Asia Frontier Capital (AFC) - April 2015 Newsletter |

|||||||||||||||||||||||||||||||

In this IssueAFC Asia AFC Vietnam Fund

|

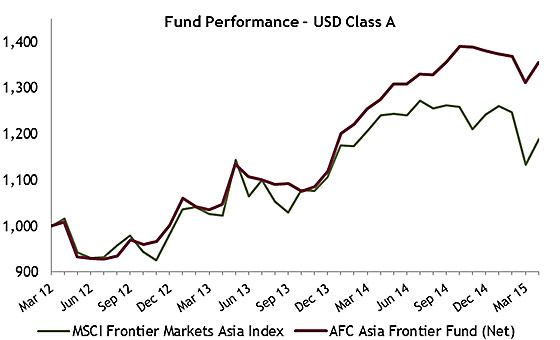

"What is coming is better than what has gone." In April 2015, the AFC Asia Frontier Fund returned +3.3% and the AFC Vietnam Fund returned +1.9%, bringing returns since inception to +35.5% and +39.9% respectively. The MSCI Frontier Asia Index (+4.8%) saw a significant bounce after dropping -9.1% in the previous month and the AFC Asia Frontier Fund has outperformed this index by 247 basis points this year. The MSCI Frontier Markets Index (+3.5%) as well as MSCI World Index (+2.2%) also ended the month up. Looking at Vietnam, the Ho Chi Minh VN Index (+2.0%) and Hanoi VH Index (+0.6%) both rallied on the back of a significant correction in March. So far in 2015 the Ho Chi Minh VN Index in USD, which is the closest comparable index, is lagging behind the AFC Vietnam Fund by 102 basis points. AFC’s funds have consistently outperformed their closest comparable indices, particularly during market drops, due to the focus on diversification and execution of their respective niche strategies. Throughout April there were a number of developments that impacted our markets. Sri Lanka pushed through landmark political reform with President Maithripala Sirisena passing a constitutional amendment reducing the executive power of the President. This move fulfilled a key election promise within the first 100 days in office and is a notable sign of political progress in the country. It is one of the few times in history where a national ruler has given up some executive power voluntarily. The oil price seems to also have begun to stabilize and has been marching slowly upwards since the beginning of the year which will hopefully steady the markets. Rapid swings in the price of oil can have a dramatic impact on the balance of payments as net importers will see a headwind whilst net exporters will see an increase in foreign reserves as they receive more currency for each barrel exported. Overall a steady, lower oil price benefits the frontier economies in our investment universe as oil is one of the key input goods for domestic production as well as export orientated industries. There have again been investment inflows this month and we would like to extend a warm welcome to all of our new investors. Asia Frontier Capital’s AUM is now on the cusp of USD 30 million, and we expect it to continue to grow even faster in conjunction with the upcoming launch of the AFC Iraq Fund later this month. Our total AUM has been growing exponentially since the MBO by our CEO – only 18 months ago AFC managed just USD 3.5 million in investments. AFC NewsAFC in the Media

AFC Collects Investors Choice Fund AwardsWe are very pleased to announce that AFC has won one of the most prestigious industry awards in Asia for the 2014 performance of both the AFC Asia Frontier Fund and AFC Vietnam Fund. The AFC Asia Frontier Fund won ‘Asia ex-Japan Fund of the Year 2014’ and the AFC Vietnam Fund won ‘ASEAN Fund of the Year 2014’ ranking them amongst the top funds that invest in the region. By not being benchmark constrained and being the most nimble in frontier markets we have managed to edge out the competition. HedgePo’s glitzy award evening was attended by the best performing fund managers in the world and the event was hosted by Bernie Lo of CNBC’s squawk box. Whilst accolades from our industry are always appreciated we have taken a moment to pat ourselves on the back for a job well done as it is an incredibly difficult feat to have two relatively tiny funds outperform the scores of analyst that support other fund management companies. We will continue to focus on doing what we do best to bring you more great returns rather than just pictures of us accepting awards. That being said here is one of the more entertaining photos from the night:

Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact our Marketing Director Stephen Friel at

AFC Iraq Fund Launch UpdateAsia Frontier Capital is pleased to announce the launch of the AFC Iraq Fund, which is open to initial subscription for investors as of May 2015. The AFC Iraq Fund will build on AFC’s core strengths and excellent track record investing in frontier markets as well as our history of launching innovative, successful funds. There is more information on the fund launch in last month’s newsletter which is available on our website (click here). To commemorate the fund’s launch, Ahmed Tabaqchali, CIO of the AFC Iraq Fund, will be a guest speaker in Dubai at the GCC Financial Markets Dialogue 2015 to discuss development and growth in the Middle East as well as frontier and emerging economies. You can find out more information on the event’s website (click here). Market Update – Oil Price and the Iraq Market

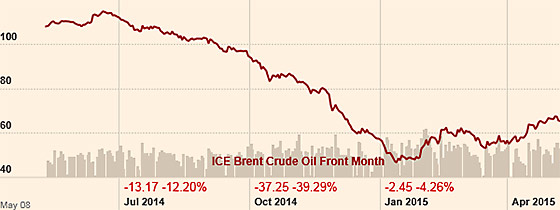

Last month’s newsletter highlighted that the oil price, having collapsed in H2/2014, seems to have made an important bottom in early 2015. Since then oil prices have continued to rally strongly, hitting new highs for the year and prompting talks of a full recovery in prices. The moves, however, are on pure shifts in sentiment which are shifting from fears of oversupply & demand weakness that drove prices down last year to hopes of demand recovery and an expectation of supply shrinkage. The basic reality, as far as supply and demand are concerned, is the same as it was a few months ago with the markets still oversupplied by about 1.5-2.0 million barrels per day. Interestingly prices are rallying while oil inventories in the US are at historic highs, plus production from Saudi Arabia and Iraq are at record highs more than offsetting any cut in Libyan production. Moreover, a number of shale oil producers have suggested that they will resume production if prices stabilize at somewhat higher prices. Looking down the road Iranian oil is also likely to come to world markets in 2016. A couple of months ago the same news would have sent oil prices plummeting amid predictions that prices were heading much lower still. So what has changed? The focus shifted from (1) the immediate weakness in global demand to expectation of recovery by early 2016 with signs that the Eurozone’s weakness are coming to an end and (2) shale oil production supply cuts will take effect in H2/15 and are showing signs of flat lining after months of increases. My belief is that underneath all the short term noise and changing short term trends is a major long-term shift in the supply-demand balance that will ultimately drive long term oil prices:

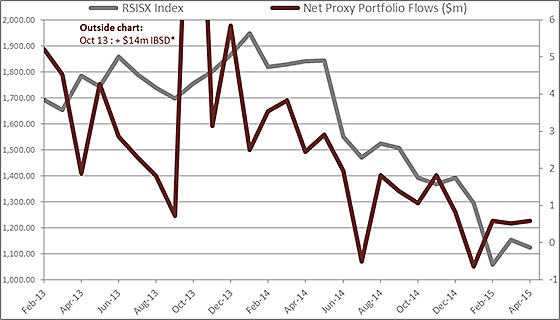

Net-net the above analysis drives our long-term investment thesis that demand increases will outstrip supply increases and thus increases the value of the oil reserves of Iraq, home to 9% of the world’s total proven reserves which are likely to be 15%, according to industry sources, as the country is explored further. As a result, in-spite of the current conflict and difficulties in Iraq, investments will pour in to develop these oil reserves which we expect will power and amplify its post-conflict recovery potential. These long term trends underline our investment thesis for Iraq and are a key driver behind our plans to launch the AFC Iraq Fund. The fund will have a strong emphasis on the long term investment horizon to truly capture and ultimately monetize this opportunity. The long term post-conflict opportunity in Iraq is clear and should bare rewards in the same manner that it has in post conflict economies in the past. That being said however, significant challenges lie ahead for Iraq and a patient approach will likely see the greatest upside for investors. The emphasis of the fund will be to participate in the long term story of Iraq without losing sight of short term issues. With a disciplined approach the focus will be to ride out periods of market noise, no matter how dramatic, whether returns are negative magnified by fear or positive magnified by greed. The timing of the fund’s launch coincides with negative investment sentiment that has contributed to price declines as can be seen from the chart below (RSISX Index developed by Rabee Securities versus a proxy for net portfolio flows). This chart shows the strong relationship between declining portfolio flows and the price index. Extreme negative sentiment will likely reverse with an accompanied increase in foreign inflows and could be triggered by stabilization in oil prices, success & containment of the ISIS threat, end of conflict, or an increase in stability in Iraq.

If you would like to find out more about investing in Iraq, please contact our Iraq team at AFC Asia Frontier Fund - Manager Comment

AFC Asia Frontier Fund (AAFF) USD A-shares returned +3.3% in April 2015, underperforming the MSCI Frontier Asia Index (+4.8%) and the MSCI Frontier Index (+3.5%) but outperforming the MSCI World Index (+2.2%). Whilst the MSCI Frontier Asia Index return was slightly higher than the AAFF this month it is important to note that last month the very same index dropped -9.1% whilst AAFF lost less than half that amount. The gains this month were led by Pakistan which saw the KSE-100 Index rally after the sell-off in the previous month. Given the positive macro triggers over the past few months, such as lower oil prices and interest rate cuts, it was not surprising to see the rally. An important event for Pakistan during the month was the visit of the Chinese President, Xi Jinping during which infrastructure and power related projects worth USD 46 billion were announced. A key part of this investment is the China-Pakistan Economic Corridor which will run from Gwadar (a port in Southwest Pakistan) to China’s Xinjiang region. If these investments come in over the next few years it could be a positive trigger for Pakistan’s economy especially its power deficit. The fund’s Pakistani cement holdings and a pharmaceutical company did well during the month on the back of good quarterly numbers. The lower costs, in the form of low input prices, was evident in the cement companies’ quarterly results and this low cost benefit should occur for the next two quarters, if not more. Sri Lanka also saw a rally after the dull market post the Presidential elections. With certain amendments promised before the elections being passed, the market gained some momentum. The infrastructure company the fund holds saw a recovery in price and this helped our performance in Sri Lanka. Vietnam also added to performance during the month as the fund’s small and mid-cap holdings did well. As mentioned in previous months’ newsletters, the fund’s Vietnam holdings are primarily in a mix of consumer and infrastructure-related companies across the small/midcap to large cap range (by frontier market standards). Bangladesh was a drag on performance given the ongoing political uncertainty in the country. The political blockades have died down, but the negative news was that the opposition did not participate in the local city corporation elections, which could lead to further tension amongst the two warring political parties, the incumbent Awami League headed by the current Prime Minister Sheikh Hasina and the opposition party, the BNP (Bangladesh Nationalist Party) headed by Khalida Zia. Mongolia had some positive news, with the Prime Minster announcing that the government is keen to solve the OT (Oyu Tolgoi) issue with Rio Tinto. If this occurs, then one can possibly expect more foreign direct investment coming into the country which should help the currency, which has stabilized over the past few months. The fund’s junior mining holdings focused on Mongolia added to performance during the month. The best performing indices within the AAFF universe in March were Pakistan (+11.6%), followed by Cambodia (+6.8%) and Sri Lanka (+5.3%). The poorest performing markets were Bangladesh (-10.7%) and Laos (-5.9%). The top-performing portfolio stocks were an oil producer from Myanmar (+51.7%), followed by a Mongolian mining company (+42.9%), a Vietnamese beverage company (+35.8%), and a Pakistani pharmaceutical company (+23.2%). In April, we partially sold three Vietnamese companies and two Mongolian companies. We added to existing positions in Laos, Mongolia, Myanmar, Pakistan, Sri Lanka, and Vietnam. As of 30th April 2015, the portfolio was invested in 118 shares and held 5.7% in cash. The two biggest stock positions are a pharmaceutical company in Bangladesh (4.3%) and a shoe retailer in Bangladesh (3.7%). The countries with the largest asset allocation include Vietnam (28.4%), Pakistan (19.5%), and Bangladesh (12.7%). The sectors with the largest allocation of assets are consumer goods (40.9%) and materials (16.0%). The weighted average trailing portfolio P/E ratio (only companies with profit) was 14.17x, the weighted average P/B ratio was 1.50x, and the dividend yield was 3.87%. AFC Vietnam Fund - Manager Comment

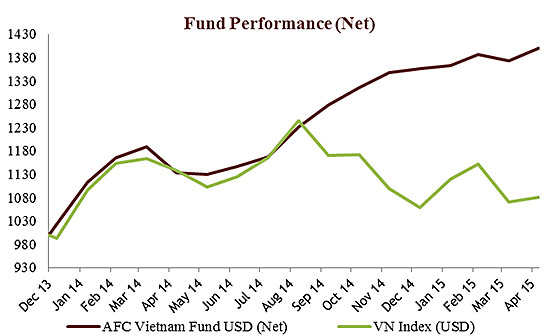

After a small setback last month, the AFC Vietnam Fund has now achieved a new all-time high. In April 2015, the AFC Vietnam Fund returned +1.9% keeping pace with the Ho Chi Minh VN Index (+2.0%) and Hanoi VH Index (+0.6%) which both recovered after a significant correction in March. Roughly 60% of our holdings have already reported their quarterly earnings so far in 2015. Though first quarter results are typically the least relevant for our in-house fundamental analysis, we have seen positive business trends for most of our companies. Important macroeconomic data has also been released recently. Foreign Direct Investment (FDI) is certainly worth mentioning as it climbed to an impressive USD 3.7 billion during the first 4 months of the year to reach nearly the same level as the first quarter of 2014. This has compared very favourably to other ASEAN nations including Thailand. Foreign investment also has a skill-based spill-over effect on the local labour market which will continue to have a positive impact on knowhow and technological adoption of the working population. This is one of the factors that will, in time, help to move the Vietnamese economy up the value chain. Looking at the currency market, the official rate is now 21,673 VND/USD, up 1% from 21,458. YTD, the Central Bank has devalued by 2%, in line with their previous guidance of 2% for 2015. Market participants had already priced in the rate adjustment, this had been in the talks for months now. In our view, the rate change came later than expected, indicating, to us at least, that the VND is stronger than market participants believe it should be.

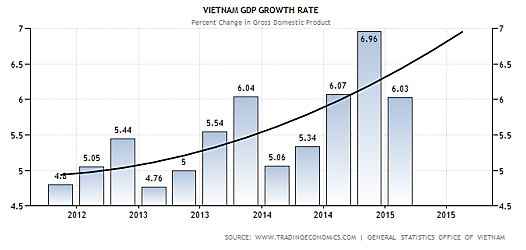

With a real GDP growth target for 2015 of more than +6% and an expected export-growth rate of around +10%, Vietnam’s economic outlook looks very bright for the coming years. This is not all that surprising given that Vietnam continues to have lower production costs than China and that there will likely be a sharp increase in trade after the signing of the new Trans-Pacific-Partnership agreement (TPP). The TPP will be very beneficial to Southeast Asia as a whole, but it is widely expected that Vietnam will be a key beneficiary within the region. The falling unemployment rate (currently at 4.2%) and a falling poverty rate (now under 10% of total population) will contribute to Vietnam attaining lower middle income country status. When walking through vibrant Ho Chi Minh City, one can see and feel the development of the country. All of these factors, in conjunction with its burgeoning young population (over 40% of the population has an age below 25 years), point to a prosperous future for Vietnam.

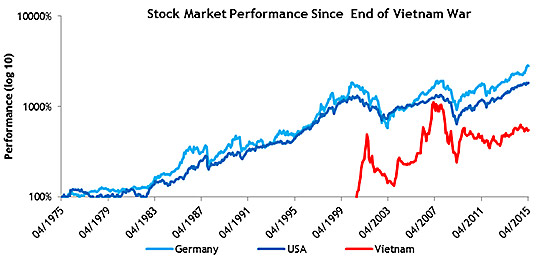

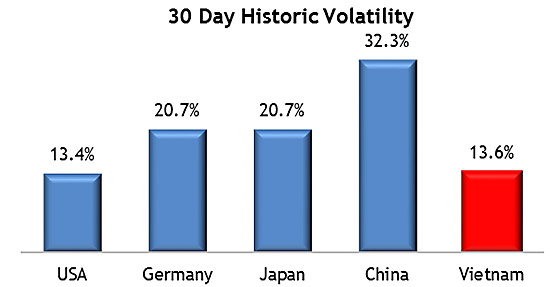

On the anniversary celebrating the end of the Vietnam War, we looked at stock performances in the USA and Europe since that date. We also compared the performance of the VN Index, starting in 2000, with the two other indices. Particularly interesting is the fact that since 2010 there is a healthy margin for the two well-known markets and Vietnam could have amazing potential for closing this gap. Lastly, we would like to comment on the widespread misconception in the investment community that frontier markets are very volatile and therefore have a higher risk. Looking at the numbers for Vietnam, stock market volatility is actually quite low compared to the US, Germany, Japan and China.

In April, the fund’s largest positions were: Sam Cuong Material Electrical and Telecom Corp (4.1%) - a manufacturer of electrical and telecom equipment, Gypsum and Cement JSC (1.9%) – a gypsum and cement company, Thuan An Wood Processing JSC (1.8%) – a household furniture manufacturer, Danang Housing Investment Development Company (1.8%) – a construction company, and Thanh Hoa Beer JSC (1.7%) – a beer producer. As of 30th April 2015 the portfolio was invested in 78 shares and held 17.3% in cash after a significant inflow of new funds at the end of the month. The sectors with the largest allocation of assets were consumer goods (29.8%) and industrials (21.8%). The fund’s weighted average trailing P/E ratio was 7.45x, the weighted average P/B ratio was 1.12x and the average dividend yield was 5.82%. AFC Country Report: Saudi ArabiaThis month’s country report profiles the Kingdom of Saudi Arabia (KSA). While Asia Frontier Capital does not currently invest in Saudi Arabia, we are always evaluating frontier markets that may possibly hold investment potential. For example, Nepal and Bhutan are both in our fund’s investment universe, although we cannot currently invest in either country. Iran is another intriguing potential market, with a relatively developed stock exchange, though any decision to invest in the country would depend on the repeal of US/EU sanctions. AFC’s Fund Manager, Thomas Hugger, travelled to Riyadh in early May to attend the Euromoney Conference on the news that Saudi Arabia is planning to open its stock market to foreign investors on 15 June 2015. The Kingdom of Saudi Arabia (KSA) is known for its incredible oil wealth and is home to the world’s second largest proven oil reserves, standing at almost 16% of the world’s total. KSA is also the world’s second largest oil producer and the world’s largest oil exporter. However, what remains relatively unknown is that it is the 15th largest economy in GDP PPP terms and the world’s 47th most populous country. KSA is home to Muslims’ most holy site of “Kaaba” in Mecca to which almost 2 million Muslims per year travel in pilgrimage (Hajj in Arabic) during the Hajj season. KSA is traditionalist and its conservatism is evident to foreigners from around the world who visit for travel or work, with both of these activities needing sponsorship. Saudi Arabia’s stock market, Tadawul, is the largest (USD 590 billion) and most diverse stock exchange in the Arab world. Given the stock exchange’s size and the fact that it has always been off-limits for direct investment from non-Saudi or non-GCC investors, it was big news among the emerging and frontier market investment community when the KSA’s Stock Market Regulator announced on 16th April that the Tadawul would officially allow foreign investors to begin trading the markets as of 15th June 2015. Currently, foreign investors can only gain exposure to Saudi Arabia though P-Notes, equity swaps, and a few ETFs. Access by institutional investors has been mostly through P-Notes, which received a boost when the KSA’s Capital Markets Authority (CMA) approved and regulated them, but as a group they never accounted for more than a tiny fraction of the market - probably 5% of total. The intention behind the decision to open the market is to attract an inflow of foreign capital to help diversify Saudi Arabia’s economy away from oil, boost job creation for the country’s relatively young and consumer-focused population, and hopefully usher in better corporate governance and financial reporting standards to help Saudi companies broaden their reach and further expand into new markets. Despite Saudi Arabia’s reputation of being an oil powerhouse, the Tadawul is very diverse in its composition, featuring large-cap companies in the petrochemicals, banking & financial services, and retail sectors, as well as many stocks listed in the insurance, telecoms, construction & building materials, and real estate sectors. Access to fresh capital via new foreign investment could help many Saudi companies become stronger regional players and penetrate nearby markets in the Gulf and the Middle East, and several fund managers have estimated that the opening could attract USD 50+ billion to the market in the next several years. Another topic of interest regarding the opening of KSA’s stock market is how it will impact any decision by MSCI to include the Tadawul in its Frontier or Emerging Market index. While MSCI has announced that it will launch a standalone index for Saudi Arabian stocks starting on 1st June, the decision of how Saudi Arabia will be classified will likely not be announced until 30th June 2016, instead of this year, as mentioned in Thomas’ travel report. Regional bourses Qatar and UAE were both promoted by MSCI in May 2014 from frontier to emerging market status. For AFC, the disappointing news regarding Saudi Arabia’s liberalization plan is that the country chose to adopt a Qualified Foreign Investor (QFI) scheme, similar to China, in which investor participation is limited to funds of a certain size (minimum AUM of USD 5 billion) and track record (minimum 5 years). While this specification likely will not impact large institutional managers, smaller, boutique investors like AFC are forced to remain on the sidelines until we meet the required size and track record requirements. Additionally, foreign ownership limits will mandate that foreign investors’ holdings cannot exceed 10% of the market’s value; with a limit of 5% for a single QFI’s holding in a particular stock and 20% for cumulative QFI holding of a stock. Regardless of the stipulations to be enforced regarding the opening of the Tadawul, Saudi Arabia appeals to many international investors because of the size and diversity of the stock market, strong demographics (young, consumer class with high income levels), and the potential for large Saudi companies to expand regionally. Saudi Arabia has been in the economic headlines a lot recently due to its decision to boost high levels of oil production over the past year to maintain global market share and to keep pace with rapidly rising US shale oil production, where these combined actions contributed to maintaining a global supply glut and accelerated the rapid fall in oil prices around the globe in the second half of 2014. Slumping oil prices have dramatically changed the economic outlook for many, leading to international oil majors scaling down capital projects, especially those that need high oil prices to be justified, and in the process laying off workers. Many oil producing countries like Russia, Nigeria, and Venezuela, to name a few, that depend heavily on oil export revenues have been harmed by the slump and are being forced to adjust their budgets. But Saudi’s national oil company Aramco has taken the long-term view and is investing heavily despite the low prices, boosting its production and number of drilling rigs and spending on new refining capacity in an attempt to potentially capture larger market share at a time when competitors’ financial woes are deepening. Saudi Arabia is now producing oil at the highest rate in 30 years, at 10.3 million barrels per day, and negotiated at least 20 drilling contracts for offshore rigs in the April alone. But despite steadily increasing oil production and a commitment to investing heavily to expand the sector, it has not all been smooth sailing for Saudi Arabia. The Kingdom, which has historically been a staunch ally of the United States, has nervously watched the unfolding of nuclear talks between America and Iran, which is seen as Saudi Arabia’s rival for power and influence in the Middle East. Both Sunni Saudi and Shia Iran are major economic powerhouses in the region, and are strong rivals and fierce competitors for leadership in the region and in the Islamic world at large. King Salman of Saudi Arabia, who was crowned as the King on 23rd January of this year, following the death of his half-brother King Abdullah, has made swift political changes both locally and regionally asserting a very strong regional role. His most recent major cabinet reshuffle shocked and rejuvenated the country’s leadership culture, naming his nephew, Interior Minister Prince Mohammed bin Nayef, as Crown Prince, and his son, Prince Mohammed bin Salman, as Deputy Crown Prince. To celebrate his coronation, King Salman announced a handout to Saudi citizens estimated at USD 32 billion, covering stipends for state employees, soldiers, students, and retirees, as well as numerous other grants. By far King Salman’s boldest decision has been to launch air strikes against the Houthi rebels in Yemen to counter Iran’s growing regional influence, a decision that has been relatively popular amongst Saudis who are wary of Tehran’s power ambitions. King Salman’s action-packed initial months as Saudi Arabia’s new King may have raised questions among foreign investors, though the underlying investment thesis for Saudi Arabia remains intact and the country has proven itself to be a mover and shaker on the global stage, with the power to steer global oil prices due to its mammoth share of the world’s oil reserves. Although it is disappointing for Asia Frontier Capital to not be able to participate in the opening of Saudi Arabia’s stock market, the country will surely be an intriguing investment destination for years to come and will be a good litmus test of how investor sentiment responds to the liberalization of a large and diversified stock market when it comes with so many rules and regulations. Other frontier markets, including some of the countries that AFC invests in, are also surely watching Saudi Arabia to see how MSCI will decide to classify it as these other countries hope to ascend to emerging market status. AFC Travel Report: Saudi ArabiaIn line with our process of being on the ground in the countries we invest in, AFC's CEO, Thomas Hugger, travelled to Saudi Arabia to explore the local market and keep his finger on the pulse of the region ahead of the launch of the AFC Iraq Fund. Organizing a visa to visit Saudi Arabia is not simple. Foreigners travelling to Saudi Arabia need either a visit visa with an invitation from a sponsor or, for a work visa, visitors need a valid work contract from an employer or sponsor. As I was travelling to Riyadh to attend the 10th Euromoney Saudi Arabia Conference, I received the visa sponsorship from Saudi Arabia’s Ministry of Finance. Despite having a sponsor’s invitation, the visa application procedure still involved lengthy waits at the Saudi Consulate in Hong Kong before being successfully approved, and the waiting continued upon arrival in Riyadh, as I stood for about two hours in the passport control queue at Riyadh International Airport. In the end, I reached my hotel around midnight local time (5am HK time), having had almost a 24 hour day immediately before the start of the conference. Not an ideal start for a business trip. The Euromoney Conference was very well attended, with 1,600 delegates. Most of the participants, however, were locals or from other GCC (Gulf Cooperation Council) countries like Kuwait and the United Arab Emirates (UAE). “Coincidentally”, the Capital Market Authority (CMA) of Saudi Arabia announced the day before the conference the conditions for the opening of its USD 590 billion equity market to foreign investors as of 15th June 2015. Unfortunately, the CMA did not change its first provisional release and will open its markets only to the “big boys”: fund management companies, insurance companies, and brokerages with at least USD 5 billion of assets under management and a minimum track record of 5 years. This is very disappointing for a small and young fund management company like Asia Frontier Capital Limited since we are at least 2 years away in order to be able to apply as a “qualified investor”. Additionally, foreigners are allowed to own an aggregate maximum 49% of a company and an aggregate total of 20% from “qualified investors” (the balance can only be owned by “strategic investors”). Each qualified investor is also allowed to own maximum 5% of any company. Lastly, foreigners in aggregate can only own at most 10% of the total market. Of course, the local conference attendees were extremely excited about the fact that foreigners will finally be allowed to officially invest, and were even more upbeat on the hope that Saudi Arabia will be part of the MSCI Emerging Market (EM) Index soon. The opening of the market and the possible inclusion in MSCI’s EM index have led many local investors and market participants to believe that the stock market will skyrocket on and after 15th June 2015 due to hopes for massive foreign money inflows. I personally have my doubts about these “assumptions/hopes”, as markets are discount mechanisms and events may not play out as hoped – as you will read later in this report. The conference began, after a reading of passages from the Holy Qur’an (Koran) with the opening speech by the Minister of Finance, followed by upbeat presentations from the Chairman of the Capital Market Authority and the CEO of the Saudi Stock Exchange (Tadawul), as well as other presentations from listed companies and fund managers. The most interesting session, however, was the last discussion of the first day in which the MSCI representative for the Middle East was in a panel with three CEOs of local fund management companies. The MSCI representative came under pressure due to his statement that Saudi Arabia will most likely not be included in the MSCI index until June 2017 at the earliest, which somehow surprised and obviously frustrated many local attendees in the audience. The reason for the extended timeframe is that MSCI announces the reshuffling of countries in its indexes every year by the 30th of June, but the actual implementation of the reshuffling does not occur until one year after the announcement, in order to provide the index followers with enough time to prepare and adjust, which makes absolute sense. The obvious frustration from the local fund managers stemmed from the fact that most likely this kind of announcement/decision will not be made until 30th June 2016, and not 2015, as had been expected by some in Saudi Arabia. The MSCI representative tried to explain in detail how the process at MSCI works: over the next 12 months, MSCI will contact thousands of investors from all over the world and collect feedback regarding the investors’ experiences, concerns, and accessibility of the country’s stock market before making any index classification decision. From my experience, the in-depth classification process that MSCI adheres to is very important. Many investors think that the reason why a country is included in an index is solely based on the size and development (GDP per capita) of the country’s economy. However, based on our research at AFC, one of the most important factors for MSCI to consider when deciding on a country’s potential inclusion in a certain index is the accessibility of the country’s stock market to foreign investors. It is for this reason that I think some observers may be disappointed in 2016 when MSCI announces its classification decision, as it is certainly possible that Saudi Arabia will be included in the MSCI Frontier Index and not in the MSCI Emerging Market Index. AFC’s theory here is that as of today, the two Chinese A-share stock markets (Shanghai and Shenzhen) are not included in the MSCI Emerging Market Index (China is part of the MSCI Emerging Market Index – but only H-shares, red chips, P-shares and B-shares – but not A-shares) since it has a very similar structure with a “qualified foreign institutional investor” (QFII) regime (however, the direct access has improved a little bit since the “Shanghai-Hong Kong stock connect” which started on 17th November 2014 and allows investors in Hong Kong to invest in Shanghai A-shares without a license). According to the China Securities Regulatory Commission’s website, as of November 2013, China has granted only 251 institutional investors with a QFII license after 10 years of existence. China’s minimum assets under management requirement for a fund manager (USD 500 million AUM) is also much lower than Saudi Arabia’s (USD 5 billion AUM). I cannot see Saudi Arabia having more than a handful of QFI investors by 30th June 2016, when MSCI will be able to make a decision regarding Saudi Arabia’s index inclusion, and this could possibly have the implication that Saudi Arabia will start “only” in the MSCI Frontier Index and will be below its smaller (in terms of market capitalization, population, and land size) neighbors like Qatar and UAE. For further reading, here are some articles regarding KSA’s stock market opening to foreign investors:

I also had the opportunity to travel around Riyadh (mainly in taxis due to the near non-existence of public transport), which is the capital of Saudi Arabia and with 7.3 million people the largest city in the country. Riyadh is situated on a large plateau in the middle of the country, as seen in the following picture which I took from the “Kingdom Center” located in Al-Olayya (Olaya), the commercial center of the city. Except for a few high-rise buildings in Olaya, almost all of the houses outside the commercial district seemed to be smaller 3 to 5 storey buildings.

However, a new financial center (left photo) is being built (in the far end of the right photo):

To me, Riyadh resembled an American city in many ways: grid-like, square-built new towns on either side of the main King Fahd Road highway which runs through the middle of Riyadh. The highway is chock-full of cars all day, primarily Japanese, Korean, and American cars. To my surprise, there were hardly any European cars on the road – according to locals I asked, European cars break down more often in the Saudi heat and car exporters to the GCC export cars with GCC specifications to deal with the demanding weather conditions. Most of the Mercedes that I did see were very old, though Bentley seems to be the preferred car of the KSA elite. At nearly every corner, one found US fast food chains like McDonalds, KFC, and Dunkin Donuts. Another similarity to the US is that when travelling into more remote areas, where huge enclosed compounds for the expatriates (including golf courses) are located, one can find lots of small shopping malls, reminiscent of American suburbia. Public transport in Riyadh is still relatively undeveloped. Only a few run-down mini buses driven by aggressive Pakistani or Bangladeshi drivers cruise through the city’s traffic jams. But there is good news for the myriad of foreign workers (primarily from Pakistan, India, Bangladesh, or the Philippines) who rely on public transit: a six-line metro system is in the process of being built and should open in 2019 (the picture below shows the Kingdom Centre with the construction site of the Riyadh Metro in front):

From a foreigner’s perspective, KSA is a conservative country when it comes to the participation and interaction of both sexes, especially outside family life. The streets are dominated by men, while malls and restaurants have female-only areas or family areas separate from those used by men. At the Euromoney conference, however, there were many female participants. AFC BournemouthOn a slightly different note, ever since I spent 20 fantastic weeks in the beautiful city of Bournemouth in the South of England back in summer 1983 to improve my English, I have been a supporter of its local football (for US readers: ‘soccer’) team, AFC Bournemouth (www.afcb.co.uk) or “The Cherries”. The team was founded in 1899 and never played in the first division and nearly went out of business due to financial problems twice during the past 20 years. But in the current 2014/2015 season, this tiny team achieved a miracle and managed to get promoted to the prestigious “English Premier League” (EPL) for the first time where it will play next season against the big teams like Chelsea, Liverpool and Manchester United. Asia Frontier Capital and The Cherries have some similarities: Obviously both use “AFC” in their name, and both are still small players in an extremely competitive environment – The Cherries in football and AFC in fund management – dominated by large and powerful global players. But like The Cherries proved, with passion, determination, dedication, good leadership, and hard work, it is still possible for small companies or clubs to play in the premier league of their fields and achieve outstanding performance. I would like to wish AFC Bournemouth all the best for a successful 2015/2016 season in the English Premier League and our readers much success in their investments, in which AFC hopefully can help add to the performance of your portfolio. |

||||||||||||||||||||||||||||||

|

I hope you enjoyed reading our monthly newsletter. If you would like any information about our funds or markets please let me know. With kind regards, Thomas Hugger |

|||||||||||||||||||||||||||||||

|

Asia Frontier Capital Limited |

|||||||||||||||||||||||||||||||

Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund, AFC Iraq Fund, AFC Iraq Fund (non-US) or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||||||||||||||||||||||||||||

GO TOP |

|||||||||||||||||||||||||||||||