Asia Frontier Capital (AFC) - November 2013 Newsletter

In this IssueMongolia Event Attendance Note Quick Links |

"I'd rather buy something that is relatively depressed than something that is relatively high." In this month's edition we discuss the recently announced AFC Vietnam Fund, which launched on 11th December 2013. You can also read about some of the factors impacting Mongolia in this month's Investment Summit Notes and Country Report after the AFC team attended the Mongolia Investment Summit and Mongolia Business Forum, which hosted the President of Mongolia. We also provide further explanation about how to invest in AFC fund offerings. AFC would also like to announce that we have become a contributor to Seeking Alpha where we will be providing insights on frontier markets in Asia. Be sure to follow us on Seeking Alpha, LinkedIn and Facebook by clicking on the links on the right hand side of this email.

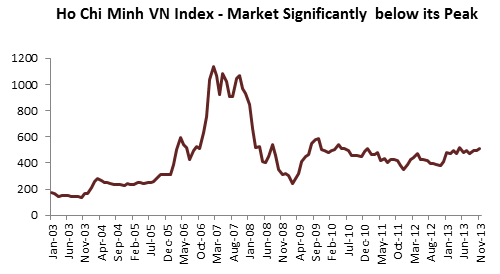

AFC Vietnam FundIt is easy to visualize an analogy between the quote from Marc Faber above and the Vietnamese stock market displayed in the graph. The stock market in Vietnam saw heady days in 2007-2008 but has not seen major action since then and this is why we believe it is a good time to enter this market given its attractive valuations, demographics and further integration with world trade. Vietnam has been the largest individual country holding in the AFC Asia Frontier Fund for some time and AFC is very excited to add this new strategy to our fund offering. The AFC Vietnam Fund is managed under the executive leadership team of Thomas Hugger, Andreas Karall, and Andreas Vogelsanger. This team has more than 75 years of investment experience as well as extensive experience working in Asia, having held senior positions in Cambodia, Hong Kong, Singapore, Sri Lanka, and Thailand. Asia Frontier Capital (Vietnam) Limited is the Cayman Islands-based investment manager of "AFC Vietnam Fund". The fund aims to achieve capital appreciation for investors over the next 5-7 years by capturing value in growth companies, especially in the small-to-medium size company segment. The target companies in this market segment are currently undervalued relative to the large caps and blue chips listed in Vietnam. The VH Index (Hanoi) and VN Index (Ho Chi Minh) have continued to exhibit low correlations with the MSCI World Index, at 0.31 and 0.40 respectively based on 10 year monthly returns. From a macroeconomic perspective, Vietnam has very compelling growth prospects alongside an attractively valued market that has significant room to grow. Competitive labour costs and improvements in human capital, combined with improving overall economic and trade environments, present a strong case for market development. Vietnam has had a stable currency and increasing foreign reserves over the past two years with GDP growth rates being supported by fiscal and monetary policy. The local market has seen several years of consolidation since dropping from its highs in 2007-2008 and improving fundamentals will continue to support domestic markets. Reaching previous highs in coming stock market cycles would mean a potential increase of several hundred percent in local terms. If you would like to know more about the AFC Vietnam Fund, please contact How to Invest in AFC Asia Frontier Fund and AFC Vietnam FundRecently some investors (primarily from Switzerland) have been trying to invest through their bank into AFC Asia Frontier Fund or AFC Vietnam Fund. However, some of the banks declined the order for unknown reasons. In such a case, you should inform your bank that CITCO Global Securities Services Ireland (www.citco.com), Societe Generale Securities Services Luxembourg (www.securities-services.societegenerale.com) or SIX Securities Services, Olten (www.six-securities-services.com) provide banks fund execution services. All three fund service providers have already invested in the AFC Asia Frontier Fund on behalf of their clients. Whilst there are many ways to gain access to our fund, we generally advise potential investors to invest directly into the AFC Asia Frontier Fund or AFC Vietnam Fund. The advantages compared to investing through a bank include:

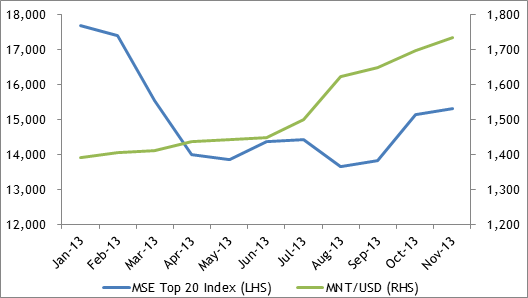

US-investors can invest in AFC Asia Frontier Fund through a "self directed IRA". Millennium Trust Company (www.mtrustcompany.com) is offering this service and clients have already invested in AFC Asia Frontier Fund through Millennium Trust. Please contact Stephen Friel Fund Manager CommentWe have frequently been told that it can be somewhat daunting to put your money to work in markets where you have not spent time on the ground. Asian markets have a unique economic, social and political history which may seem even more daunting to navigate if you have not spent decades studying the drivers of the Asian region. The concept of investing in the frontier is relatively simple, however, if it is linked to your view of human behavior, incentives, and how you see people making logical decisions driving trends in the future. With the significant consumer focus of AFC's investment strategy, we own the companies that will manufacture, distribute, and sell the food and consumer products that will be in high demand from Frontier Asia's growing consumer class. There are 572 million people in our country universe with an average age of around 30 years old, all working hard for a better future. This means that there are hundreds of millions of children, teenagers and parents building towards higher standards of living looking to spend more on both staple and discretionary goods. High GDP growth rates and increasing productivity will mean more wealth for those living in frontier countries, which boost the capacity to save, invest, and consume. Looking at the portfolio, AFC Asia Frontier Fund (AAFF) USD A-shares gained +0.9% in November 2013, outperforming the MSCI Frontier Markets Asia Index which lost -0.2%. AAFF continues to underweight Pakistan relative to the MSCI Frontier Markets Asia Index due to ongoing macroeconomic issues and the country's low levels of foreign reserves. The focus of AAFF is not to follow the MSCI Index but rather to avoid allocation to markets that have potential for significant currency depreciation or have the potential to face serious macro headwinds. The strategy then captures returns in stocks that present the greatest value and growth opportunities across countries with a focus on consumer facing businesses, while reducing the downside potential of significant market corrections. In November, the best performing indexes within the AAFF universe were Cambodia (+8.0%), Pakistan (+6.7%) and Bangladesh (+6.6%). Sri Lanka lost some ground (-3.0%) and Laos was also down (-1.9%) this month. The top-performing portfolio stocks were a Pakistani tobacco company (+42.8%), followed by a Pakistani textile company (+30.9%), a Mongolian leather and fur producer (+26.7%), and a Bangladeshi textile company (+26.6%). With upcoming elections in Bangladesh there are currently some social and political issues playing out which may impact production and distribution functions of companies and this would possibly impact their earnings in the last quarter of 2013. In November, we added to existing positions in Bangladesh, Laos, Mongolia, and Vietnam. We sold a Pakistani textile company stock and bought shares in a Pakistani producer of over the counter medicine products. Additionally, we added one new small cap position to our Mongolia basket: a fire equipment company. Given that total market turnover in Mongolia is frequently less than US$ 200,000, the opportunity to pick up some smaller stocks can come up rather infrequently. The overarching drivers of the Mongolian consumer sector will continue to be linked to the macroeconomic environment so whilst we are not able to pick up every stock we would like on a daily basis, we can continue to buy companies we like in this sector on an opportunistic basis. You can read more about the Mongolian market in the Mongolia Country Report and Investment Summit Notes. As of 30th November, the portfolio was invested in 110 shares, 2 closed-end fund (both with 34% discount to NAV), 1 GDR (with 62.3% discount) and held 11.8% in cash. The two biggest stock positions are a power producer (4.5%) and a financial institution (4.4%) in Laos. The countries with the largest asset allocation are Vietnam (19.0%), Bangladesh (15.8%) and Pakistan (13.2%). The sectors with the largest allocation of assets are consumer goods (42.2%) and financials (11.0%). The weighted average trailing portfolio Price/Earnings ratio (only companies with profit) was 12.4x, the weighted average Price/Book ratio 3.1x and the weighted average Dividend Yield was 4.6%. Mongolia Investment Summit and Mongolia Business Forum Note"Just like others, we do make mistakes. There have been moments when we disappointed the investors. But because we are open, we can correct the mistakes and fix the problems." In November, we attended two Mongolia-themed events in Hong Kong: the Mongolia Investment Summit and the Mongolia Business Forum, which hosted the President of Mongolia. The news coming out of Mongolia over the past year has not been great. Negative press due to the issues between the Government and Turquoise Hill Resources/Rio Tinto regarding the Oyu Tolgoi project has contributed to falling foreign investment and a declining stock market. Oyu Tolgoi Project Location The OT project consists of two phases, Phase I and Phase II. The development of the first phase cost roughly US$6.2 billion (the biggest foreign investment to date in Mongolia) and consists of an open pit mine. Development is now complete, and copper concentrate shipments began in the second half of 2013. The second phase of the project consists of developing an underground mine. Development of this phase was suspended in August 2013 due to certain disagreements between the Government of Mongolia and TRQ/Rio Tinto regarding project financing. This disagreement has impacted foreign investor sentiment which has resulted in much lower foreign direct investment into the country in 2013. In order to fund existing mine development, TRQ had taken on a US$1.8 billion interim funding facility and a US$600 million bridge facility from Rio Tinto. Both of these instruments mature on January 14, 2014. Since the project financing for Phase II cannot close until disagreements between the government and TRQ are sorted out, the upcoming repayment of US$2.4 billion will be refinanced through a rights offering, which will dilute existing shareholders if they choose not to exercise their rights. TRQ claims in its filings that Phase II financing would require Mongolian Parliament approval, whilst government representatives have indicated that approval of Phase II financing has to be decided by the Board of OT LLC. It is possible that if these issues are not sorted out, more damage could be done to investor sentiment and Mongolia's reputation regarding foreign investment. In light of this, most participants at the Mongolia Investment Summit and the Mongolia Business Forum were keen to learn what the outlook was for the country in light of the current OT disagreement. The highlight from both of these events was the talk by Tsakhiagiin Elbegdorj, the President of Mongolia. He was quite frank in his views that certain mistakes have been made and the government is committed to improving the business environment. Hopefully this positive tone can be seen as a sign that the investment climate can improve in 2014. The other government representatives who spoke also gave the impression that they are ready for the country to move forward. A positive sign and hopefully it will translate into action. President of Mongolia at the Mongolia Business Forum, Hong Kong These positive postures and signals by the government have led to changing fortunes for the Mongolian Stock Market with the MSE Top 20 Index up about 10% since the beginning of October in US$ terms. On an YTD basis, the MSE Top 20 Index is down roughly 27.5% in US$ terms and the depreciating Mongolian Tugrik has not helped. Declining foreign investment and a widening current account deficit have led to the Tugrik depreciating by about 25% since the beginning of the year. Though trading volumes on the Mongolian Stock Exchange have dropped in the past year and are lower than some of the other Asian frontier markets we invest in, they have picked up over the past few months with October and November having an average daily value of stocks traded at US$1.2 million and US$0.76 million respectively. This is significantly higher than earlier in the year, when average daily value traded between January-September 2013 was ~US$ 68,000. As of November 2013, there were 262 listed companies on the exchange, of which only 88 traded during the month - which explains why volumes are still low in the market. Stocks on the MSE Top 20 Index, comprised of Mongolia's top 20 companies by market capitalization, have the highest volume and are relatively more liquid than non-Top 20 companies. The Mongolian economy and its stock market are still in the early stages of development and it will not be surprising to see further developments to the stock market in the near future. The exchange recently signed an agreement with FTSE to adopt a global index methodology by Q2 2014 and the Revised Securities Markets Law was also recently passed. Exchange infrastructure has also been upgraded in the past year through a partnership with the London Stock Exchange, which involved implementing a new IT System. Movement of the MSE Top 20 Index and MNT/USD Currency Leaving the OT issue aside, there was not much surprise in what the other resource-focused companies said, as most mineral exports from Mongolia make their way to China. With the Chinese economy slowing, Mongolia's GDP growth has also slowed from 17.5% in 2011 to 11.5% in the first nine months of 2013. Since the first quarter of 2013, however, growth has picked up due to agricultural output and construction. The government has made low cost funds available to finance housing and construction projects and the growth in construction activity is a reflection of this policy. As a result, we were not surprised to see a few Mongolia-focused real estate players at the Investment Summit. Not many may be aware that Mongolia also accounts for roughly 20% of global Cashmere production, and Mongolian Cashmere products are known for their high quality. The growth of the Cashmere industry has led to textile exports from Mongolia reaching US$260 million in the first ten months of 2013, a growth of 21% and accounting for 7.5% of exports. Things Mongolia is known for besides the Oyu Tolgoi Project The negative sentiment in the market due to the OT issue and slowing economic growth has provided us an opportunity to look at some good companies in the non-resource space and we have increased positions in these companies over the past month. Though the macro fundamentals of the economy may not look great due to slower exports and lower foreign investment, the new Investment Law and the OT issue being resolved will help improve these fundamentals going forward. It is a known fact that Mongolia's economy can see significant developments due to the abundant natural resources it possesses and we believe that once the dust settles over the various issues the country is going through, potential winners can emerge and our fund will look to capture those opportunities. Mongolia Country ReportWith an estimated $2 trillion of undeveloped mineral deposits and the Mongolian Stock Exchange (MSE) ranking as one of the world's best-performing bourses in 2010 and 2011, Mongolia's outlook seemed bright until a year and a half ago. Since then, investor confidence has been rattled by a dispute between Rio Tinto, developer of the $6.2 billion Oyu Tolgoi ("OT") copper and gold mine, and the Government of Mongolia ("GoM") regarding revenue shares and the previously-negotiated investment agreement for the project. OT is seen as a litmus test for overall investor confidence in Mongolia, with onlookers watching anxiously to see how the GoM will continue to deal with a vast project that is projected to transform Mongolia. The period from Jan 2012 to July 2013 presented a score of setbacks, however. In July 2012, the GoM passed a foreign investment law that limited foreign ownership to 49% in strategic industries such as mining. In December of last year, an even more stringent minerals law was enacted that levied a 68% tax on profits from mining projects. The Government's overreaching policies towards mining and foreign ownership served to deter investors and contributed to plummeting equity prices both on the MSE and for Mongolia-related equities trading on foreign exchanges in London, Toronto, and Hong Kong. In the first half of 2013, Mongolia's resource-centered economy was battered by the curtailment of foreign direct investment and slumping global commodity prices. In 2013, a 15% dip in the price of coal, Mongolia's largest export, led to a 47% reduction of earnings from coal exports. The Mongolian tugrik - which has historically remained relatively stable - depreciated 15% in Q3 2013 alone, leading to the Tugrik being proclaimed the world's third worst currency in Q3 after Syria and Iran. The Mongolian Stock Exchange has suffered as a result of the recent economic turmoil, with the MSE Top-20 Index dropping 23% in the first half of 2013. Signifying the uncertainties of foreign investment in Mongolia, FDI dropped 17% in 2012 to $3.9 billion and had dropped 49% YoY as of September 2013. But despite the impediments of the last 18 months and the abundance of negative press coverage that Mongolia has received, there have been a number of positive developments for the country's investment outlook. Mongolia's political sphere is one bright spot for the country. On June 26, Presidential elections were held and the Democratic Party incumbent, President Tsakhiagiin Elbegdorj, was reelected with 50.2% of the popular votes. Elbegdorj's victory was cheered by foreign investors and geopolitical analysts who underlined the necessity to structure clear guidelines for dealing with the country's mineral wealth, infrastructure and environmental problems, and widespread corruption. All three Presidential candidates ran on a platform of resource nationalism, but Elbegdorj was viewed by foreign investors as taking the most moderate stance on this issue, as mentioned by AFC Frontier Fund's Fund Manager Thomas Hugger in a CNBC interview on June 26th. Mongolia's peaceful Presidential elections were a very positive sign for investors, as it is not often that one finds a functioning democracy in a resource-rich developing country. With the reelection of the Democratic Party, Mongolian lawmakers were able to move forward with changes to the country's uncertain mining and investment regulations to improve the country's investment climate and sovereign credit rating. In October, Mongolia passed a new foreign investment law to revive foreign investment by relaxing restrictions on investors in strategic sectors, including mining, and by providing greater clarity on the taxes they must pay. The new law removes the distinction between foreign and domestic investors, and private firms will no longer need approval from the GoM to invest in strategic sectors such as mining, telecommunications, and banking. The updated investment law also protects investors from expropriation, allows profits to be repatriated out of Mongolia, and reaffirms the right to arbitration. Additionally, the new law gives investors 5 to 22 years of stability on value added tax, corporate income tax, mining royalties, and customs duties. The newly-enacted investment law will help address foreign investors' concerns relating to the stability of investment projects in Mongolia. Two additional events that would contribute to improved investor confidence would be the successful second funding phase of Rio Tinto's Oyu Tolgoi mine, and concrete steps towards the launch of an initial public offering for Erdenes' Tavan Tolgoi coking coal mine. Mongolia's GDP growth has retreated in recent years, but still remains in double digits. GDP growth reached 11.5% through Q3 2013, and Mongolia's Central Bank Governor announced in November that GDP growth could reach 17% in 2014 due to renewed investor confidence and progress on the $4 billion second phase of development for the Oyu Tolgoi copper and gold mine. Mining exports account for roughly 90% of Mongolia's GDP, and the country is susceptible to changes in commodity prices and China's economic growth - China buys over 86% of Mongolia's exports. Mongolia has been negatively affected by China's slowdown, as the Chinese economy is forecasted to suffer its lowest GDP growth rate in over two decades. Despite China's deceleration, a number of investment agreements were signed in October between Beijing and Ulaanbaatar, including an oil exploration project in eastern Mongolia headed by PetroChina Co. Mongolia is aiming to increase its number of border trade checkpoints with China from one to four and is narrowing down its list of companies bidding to develop Mongolia's railways. Currently, Mongolia's railway tracks are 3.4 inches wider than Chinese tracks, a remnant of the Soviet era. The difference between the two countries' rail lines requires trains exporting coal from Mongolia to China to switch train cars at the Chinese border, significantly increasing the cost of railroad freight export. Proceeds from a USD-denominated $1.5 billion sovereign bond issued in November 2012, the 10-year "Chinggis Bond", are being used to finance Mongolia's New Railway, with the aim to build a 1,800-km railway by 2016. Mongolia is also looking to issue up to US $1 billion of Japanese yen-denominated sovereign debt in either 2013 or 2014, and may potentially explore the feasibility of issuing Chinese Yuan-denominated bonds to help finance expansions in Mongolia's energy and transport infrastructure as the country gears up to increase exports and production. We believe that Mongolia's renewed stance on foreign investment and the legislative changes that have been made should contribute to improved investor confidence in the country. Mongolia remains well-positioned for fundamental long-term growth, with an estimated $2 trillion of undeveloped minerals and over $10 billion already committed to deep mining and infrastructure projects. Mongolia's small population of 3 million stands to experience major benefits from the country's projected economic growth, as existing mining projects have just scraped the surface - only 17% of Mongolia has been explored thus far for commodity deposits. This overall increase in economic welfare will support growth in consumer, building materials, and financials stocks as income levels rise. The GoM has also made progress on initiating a new program that will provide 20-year mortgages at 8% to home buyers, instead of the previous 17-20%. Additionally, Mongolia's central bank is altering its monetary policy strategy to make the economy less vulnerable to swings. Mongolia still presents many opportunities to investors, and valuations on many stocks on the MSE are at 1-year lows and trading at substantial discounts to book value. For investors who believe in Mongolia's long-term growth potential and the steps that the country is taking to rectify its mistakes and rebuild investor confidence, now is a good time to invest in fundamentally-sound Mongolian equities at bargain prices. We would like to wish all of our valued clients and newsletter readers a Merry Christmas and Happy New Year. We look forward to continuing to bring you news from frontier markets across Asia in 2014. Thomas Hugger Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

| GO TOP |