Asia Frontier Capital (AFC) - September 2013 Newsletter

In this IssueSkybridge Alternatives The Generalised Quick Links |

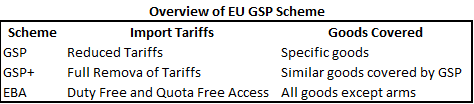

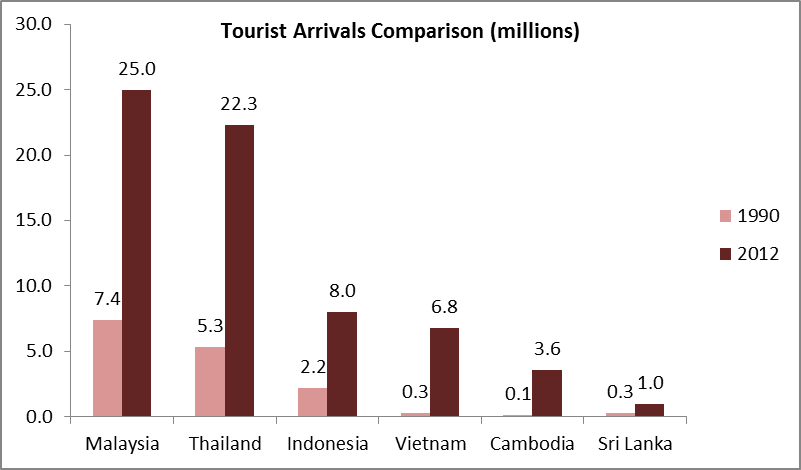

Welcome to this month's news from the Asian frontier. This month has seen more travel, research, and investor interest in AFC than ever before. Highlights from this month include our investment road show to Singapore, attendance at the Skybridge Alternatives conference, participation in a Sri Lankan investment summit in Hong Kong, and a research report from AFC's team being published in Marc Faber's highly-regarded Gloom, Boom & Doom report. Looking ahead at this month, we will be providing insight from changes to the Generalised Scheme of Preferences (GSP) which will have an impact on tariff levels facing frontier markets starting in January 2014. We would also like to take this opportunity to extend a personal welcome to all of our new clients who came on board in September. Our fund administrators plan to be even busier this month as our investor pipeline fills up from AFC's ongoing roadshow. We encourage potential new subscribers to be in touch with documentation queries as early as possible ahead of this month's cut-off date on the 25th of October. Upcoming AFC Investment RoadshowsAs announced in last month's newsletter, AFC's CEO and Fund Manager, Thomas Hugger, is visiting London and Switzerland in October to meet with investors as part of our international investment roadshow. Although the schedule is already quite full, potential investors are encouraged to be in touch with Stephen Friel at London 14th to 18th of October AFC Media Coverage and the Gloom, Boom and Doom ReportIn the past month, AFC has been featured in articles in both Forbes and Asian Investor. Our fund manager also hit the airwaves of Malaysia with a prime time interview on BFM89.9 - The Business Station. Additionally, AFC's report "The Case for Asia's Frontier Markets" was published in the October issue of Marc Faber's renowned Gloom, Boom & Doom Report. AFC would also like to announce its new partnership with 'Emerging Frontiers', an online media resource that provides investment news and analysis from emerging and frontier markets. If you have an interest in keeping up to date with news from frontier markets around the globe, consider subscribing to their weekly news digest which is available on their website. Fund PerformanceThis month saw some interesting action in the markets which reflected shifts in the overarching macroeconomic factors that are driving changes to the global economy. A recurring theme in 2013 has been ongoing uncertainty in Europe as well as the US as world leaders try to work out how to unwind, taper and adjust their fiscal policies in a way that balances short term pain with potential long run consequences of inaction. One of the key debates that has been ongoing is whether the driver of growth in the coming decades will shift to the emerging world as the growing middle class in these countries expands their economic voice. The aggregated views of the SALT presenters, panel participants and presenters indicated that they saw a continuation of Asia's rise which may be slowed but not stopped by instability in other regions. The performance of the AFC Asia Frontier Fund and related indexes reflected some of these changes as there was a divergence of performance in Asian frontier markets against the rest. In September 2013 the AFC Asia Frontier Fund (AAFF) USD A-shares gained 0.1% and outperformed the MSCI Frontier Asia Index (-2.3%) but underperformed both the MSCI Frontier Markets Index (+3.2%) and the MSCI World Index USD (+4.8%). One of the major drivers of the diverging performance of these indices was a shift in expectations on the rate of growth in Asia as well as weakness in Pakistan, which makes up 42% of the MSCI Frontier Asia Index. The selloff was particularly driven by foreign investors who pulled money out of equities to sit in cash or search for value elsewhere. AAFF again avoided losses as markets fell due to the strategic construction of the portfolio which primarily holds more stable consumer stocks as well as small and midcaps that are overlooked by larger funds and not included in the indexes. This also reflects the opportunities that are available when investing in actively managed funds rather than those who have an emphasis on tracking indices. In September, only two country indices in the AAFF universe were up: Vietnam (+4.2%) and Mongolia (+1.1%). Vietnam saw strength as selling pressure from foreign investors, particularly ETFs, subsided. Mongolia ticked higher as market sentiment turned positive as the standoff with Rio Tinto and Oyu Tolgoi may now have an end in sight. All other indices in the AAFF universe were down last month, with the worst performers being Cambodia (-21.3%), Bangladesh (-6.5%), and Iraq (-3.9%). The Cambodia Stock Exchange still lists only one stock, Phnom Penh Water Supply Authority (PPWSA), which suffered from worsening investor sentiment due to the political situation after the July elections were claimed by the opposition party to be irregular. The top performing stocks were a Mongolian hardware store (+52.7%), a Mongolian fur and leather processor (+41.2%), and a Vietnamese telecommunication equipment manufacturer (+24.1%). During the reporting month AAFF increased its holdings in various stocks in Bangladesh, Laos, Mongolia, and Vietnam. As of 30th September 2013, the portfolio was invested in 108 shares, 2 closed-end funds (with 35.8% and 25.7% discount to NAV), 1 GDR (with 55.1% discount) and held 7.3% in cash. The two biggest stock positions are a power producer from Laos (4.3%) and a pharmaceutical company from Bangladesh (4.3%). The countries with the largest asset allocation are Vietnam (20.9%), Bangladesh (16.9%), and Pakistan (12.3%) The sectors with the largest allocation of assets are consumer goods (45.0%), financials (10.7%) and materials (10.5%). The fund's weighted average Price/Earnings ratio was 12.81x, the weighted Price/Book ratio was 2.83x and the portfolio dividend yield was 4.69%. For further information please download our fund information from our website here. Skybridge Alternatives Conference (SALT)After heading to Singapore in September to meet with investors, the AFC marketing team attended this year's Skybridge Alternatives Conference (SALT). Known internationally for its cavalcade of high profile speakers and world renowned investors, SALT remains one of the premier events bringing together fund managers and global investors looking for access to new strategies. Notable speakers at the event included Timothy Geithner (Former US Secretary of the Treasury), John Lipsky (Former Managing Director of the IMF), Jean-Claud Trichet (Former President of the ECB) and Nassim Taleb (Author of The Black Swan), amongst others. One of the most interesting presentations was by Dr. Marc Faber (Writer of the Gloom, Boom & Doom Report), who opened the conference by sharing his views on the future of the US economy and upcoming investment opportunities in Asia. It should be raised at this point, in the interest of full disclosure, that our team may have a small bias towards the topic of this presenter given that he is one of AFC's shareholders. Dr. Faber's presentation proved to be a talking point at the conference, sparking ongoing debate amongst the event's participants. The event's attendees included representatives from some of the world's largest pension funds, funds of funds, endowments, and family offices. Given the niche investment approach of the AFC Asia Frontier Fund, it is always interesting to see how new investors from different parts of the world respond to AFC's investment strategy. The vast majority of 'Western' investors we meet have well-established portfolios but are missing exposure to Asia's frontier markets, despite holding a significant allocation to emerging markets such as China, India, and Indonesia. It was evident that many misconceptions exist, as most potential investors perceive the growth drivers and correlations of Asia's frontier markets to be the same as it is for emerging markets. Despite this, there was a tremendous amount of interest in looking at financial assets located outside of the US and Europe due to the ongoing economic uncertainty and longer term structural issues that remain unresolved. The difference between investors based in Asia and investors living outside of the region was striking. When talking to other fund managers, there was a general awareness of the economic shifts impacting frontier markets, as many of their own portfolios contained companies that had moved their operational base to follow lower wages and costs of production. Excitement about opportunities in Asian frontier markets was noticeably higher from those who have lived through the rapid transformation of Asia - from economic backwaters to regional powerhouses - within their lifetime. There were many comparisons on the similarities between the countries in AFC's universe and the stages that China, Thailand, and India were at two decades ago. Investors representing family businesses from across the greater Asian region were particularly quick to pick up on the depth of AFC's thesis given their hands-on experience with intra-Asian and international trends that are bolstering the future prospects for the frontier. There was a positive outlook regarding the development of the region's stock markets and the growth of IPOs and moving forward the number of listed investment opportunities in frontier Asia will continue to rise. The Generalised Scheme of Preferences (GSP) and its Impact on the FrontierAs the size of the AFC Asia Frontier Fund continues to grow, the analytical team aims to provide insight on upcoming developments impacting our key markets. One such development is the change in the way in which more developed markets will trade with those further down the economic development list moving forward. This month's research piece will cover the impact of changes to tariffs under the Generalised Scheme of Preferences (GSP) and how they may impact AFC's investment universe. The GSP is a scheme under the United Nations Conference for Trade and Development (UNCTAD) through which countries give selected products originating from developing and least developed countries preferential treatment through tariff cuts. There are currently 13 national GSP schemes notified under the UNCTAD. These are GSP schemes of Australia, Belarus, Canada, Estonia, the EU, Japan, New Zealand, Norway, Russia, Switzerland, Turkey, and the USA. In this month's newsletter, we focus on the EU GSP scheme, which is expected to change beginning January 1, 2014. The EU's GSP program helps developing and least developed countries by making it easier for them to export their products to the EU through reduced tariffs for specific goods entering the EU market. This helps developing countries grow their export revenue and supports job creation and economic growth in the exporting nation. The EU has decided to update its current GSP scheme to further benefit the countries that need such schemes the most. At present, some countries in the GSP scheme have free trade agreements with the EU, are middle/high income countries, or are competitive developing nations and should no longer be applicable for the GSP scheme due to their improved integration into the global economy. The new GSP scheme will focus on countries that need such benefits the most, resulting in the number of GSP beneficiary countries decreasing to 90 from 177. Within the EU GSP framework, there is also the GSP+ and EBA (Everything But Arms) framework. GSP+ Scheme: The EU GSP+ scheme provides full removal of tariffs for imports into the EU and has been designed to benefit countries that are economically vulnerable. These are countries that are: Further, in order to qualify for the GSP+ scheme, countries must meet criterion such as implementing human and labour rights as well as good governance measures. These countries also must agree to be monitored regarding their implementation of the required measures. From the Asian frontier markets that we cover, Iraq, Mongolia, Pakistan, and Sri Lanka are all eligible to apply for GSP+ status. EBA (Everything But Arms): This scheme is designed specifically for Least Developed Countries (LDCs) and provides such countries with duty free and quota free access to the EU for all goods except arms and armaments. From the Asian frontier markets that we cover, the countries that are eligible to benefit from the EBA scheme are Bangladesh, Bhutan, Cambodia, Lao PDR, Myanmar, and Nepal. Country Snapshot: Sri LankaEvery month we highlight economic developments in one country within the AFC Universe and this month we also add our comments about the Sri Lanka investor conference which we attended in Hong Kong. In line with our process of meeting companies and their management teams as often as possible the investor conference gave us the opportunity to meet 11 companies face to face and we also got an update on Sri Lanka's economy. It was a good mix of companies that represented well-established names from the banking, consumer, hospitality, and industrial sectors. The mood amongst the management was optimistic as they now have the opportunity to embark on new growth opportunities after the end of the civil war in 2009. For more than two decades the economy was held back due to the conflict, but the last few years have seen the country resurge to capture its potential. This newfound optimism was reflected in our talks with various management teams that are enthusiastic about growing their businesses. Furthermore, the government is playing an important role in helping these businesses grow by contributing to infrastructure development as well as supporting revenue-earning industries like tourism. Sri Lanka has always been known for its holiday appeal, but its tourism industry has only just begun to experience rapid growth since the end of the country's civil war in 2009. Asian tourist destinations in general have boomed over the past two decades, but Sri Lanka was held back due to the war. Vietnam, for instance, received merely 300,000 tourists in 1990, but by 2012, this number had jumped to 6.8 million, an increase of 22 times. On the other hand, Sri Lanka had a similar number of tourist arrivals in 1990 but only reached 1 million arrivals last year. This reflects the damage that the conflict created for an important industry but also highlights the potential that the country holds for tourism.

The end of the war has helped tourism arrivals grow from roughly 450,000 in 2009 to an estimated 1.25 million in 2013, nearly a threefold increase. This surge in tourism has led to new developments as the hotel & leisure industry underinvested during the war, leading to a lack of capacity in terms of hotel rooms. For example in the country's capital, Colombo, the organised hotel industry has about 3,200 rooms, compared to 64,000 rooms in Bangkok. In light of the increasing tourist numbers, there are plans to develop Colombo/Sri Lanka as a gaming hub in South Asia. Currently, most South Asian tourists, particularly those from India, travel to Macau for their gaming related tourist activities, as casinos are not allowed to operate in India. With India already contributing to the largest number of tourist arrivals to Sri Lanka, developing Colombo as a gaming centre could possibly attract these tourists, as Colombo is closer and cheaper than heading to Macau. Flight times between most major Indian cities and Colombo is between 1.5-3.5 hours, compared to a 6 hour flight to Hong Kong/Macau.

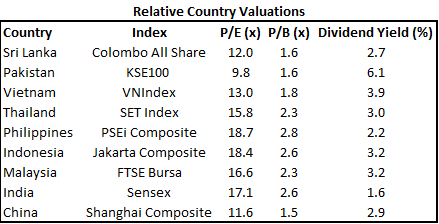

Another industry that has seen post-war growth prospects is the construction and construction-related industry due to the government's emphasis on post-war infrastructure development. The eastern and northern parts of Sri Lanka were significantly impacted by the war and this has left a lot of room for rebuilding and developing these regions further. The construction industry grew by 14% and 22% in 2011 and 2012 respectively and has grown by 18% in the first half of 2013. Construction-related stocks are poised to benefit from this focus on infrastructure and this is reflected in the financials of some of the companies that have seen revenue and earnings grow significantly over the past 3 years. This focus on redevelopment by the government has come at a cost, however, as the fiscal deficit was 6.4% of GDP in 2012. Still, this is lower than the 10% it touched in 2009 at the peak of the war. The Sri Lankan stock market, represented by the Colombo All Share Index, trades at a trailing 12 month P/E of 12.0x and P/B of 1.6x. Post-war Sri Lanka offers opportunities in sectors such as tourism, consumer, and infrastructure and we look at companies that offer attractive or reasonable valuations relative to their growth prospects. Some of the larger names on the index are diversified holding companies with interests in multiple industries and thus we also look at companies which could see value being unlocked from their balance sheets in the future.

Sri Lanka is also making strides to further develop its capital markets. In an effort to incentivise local companies to list on the CSE, the bourse is holding a forum this month targeting unlisted companies to highlight the benefits of publicly listing their shares and corporate debt on the Colombo Exchange. The bourse is spearheading a number of events to increase awareness about the strategic and financial benefits to private sector businesses of listing their equity and debt on the CSE. Sri Lanka has also been in discussion with Hong Kong Exchanges and Clearing Limited (HKEx), as it plans to demutualise its Colombo Stock Exchange (CSE) in 2014. The demutualisation would convert Sri Lanka's exchange from a non-profit, member-owned organisation to a for-profit, shareholder owned corporate entity. Sri Lanka is looking at the model of HKEx, which listed in Hong Kong in 2000 and is now one of the world's largest exchange owners based on the market capitalisation of its shares. In addition to planned legislative and regulatory improvements, the CSE has also been aggressively courting foreign investors, sponsoring a conference in Hong Kong which we attended, as well as roadshows earlier this year in Dubai and Mumbai. Foreign investors now account for 38% of market turnover in Sri Lanka, more than triple the amount from 2011. One selling point for Sri Lanka has been the stability of the Sri Lankan rupee, particularly in comparison with the currency woes India has faced. The Governor of the Central Bank of Sri Lanka, Ajith Nivard Cabraal, has highlighted how the country has kept inflation in single digits and interest rates in check, leading to far less volatility in the Sri Lankan rupee compared to other Asian countries. While India's growth has slowed, Sri Lanka's GDP is forecasted to grow by 6.3% this year and 6.8% in 2014. Please do not reply to this email address. This is a pure outgoing mailbox and your replies will not be read. If you have any questions or comments, please write an email to Kind Regards, Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|

|

GO TOP |

Sri Lanka has a lot of to offer to the adventurous traveller

Sri Lanka has a lot of to offer to the adventurous traveller