Asia Frontier Capital (AFC) - January 2015 Newsletter |

|||||||||||||||||||||||||

In this IssueAFC Asia AFC Vietnam Fund

|

"Empty pockets never held anyone back. Only In January 2015, the AFC Asia Frontier Fund returned –0.5% and the AFC Vietnam Fund returned +0.4%. The MSCI Frontier Markets Asia Index (+1.5%) had a positive month whilst the MSCI Frontier Markets Index (-4.1%) and MSCI World Index (-1.9%) lost ground. In Vietnam, there was significant market movement with the Ho Chi Minh - VN Index (+5.6%) and Hanoi VH Index (+3.3%) rallying strongly in January lead by a turnaround in sentiment towards the banking sector which saw a significant rally in index-heavy banking stocks. One of the major events this month was the sharp increase in the value of the Swiss Franc after the Swiss National Bank unexpectedly abandoned its policy of capping the Swiss Franc against the Euro. When the CHF started to move, Bloomberg lit up and the whole AFC office turned to watch the ticker as the currency spike started to cause turmoil in markets, the bankruptcy of some international brokerage firms, and losses of hundreds of millions for some large banking institutions. The European Union announced a few days later that there would be another round of quantitative easing (QE) which then pushed the Euro to multi-year lows. Large shifts in currency markets occur relatively often and this has once again highlighted the importance of diversification for investment portfolios to take into account currencies along with asset classes and geographic exposure. In this unprecedented age of low interest rates and global quantitative easing, investors should be wary of holding all portfolio assets in a single currency. This is of particular importance to investors if their personal or business income is also derived from the same currency, as your future earnings are, to a large degree, dependent upon the economic success of your home market. Looking back at the past year, there have certainly been some momentous moments for Asia Frontier Capital and, as it turned out, in 2014 the AFC Asia Frontier Fund (CHF share class) was in the top 20 performing hedge funds in the world and the AFC Vietnam Fund was also the highest-returning Vietnam fund in the world. We are very optimistic about the long term performance of our markets and would like to extend a thank you to all of our investors who have supported our boutique fund management company. AFC NewsAFC Wins Prestigious Fund Awards! With our 2014 fund performance in mind and the asset management awards season now at an end, we are very pleased to announce that AFC has picked up quite a few industry awards. Whilst we of course appreciate the recognition and accolades, we are already looking forward to producing better results in the coming year. The awards we have won are as follows: Top Performing Hedge Funds 2014 - Preqin

2014 Asia Asset Management Best of the Best Awards – The Journal of Investments & Pensions

2015 Hedge Fund Awards - Acquisition International, Sponsored by BarclayHedge

2014 International Fund Awards – Acquisition International

2015 International Fund Awards (to be announced March 2015) – Acquisition International

Innovation & Excellence Awards 2015 – Corporate Livewire

Hedge Fund Industry Awards 2015 - Finance Monthly

Alternative Investments Awards 2014 – Wealth and Finance International

New Director Appointed for AFC Umbrella Fund & AFC Umbrella Fund (non-US)

AFC in the Media

Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact our Marketing Director Stephen Friel at

AFC Asia Frontier Fund - Manager Comment

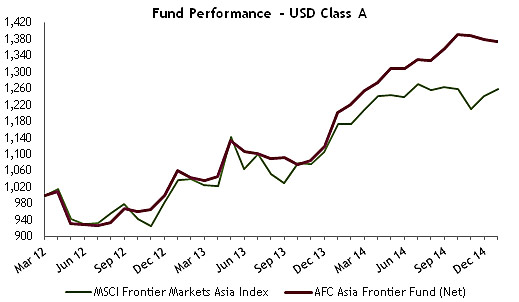

AFC Asia Frontier Fund (AAFF) USD A-shares returned –0.5% in January 2015, underperforming the MSCI Frontier Markets Asia Index (+1.5%), whilst outperforming the MSCI Frontier Index (-4.1%) and MSCI World Index (-1.9%). The bigger news in our markets this month was the Presidential election held on the 8th of January in Sri Lanka, with Maithripala Sirisena emerging as the winner. The win was a bit surprising, but in hindsight it should not have been given that Sirisena and other ministers defected from Mahinda Rajapaksa’s government in November 2014 to become part of the common opposition. This was a sign that not all seemed in order within the Rajapaksa government and reflected that the Presidential elections would see a close fight. There had been talk and rumors regarding the dictatorial nature of the Rajapaksa regime but at the same time the opposition was quite weak, which made Rajapaksa’s re-election more likely until the defections. Sirisena picked up lot of votes in the North and the East, two regions that were impacted during the end of the war in 2009 and which have historically not been strong vote banks for Mahinda Rajapaksa. On the political front, the new President has vowed to bring in changes such as abolishing the Executive Presidential System and introducing constitutional structure with an executive. Other political measures are linked to having a more balanced foreign policy, as the previous government skewed towards China with a lot of Chinese investment pouring into infrastructure projects. Sirisena is also expected to assuage some of the concerns of the minorities such as the Muslims and the Tamils since the minority-led parties supported his candidacy for President. On the economic front, the first victims of possible change were the infrastructure and tourism projects that were undertaken under the Rajapaksa government. Given the backlash against the prior government, it is not surprising to see the new government review mega projects. The Northern Expressway project and other infrastructure-related projects are being reviewed, whilst the Chinese port city in Colombo was put on hold until a few weeks ago but has now been given approval. At the same time, the casino projects of John Keells Holdings and the Crown group have been suspended. The recently passed interim budget was also very populist, with cuts in domestic fuel prices, increases in minimum support prices for certain agricultural products, waivers of loans to farmers, increases in salary levels for government employees and a one-time super tax of 25% on companies with earnings of more than LKR 2 billion. The economic moves so far paint a mixed picture, but historically the key opposition party in the recent elections, the United National Party, which supported Sirisena’s candidacy, has been pro-market and business friendly. These economically populist measures may also have been passed in order to gain a majority in the upcoming parliamentary elections which will be held in April 2015. Though the current political developments impacted market sentiment, there continues to a need for post-war infrastructure development and foreign investment given the current fiscal deficit and public debt levels in the country so it would not be surprising to see the government adopt more business friendly measures in the longer run. Amongst the fund’s Sri Lankan holdings, an infrastructure-related investment, which is the fund’s largest investment in Sri Lanka, corrected due to the negative sentiment surrounding infrastructure projects but other than that some of the larger consumer holdings did better than the overall Sri Lankan market. There were certain political developments in Bangladesh as well, in the form of blockades marking one year since the elections which were boycotted by the opposition. These opposition-supported blockades have continued throughout January and if they sustain, they could impact the export-driven industries such as the garment industry and the economy in general. Having said that, the blockades have occurred in the past and AFC’s strategy is to buy fundamentally good companies if there is any panic. Over the past few quarters, the fund’s investments in Bangladesh have been in consumer and utility companies and not so much in textile-related companies. Larger consumer holdings in Bangladesh bucked the overall market trend during the month. Besides the political developments in Sri Lanka and Bangladesh, there was no major negative news from the fund’s other key markets. Pakistan continued to rally on the back of a 100 basis point cut in key interest rates due to lower crude oil prices and inflation. We believe the fund holdings in Pakistan are well-positioned to take advantage of lower input prices as well as increases in consumer demand with the fund’s mix of textile, cement, and consumer-related holdings. Textile and cement holdings for the fund did well during the month as these companies benefited from lower input prices. Vietnam continues to show better GDP and industrial production growth numbers, with 4Q2014 GDP growth of 6.96% and industrial production growth of 10.1%. With a recovery in economic activity, the fund has made investments in certain cyclical companies such as an electrical cable company in which the fund initiated a positon this month. Our holdings in Vietnam underperformed the overall market, as banking stocks rallied and the fund has not invested in any banks given the historical issues with the sector. If the outlook on Vietnamese banks continues to change on a sustainable basis, the fund may look more closely at this sector. The best-performing indices within the AAFF universe in January were Pakistan (+7.2%), followed by Vietnam (+5.6%) and Laos (-0.9%). The poorest performing markets were Iraq (-33.2%) and Cambodia (-6.8%). The top-performing portfolio stocks were a Mongolian oil company (+52.9%), followed by a Vietnamese food producer (+31.1%), a Mongolian gold mining company (+28.6%) and an Iraqi food trading company (+20.5%). In January we added to existing positions in Bangladesh, Mongolia, Pakistan, Sri Lanka and Vietnam. We added two positions in Vietnam: a consumer good company and an electrical cable company. We also partially sold a small position in a Mongolian company. Overall, the underperformance of certain holdings in Sri Lanka led to a softer month but taking a longer term view, we think that the portfolio is well positioned to take advantage of the benefit of lower input prices across our key markets. As of 31st January 2015, the portfolio was invested in 118 shares, 1 closed-end fund (with 27.2% discount to NAV), 1 GDR (with 62.2% discount) and held 9.3% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.4%) and a pharmaceutical company in Pakistan (3.7%). The countries with the largest asset allocation include Vietnam (23.9%), Pakistan (20.4%) and Bangladesh (13.8%). The sectors with the largest allocation of assets are consumer goods (41.0%) and materials (13.9%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 13.77 x, the weighted average P/B ratio was 1.43 x and the dividend yield was 3.60%. AFC Vietnam Fund - Manager Comment

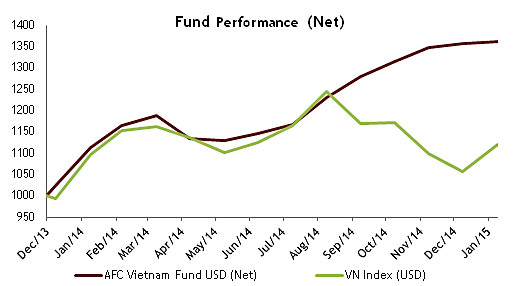

To read this month’s fund update in German please click here. In January 2015 the AFC Vietnam Fund returned +0.4%, bringing the net return since inception to 36.2%. After a four month correction, the first trading week of 2015 started with a nice recovery. After the past few surprisingly weak months, the turnaround that we had been expecting happened, and will hopefully soon expand to the broader market. The main beneficiaries of the recent rebound were the long-neglected banks, which reported positive earnings but also increased due to government reports about a few potential banking mergers this year. We too became more bullish on the banking sector recently and were close to investing, but decided not to get involved in the end because we see more potential in the medium term in other sectors, such as industrial, consumer, and selectively, property sectors. The second main reason for the index increase was the announcement of a share buyback program by PetroVietnam Gas JSC (GAS), a company which is part of the Ho Chi Minh Index with a (very high) weighting of 15%. We bought a small position in this stock, assuming a technical recovery, which is far from the allocated index weighting and more in line with other investors who typically hold a relatively small position relative to the index. We therefore see quite a diverse performance picture in January; the Ho Chi Minh Index led by GAS and banks rose by +5.6%, the Hanoi index, which also contains banks (but not GAS), increased by +3.1%. The indices have recovered well after a significant decline in recent months and many of our holdings which outperformed the market in recent months saw a consolidation in the past few weeks.

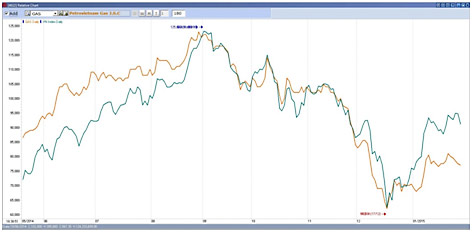

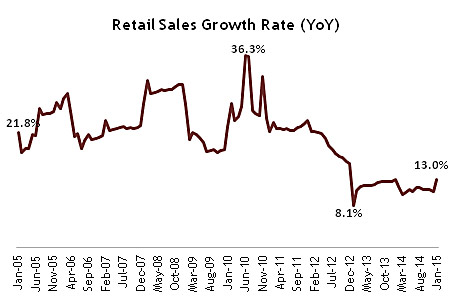

The volatility of the heavily index-weighted GAS (orange line) is only partially visible in the graph above versus the HCMC Index (green line). GAS had first doubled and then halved again, all in the same year. We are therefore glad to have invested free of any short-term index fluctuations and will continue to focus our attention on the long-term development of the Vietnamese economy and businesses. All the macroeconomic numbers released so far have enforced our long-term bullish view about Vietnam. We saw very strong retail sales numbers with a +13% growth rate year-on-year, mainly due to strengthening domestic activities. This month’s real growth pace is showing that domestic demand is strongly improving in real-term. Improving domestic consumption, combined with strong foreign direct investment, is certainly a powerful combination to drive a robust and sustainable recovery.

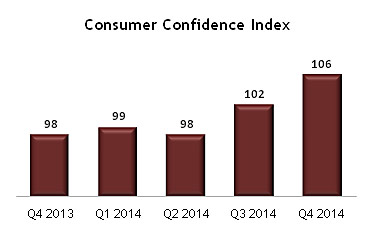

Another encouraging sign came from the Q4 2014 Consumer Confidence numbers, which also showed a very healthy increase to 106, +4 versus Q3 2014. It was interesting to note that 85 out of 100 Vietnamese people are changing their consumption habits, becoming more "intelligent" shoppers with at least 83% comparing similar products first before purchasing them, but at the same time becoming more quality conscious and being prepared to pay more for good products.

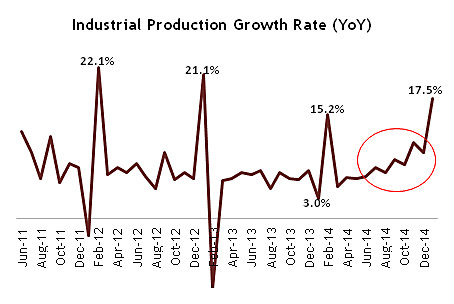

It is also worth noting that industrial production picked up in January to reach +17.5% year-on-year. In particular the manufacturing sector producing smart phones, PCs and other electronic devices surged impressively. January numbers are often quite strong as it is shortly before the Lunar New Year but the previous months also showed a nice acceleration.

At the same time, earnings reporting for 2014 has begun, which is important as it forms the backbone of our fundamental quantitative approach. Based on the results, we will decide if any portfolio adjustments are necessary. Presently, around 60% of our holdings have already reported their earnings, showing a mixed picture, with overall sales slightly above expectations, but revenues slightly below our estimates. According to current forecasts, 2014 profits of the companies in our portfolio should increase by approximately +10%, which is significantly higher than the overall market. It is still too early to do a reliable 2015 earnings forecast at this time, but a more detailed explanation of my views on economic forecasting can be found by clicking here (English) or here (German). Whilst there was an announcement of a 1% devaluation of the Vietnamese currency at the beginning of the year, by adjusting the trading band 1% up, we view this as a non-event given all the turmoil around the Swiss franc. The Vietnamese Dong is trading even slightly stronger versus the USD since the beginning of the year.

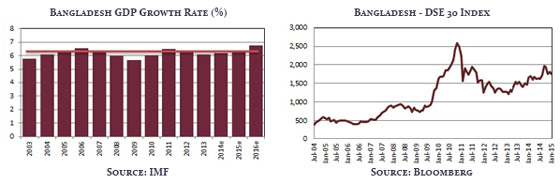

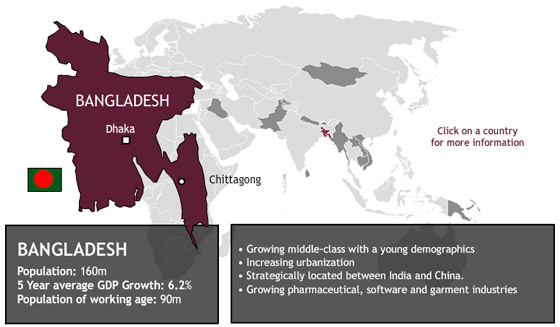

In January the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (5.2%) - a manufacturer of electrical and telecom equipment, Thuan An Wood Processing JSC (2.6%) – a household furniture manufacturer, FLC Group JSC (2.3%) – a real estate development company, SPM Corp (2.2%) – a pharmaceutical company and Gypsum and Cement JSC (2.2%) – a cement company. As of 31st January 2015 the portfolio was invested in 72 shares and held 3.6% in cash. The sectors with the largest allocation of assets were consumer goods (31.9%) and industrials (25.4%). The fund’s weighted average trailing P/E ratio was 7.56x, the weighted average P/B ratio was 1.10x and the average dividend yield was 5.87%. Please also note that because of the Vietnamese Tet holiday (Lunar New Year) there will be no mid-month report as the Vietnamese markets will only be open from February 24-27. AFC Country Snapshot: BangladeshWith over 160 million people, a young and cheap labor force and a strategic location between India and China - two of largest engines of global economic growth over the past decade - Bangladesh maintains strong prospects for extended economic growth. The extent of Bangladesh's growth will largely depend on its leaders' ability to improve economic and diplomatic ties among its neighbors. Completion of a highly anticipated Indo-Bangladeshi free-trade agreement will help spur Bangladesh's already surging garment, pharmaceutical, and software industries. Bangladesh has also begun to construct large infrastructure projects, such as electrical power plants, to address domestic and regional energy needs. In addition, with 50% of its workforce in the service sector, Bangladesh has the potential to become an offshore centre for outsourcing, which would help to further diversify its economy.

Stock Market: Bangladesh has two separate stock exchanges, the Dhaka Stock Exchange (DSE - established on 28th of April 1954) and the Chittagong Stock Exchange (CSE - established on 4th of November 1995). The DSE has a total of 274 listed companies with a market capitalization of USD 41.9 billion. The CSE hosts 246 companies and has a market capitalization of USD 33.7 billion as of February 2015.

Country snapshots for all of AFC's markets can be found on our website at www.asiafrontiercapital.com AFC Country Report: BangladeshAmidst all the talk of Asia’s high-potential emerging economies – particularly the media frenzy surrounding Myanmar in the aftermath of the country’s reforms – neighboring Bangladesh is perpetually ignored. This bustling country of 156 million people, the 8th largest in the world, seems to only be featured in global news media when something bad has happened. Whether it was the 2013 Rama Plaza factory building collapse, the Nov 2014 death sentence handed down to the leader of Jamaat-e-Islami, the country’s main religious party, or the violent protests and street blockades in January 2015 led by the opposition political party, the Bangladesh Nationalist Party (BNP), many outside observers’ perceptions are largely shaped by the depressing stream of events trickling out of Bangladesh. Despite the troubling headlines, Bangladesh does have some attractive investment characteristics. Its enormous population is famously hard-working, with established industries in textiles, manufacturing, pharmaceuticals, and chemicals, and also young – the median age in the country is 24 years old. As wages and labor costs have risen in China’s traditional manufacturing strongholds, factory owners have begun looking elsewhere to relocate their factories to cheaper destinations. Many factories have moved to Vietnam and Cambodia, but Bangladesh has also positioned itself as an attractive potential landing spot. In Laos, ongoing labor talks may raise the country’s minimum wage to USD 99-111/month as early as March 2015, while wages in Vietnam have been raised to reach USD 101-146/month depending on the region, and Thailand’s minimum wage is roughly USD 202/month. In Myanmar, a minimum wage law was only introduced in March 2013, and the Ministry of Labor has still not formally announced what the official minimum wage will be, although the current minimum wage for public sector employees is about USD 50/month. Despite the large increase in percentage terms in Bangladesh’s minimum wage in 2013, the country still remains very competitive and generally cheaper than its Southeast Asian rivals. In an industry like ready-made-garments (RMG), however, profit margins are razor thin and many Bangladeshi factory owners worry about the costs and delays that will occur due to the increasing regulation and oversight of the country’s biggest export industry. Significant progress has been made to improve the monitoring of the safety of the country’s factories, including the establishment of the Accord on Fire and Building Safety in Bangladesh, a 5-year legal agreement between international labor organizations, NGOs, and retailers in the textile industry signed in May 2013 to maintain minimum safety standards in the textile industry, and the Alliance for Bangladesh Worker Safety, a group of 26 major global retailers representing the majority of North American imports of Bangladeshi RMGs formed in 2013 that has launched the Bangladesh Worker Safety Initiative to improve safety conditions in the country’s factories. Local factory owners complain, however, that the massive overhaul and costs of safety compliance will threaten their competitiveness and endanger the overall industry that employs millions of Bangladeshis. Many high-volume factories in the country depend on sub-contracting to smaller firms to meet last minute orders, and the expensive and time-consuming process of inspections, structural upgrades, and fire / electrical equipment fixes is manageable for larger factories with wealthy owners but often too burdensome for smaller sub-contractors. Some in the industry have expressed concern that Bangladesh’s competitive advantage of being an “agile” production base may be jeopardized if producers cannot comply fully to the new safety standards. According to the IFC, the costs of mandatory upgrades will cost owners between USD 100,000 to 1 million. However, several US apparel manufacturing firms say they have made investments to help improve factory safety and some have guaranteed loans for the IFC and Bangladesh’s BRAC Bank to disburse to domestic factories. Despite improvements in safety and oversight in the textile industry, the economy has already encountered a substantial obstacle in 2015 with ongoing transport blockades organized by the opposition political party, the Bangladesh Nationalist Party (BNP), to protest the detention of their leader, Khaleda Zia. The ongoing blockade is costing Bangladesh’s transport sector alone USD 26 million per day due to delays and road blocks, and businesses are being pummeled by disruptions to vital components of their supply chain such as the import and distribution of raw materials and intermediate inputs. The transport blockade has increasingly become violent, with the death toll recently surpassing 50, more than 7,000 arrested, and widespread arson of commuter buses and cars. From the 5th to 23rd of January, an organization of businesses estimated that the economic loss caused by the protests and transport blockade was equivalent to 2.7% of the country’s GDP, contributing to delays in goods shipment and rising prices for products across the country. Bangladesh’s capital markets have slumped in response to the turmoil, with both the Dhaka and Chittagong stock exchanges falling significantly in the month of January. Sadly, such chaos and calamity has become relatively common in Bangladesh, but the general investment thesis of a growing consumer class in the world’s 8th largest country and an emerging low-cost manufacturing hub remains intact despite the many bumps in the road that we expect for the country. On a brighter note, from a macroeconomic standpoint, one global trend that should have a positive impact on Bangladesh is the fall in oil prices in recent months. Through the end of January 2015, oil had posted seven consecutive months of losses for the first time in history, with Brent falling 50% and sinking to a six-year low. Bangladesh is a net importer of oil, importing 5 million tonnes of fuel oil and 1.3 million tonnes of crude oil annually. For Bangladesh, lower oil prices should boost the country by stimulating domestic spending, raising purchasing power, contributing to sizeable foreign exchange savings, and reducing the cost of living through lower transport, fuel, and electricity costs. The economic stimulus effect will ultimately depend on the cost saving that is passed on to the consumer via lower petroleum prices in the domestic market, as the sole oil importer is the state-owned Bangladesh Petroleum Corporation (BPC). AFC Travel Report: BangladeshIn line with our process of being on the ground in the countries we invest in, AFC's CEO Thomas Hugger, recounts some of his experiences from his travels to Bangladesh in January 2015. Every time I arrive in Dhaka, I wonder how so many passengers could have fit on a Boeing 777… where were they all during the flight? Then I remember that Bangladesh is itself an anomaly to the general notion of population density. The country is roughly the size of Iowa with a population of about 156 million, which is more than 50x that of America’s small Midwestern state!

Fortunately we (I was traveling together with the new AFC Umbrella Fund Director Henry Looser) were able to leave through a side exit for “VIP” guests and thus avoided the hectic atmosphere at the regular exits where dozens of touts are waiting to haggle, hustle, and offer their transportation services into Dhaka.

We arrived on a Sunday, the first working day of the week in Bangladesh (87% of the population is Muslim). With a population of about 156 million, Bangladesh is the 8th most populous country in the world and the most densely-populated large country in the world (less populated city-states like Macau, Monaco, and Vatican City slightly edge out Bangladesh at the top of the rankings). Normally, Sunday is a very busy day on the street since schools and businesses restart after a two day weekend. On this visit, however, we were greeted by a general countrywide strike (hartal) which was started by the opposition party on 5th January 2015 exactly one year after the 2014 parliamentary election which the opposition party BNP had boycotted. The hartals in Bangladesh are unfortunately often quite violent with street blockades and attacks on property and public transport, including the burning of buses. The day we arrived, the countrywide death toll had already reached 25 lives. Despite the hartal, we experienced quite a lot of traffic on the highway from the airport to Gulshan (the new business district in Dhaka) due to a religious procession (Ijtema) which takes place in Tongi, not far from the airport, and is considered the third largest Muslim congregation in the world after the Arbaeen gathering in Kerbala, Iraq and the Hajj in Mecca, Saudi Arabia. We arrived safely at our hotel in Gulshan after passing various police checks. Entering our hotel was like entering the transit area of an airport with security checking and x-rays screening the luggage. The next day I was astonished to discover that when I tried to send out a Whatsapp message to my wife in Hong Kong, the service was shut down, together with other internet-based services (Tango, Viber, Line). Apparently, the government has blocked these instant messaging apps because the opposition BNP used these services to organize blockades.

Due to the ongoing hartals, many of the confirmed meetings with companies were unfortunately canceled due to security reasons (it was deemed to be unsafe to travel outside of Gulshan district due to ongoing road blockages). Nevertheless, we were able to visit several companies that we have invested in. The first meeting was with British American Tobacco Bangladesh, which is 73% owned by BAT, UK and 10% by Investment Corp Bangladesh. We met with the company secretary, who was very proud to inform us that his company is the country’s largest taxpayer. BAT’s products (Benson & Hedges) cover the low, medium, and premium ranges and the company has a 99% market share in the premium segment (Marlboro has 1%!) and 50% in the medium and low range. There is an even lower segment, the “bidis” (“beedi” in India or Sri Lanka) which are hand rolled sticks commonly smoked by the poor. The price for 25 bidis is around BDT 7 (USD 0.09) compared with BDT14 (USD 0.18) for 10 low segment cigarettes or BDT 80 (USD 1.03) for 10 premium cigarettes. Another company we were able to see was the Bangladeshi subsidiary of a multinational pharmaceutical company which is listed on the Dhaka Stock Exchange (“DSE”). 75% of the company’s products are produced in Chittagong, Bangladesh and the rest are imported. Surprisingly, the company executives complained about the preferential treatment of local companies in Bangladesh. As soon as one pharmaceutical product is produced in Bangladesh, foreign imports are not allowed anymore. We held additional company visits with one of the largest denim producers in Bangladesh, which has started to diversify vertically, and with the largest producer of acrylics (used for textiles, paint, fiberglass, and plastics) in Asia. Like many other Bangladeshi companies, both of these companies were suffering in January, despite record months in November and December, from the ongoing political unrest since it is too dangerous to transport finished goods by truck to the port in Chittagong for shipping. It is estimated that one day of hartal costs the entire economy USD 500 million, USD 45 million of which is solely garment exports!

In summary, my few days in Dhaka confirmed AFC’s overall view. Bangladesh has great long term potential, if and when the politics are right. I have been traveling to Bangladesh frequently since 1997 and on each trip, I notice how the country has progressed since my last visit: expanding and improving infrastructure, for example, and gradual wealth generation which is lifting people from absolute poverty to low income earners. This wealth generation has, unfortunately, still eluded many Bangladeshis, primarily due to political instability and general bureaucracy. When I look at other countries in the AFC universe like Cambodia or Myanmar, I see them overtaking Bangladesh soon. However, with the ongoing shift in low cost manufacturing, particularly in textiles and ready-made-garments (“RMG”), to cheaper destinations, Bangladesh is well-positioned to be a major beneficiary thanks to its existing RMG industry and infrastructure which will result in general economic growth benefitting many of the hard-working people of Bangladesh. |

||||||||||||||||||||||||

|

I hope you enjoyed reading our monthly newsletter. If you would like any information about our funds or markets please let me know. With Chinese New Year and Tet approaching I would like to wish you and your family all the best for the upcoming celebratory season. With kind regards, Thomas Hugger |

|||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||