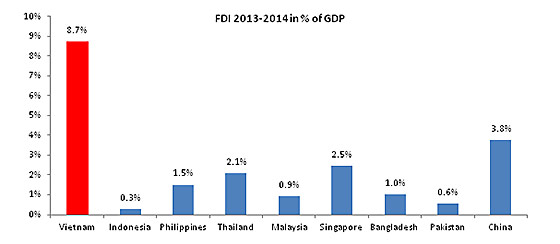

However, these currency movements should not be overstated, because the monthly exchange rate fluctuations against the CHF and the USD since the launch date of our fund have been almost 0 and only against the Euro we had a monthly appreciation of approximately 1% (due to the weakness of the Euro). Regarding important macro-economic data relevant for the stock market, Foreign Direct Investment (FDI) in particular is worth mentioning. During the first 4 months of the year they reached an impressive USD 3.7bn which is almost the same level as the same period last year. This compares very favorably with similar countries such as Thailand. New foreign investment is also very important to increase knowhow and technology in Vietnam in order to move the country up the value chain as the economy develops.

Our current portfolio is well diversified, and with an average P/E ratio of only 7.33x, more than a 50% discount to the regional and international markets. We are well positioned and are waiting for the next sustained rise in the Vietnamese stock market, which may have already been initiated with the soon to be expected change in the Foreign Ownership Limits (FOL).

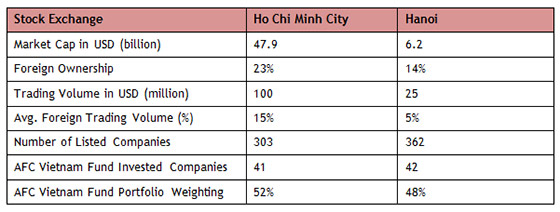

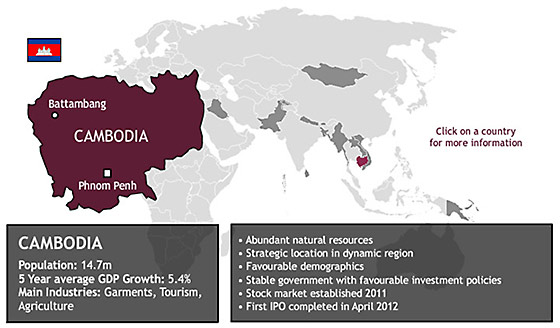

The split of company listings between HCMC and Hanoi is about 50/50. Our stocks have a total market combined market capitalization of USD 10 billion (total market cap of HCMC and Hanoi 54 billion). In May the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (4.1%) - a manufacturer of electrical and telecom equipment, Bao Viet Securities JSC (1.9%) – a brokerage company, Thuan An Wood Processing JSC (1.7%) – a household furniture manufacturer, Danang Housing Investment Development Company (1.5%) – a construction company, and Nui Nho Stone JSC (1.5%) – a construction materials company. As of 31th May 2015 the portfolio was invested in 85 shares and held 11.5% in cash after a significant inflow of new funds at the end of the month. The sectors with the largest allocation of assets were consumer goods (32.9%) and industrials (22.2%). The fund’s weighted average trailing P/E ratio was 7.33x, the weighted average P/B ratio was 1.13x and the average dividend yield was 6.09%. AFC Country Snapshot: CambodiaAfter decades of political mismanagement and civil war, Cambodia has recently begun to capitalize on its economic potential. Since adopting free-market economic policies in the 1990’s and increasing its integration within the international community, Cambodia’s economy has flourished. From 1998 to 2007, Cambodia’s GDP growth ranked sixth in the world (9.8%) and fastest in the Far East after China. Cambodia’s continued upward trajectory will be driven by several factors. Cambodia is resource-rich with newfound offshore oil and gas deposits in the Gulf of Thailand and mineral deposits in the northern provinces. Tourism is also growing quickly, as Cambodia is home to pristine beaches, world-class cultural relics (Angkor Wat), and a burgeoning eco-tourism sector. Cambodia also benefits from a young and cheap workforce and a growing middle-class

Stock Market:

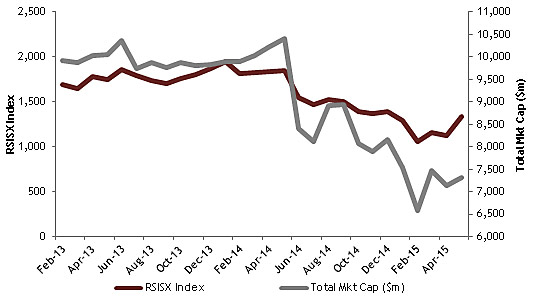

AFC Country Report: CambodiaEven among the fast-paced and ever-developing frontier markets of Asia, Cambodia certainly stands out for its dramatic turnaround. Twenty years ago, Cambodia was an aid-dependent, post-conflict country with an economy in ruins and a population on edge after having experienced such a violent recent history. The Khmer Rouge genocide and “Year Zero” killed millions of the country’s people and wiped out nearly all of Cambodia’s teachers, artists, and intellectuals. Fast forward to today, and Cambodia has one of Asia’s fastest growing economies, attracting an increasing amount of foreign investment and gradually making its way onto the radar of an increasing number of investors. According to The World Bank, Cambodia’s economic growth averaged 7.7% between 1993 and 2013 – the sixth fastest growth rate of any economy in the world – and per capita income increased by more than 3.5x, from USD 248 to USD 878. The country’s cheap labour force has propelled a huge surge in the garment industry, which is the largest export sector for Cambodia and employs 650,000 workers, 90% of whom are female. With the upcoming ASEAN Economic Integration in the works, many large Asian conglomerates and strategic investors, particularly from Korea, China, Japan, and Thailand, have identified Cambodia as an attractive investment locale that stands to benefit significantly from Southeast Asia's forthcoming eased tariff restrictions and growing intra-ASEAN trade. One challenge for Cambodia in its quest to attract investors has been the development of the country’s stock exchange, the Cambodian Securities Exchange (CSX), which was established in 2011. More than three years after the debut listing on the bourse of Phnom Penh Water Supply Authority (PPWSA) in April 2012, only two stocks currently trade on the CSX and share prices have declined steeply. In July 2014, the CSX saw the listing of a second company, Grand Twins International, a Taiwanese garment maker looking to raise funds for further expansion. The listing of Grand Twins, however, received lukewarm enthusiasm from investors partially because of the country’s deadly garment worker protests and wage strikes in January 2014 that received international media attention and cast a dark cloud over the garment industry in Cambodia. Trading volume on the exchange has since slowed dramatically, and the initial fanfare surrounding the launch of the country’s stock market has very much cooled. A potential snag for the growth of the bourse could be the lack of a listing of a strong Cambodian company operating in an industry that investors have traditionally favoured in emerging/frontier markets, such as telecoms, banks, or cement. ACLEDA Bank, the country’s largest bank measured by assets that has recently expanded to Myanmar and Laos, has discussed a possible IPO for several years, but has yet to formally declare plans to list. Telecom Cambodia and Sihanoukville Autonomous Port have also both discussed plans to list in the past, but nothing definite has come to fruition. In late May 2015, it was announced that Phnom Penh Autonomous Port (PPAP), the second largest port in the country, is aiming to list on the CSX by November 2015 to raise funds for the development of a new terminal. The capital raised in the offering will be used to double the terminal’s capacity to 300,000 containers from its current 150,000. Due to the growing pains of the CSX, foreign investors have found other ways to access the Cambodian growth story through companies listed on exchanges outside of Cambodia. NagaCorp, the Hong Kong-listed casino and gaming operator that owns NagaWorld Casino & Resort in Phnom Penh, has exhibited strong growth and outlined plans for further expansion in the Kingdom. In May, NagaCorp announced that it had agreed to a 10-year deal with several independent investors to raise USD 40 million to develop a new 300-unit electronic gaming machine (EGM) for its NagaWorld Casino in Phnom Penh. This announcement came on the heels of a statement by the company that it expects its 1H 2015 net profit to rise by at least 40% year-on-year. NagaCorp’s strong performance has partially been attributed to the rise in inbound tourists from China and Vietnam, which grew 14.9% and 18.9% in Q1 2015 year-on-year respectively. NagaCorp is also developing a shopping complex next to its Phnom Penh casino and has begun offering direct flights to Macau and mainland China in a push to compel more gamblers to choose Cambodia over Macau.

NagaCorp is not the only publicly-listed gaming operator with its sights set on Cambodia. Australia-listed Donaco International recently paid USD 360 million for Star Vegas, the leading casino in Poipet, the Thai-Cambodian border town that does a thriving business in gambling. Donaco also owns a casino in Vietnam near China’s Yunnan Province, and sees its acquisition in Poipet as a large growth opportunity due to the fact that casino gambling is illegal in neighbouring Thailand. Another regionally listed company that has achieved success in Cambodia is Group Lease PCL (“GL”), a Thai company listed on the Stock Exchange of Thailand (SET) that leases motorcycles and farm-machinery as well as providing nano-financing. GL’s Cambodian subsidiary broke even in 2 years, and the Thai-listed company recorded a record high net profit in Q1 2015 of THB 110 million (USD 32.7 million), 35% of which came from the company’s non-Thai operations, with Cambodia accounting for the majority of these earnings. Quarterly net profit was up 77% quarter-on-quarter, and the share price has surged +105% in the last six months. The company plans to continue its regional expansion, setting up a new subsidiary to develop its business in Laos and reportedly eyeing Indonesia as well. Despite political gridlock and opposition protests surrounding the July 2013 election, political stability has resumed and investor confidence seems to have largely been restored, with Cambodia continuing to position itself as an investor-friendly destination for investment with a pro-business government and sound macroeconomic outlook. Location and accessibility remain another strong point for Cambodia. Within a 1.5 hour flight, one can reach 600 million consumers (including China’s Yunnan Province), and with labour costs increasing in China’s traditional manufacturing hubs and Vietnamese factories moving up the value chain, Cambodia presents a strong opportunity for manufacturers looking to lower costs by relocating.

Although Cambodia’s capital, Phnom Penh, and tourist jewel, Siem Reap, have developed rapidly, the country remains relatively rural and undeveloped, with roughly 80% of the population still working in agriculture. There is a massive infrastructure need to continue to improve living standards in the country’s rural provinces, underscoring the reasoning behind Cambodia’s decision to join the China-backed Asian Infrastructure Investment Bank (AIIB), which has generated plenty of controversy in the news due to the United States’ relative condemnation of the new development bank. The Cambodian government has estimated that it will need USD 1.6 billion from 2014-18 to develop infrastructure needs in the Kingdom, primarily roads, railways, power, electricity, telecoms, and water and sanitation projects. The Japan International Cooperation Agency (JICA) and International Monetary Fund (IMF), meanwhile, forecast in 2011 that Cambodia would need USD 13 billion for its infrastructure requirements through 2020. Some analysts, however, have expressed concern that Cambodia may rely too much on external financing from the AIIB for its infrastructure needs and that the Bank will further extend China’s sphere of influence on its poorer ASEAN neighbours like Cambodia. In addition to the AIIB, other analysts have pointed to the potential benefits of Cambodia joining a regional trade partnership, such as the Regional Comprehensive Economic Partnership (RCEP), a Chinese-backed treaty established in 2012. Admission to the RCEP could help pave the way for Cambodia to apply to be a member of the Trans-Pacific Partnership (TPP), which would provide access to a huge market for Cambodia’s goods and likely help to attract foreign companies interested in establishing factories in Cambodia. From an investor’s perspective, the Cambodian economic growth story has been impressive overall, particularly considering the country’s dark past and not too distant violent history. GDP growth has helped create a small but growing middle class, and living standards for the average Cambodian have dramatically improved in the last two decades. The challenges of the country’s stock market underscore the fact that Cambodia still has many wrinkles to iron out, and growth in the bourse may be constrained by investors’ caution over corporate governance and transparency standards. However, in light of the upcoming ASEAN Economic Integration and the projected uptrend in the country’s economy, Cambodia will be an attractive investment destination for years to come and we at Asia Frontier Capital will certainly be tracking developments in the country closely. AFC Travel Report: CambodiaIn line with our process of being on the ground in the countries we invest in, AFC's Regional Investment Analyst, Scott Osheroff, travelled to Cambodia to explore the local market and keep his finger on the pulse in the region. My first foray into Cambodia in 2012 started in the dusty and chaotic border town of Poipet on the Thai-Cambodian border. I arrived by bus at dusk along with many other weary travelers after spending some time exploring Thailand travelling overland. Whilst border towns in Southeast Asia all have their own certain charm, in the shape of entrepreneurs looking to squeeze every possible penny out of passing tourists, I decided not to spend the night. Instead I looked to continue my journey to Siem Reap, home of the Angkor temples. This being long before the days of Uber, I had to spend some time haggling with some of the locals offering transport and arranged a taxi for the two hour ride before I could rest my head. Siem Reap is the must-see attraction in Cambodia, offering more historic temples and Asian architecture than almost anywhere I have been. The infrastructure and services available have been developing steadily over the past few years and you could literally spend weeks looking at dozens of jaw-droppingly massive religious sites - though you may end up with temple fatigue after a few days without the occasional break to sip cocktails by your hotel pool. Whilst the facilities are improving, the health and safety at some of these locations are not quite up to the standards of other tourist hotspots around the world. That being said, there are healthcare services available and of a much higher quality that you would expect in such a poor country. AFC’s Marketing Director, Stephen Friel, can attest to this, as he experienced them firsthand in 2011 when he inadvertently slipped on some dusty steps at Angkor Wat and had to have both of his newly broken arms mended at the Royal Angkor International Hospital. The grand total for x-rays, nursing care, medicine, UK-trained Thai doctors fixing two broken bones, and compound fractures in the wrist was roughly USD 1,000 which is a fraction of what you would pay in the West. With medical tourism in Asia becoming big business, perhaps Cambodia could participate in this industry at some stage in the future.

Leaving Siem Reap, I took a bus to the capital city, Phnom Penh, which – at the time – was a city of low density real estate and still had a few unpaved streets. The controlled chaos and infrastructure of other Southeast Asian cities, such as Bangkok and Ho Chi Minh, hadn’t yet arrived, making for a peaceful and somewhat rustic experience. Fast forward to May this year when I revisited Phnom Penh, and the above comparison no longer fits the mold of today’s Cambodia. The city is now bustling and congested, with cranes covering the horizon. With paved streets and expats becoming increasing mainstays, Phnom Penh is transitioning into a modern city in every aspect. The high average GDP growth of 7.7% from 1993 to 2013 has been fueled largely by real estate investment, efficiencies in agricultural production and the relocation of manufacturing, particularly in garments, from China to the greater Mekong Sub-region. This is leading to Cambodia playing a long game of “catch-up” with its neighbors. With over 650,000 Cambodians working in the garment industry, the overall number of locals involved in light and medium industrial manufacturing will continue to expand as Cambodia integrates with its ASEAN sister countries. This will also see logistics improve and high electricity costs subside. A natural home for labour intensive industries with Cambodia’s free market economy, the Kingdom is an ideal jurisdiction for such foreign investment. Riding the wave of this growth, Phnom Penh has been the beneficiary of investment from retail chains, thus providing new options for the growing middle and upper class who previously visited Bangkok, Ho Chi Minh, or Singapore for weekend shopping sprees. KFC having been the first entrant to the country in 2008, over the past several years there has been a surge of new multinationals moving in, including Burger King, Domino’s Pizza, Bon Chon Chicken, Yoshinoya, Krispy Kreme, Dairy Queen, Pizza Company, Coffee Bean & Tea Leaf, Ducati, Hugo Boss, and Rolls Royce, to name but a few.

Complementing these retail entrants is a construction boom which has led to a transformation of the downtown core and the periphery of the city. Entering a new phase in the real estate industry, Loan-to-Value ratios are increasing and more locals are taking on debt to buy property. Factor in the foreign investment in search of yield and every undeveloped land package seems to be under some stage of construction. On the periphery of the city, satellite towns being financed and constructed by Korean, Chinese, and Indonesian companies are sprouting from the rice paddies. Looking at all of the construction and uncertain demand, there is the potential for a correction in the market at some point, the signs of irrational exuberance remain however as new construction continues uninhibited by the potential saturation of the market.

As my visit came to an end, I left Cambodia on National Road No. 1 toward the Vietnamese border where passing through the town of Baveat I came across a sign perhaps foreshadowing the future of Cambodia—casinos. A gambling haven for Thais and Vietnamese who cannot gamble domestically, Cambodia has increasingly become a regional player in the gaming industry, attracting Chinese, Japanese, and Koreans in the process. Perhaps today the seeds are being laid for the new Macau of Southeast Asia? In Cambodia it seems anything is possible.

|

|||||||||||||||||||||||||||||||||||||||||||||

|

I hope you enjoyed reading our monthly newsletter. If you would like any information about our funds or markets please let me know. With kind regards, Thomas Hugger |

||||||||||||||||||||||||||||||||||||||||||||||

|

Asia Frontier Capital Limited |

||||||||||||||||||||||||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

||||||||||||||||||||||||||||||||||||||||||||||

GO TOP |

||||||||||||||||||||||||||||||||||||||||||||||

Source: VietCapital Securities

Source: VietCapital Securities Source: Bloomberg

Source: Bloomberg Source: World Bank

Source: World Bank