Asia Frontier Capital (AFC) - December 2013 Newsletter |

|||

In this IssueAsia Frontier Quick Links |

"A good hockey player plays where the puck is. A great hockey player plays where the puck is going to be." We would like to wish all our readers a happy New Year and utmost investment success in 2014. In this month's newsletter we bring you for the first time the fund manager comments for the AFC Vietnam Fund as well as the AFC Asia Frontier Fund. With both funds experiencing gains through the end of 2013 and our deepening coverage of Vietnamese equities, 2014 stands to be a very exciting year ahead for Asia Frontier Capital and all of our investors. This month’s edition includes an update on all of AFC’s recent news and media coverage and details on the upcoming AFC Vietnam Fund roadshow. With the launch of the new fund, the AFC team spent the holiday season doing research and bringing new investors into the fund. As such, our usual country and travel report will be replaced with an in-depth Vietnam market update. Finally, we would like to announce that AFC Asia Frontier Fund will lower the minimum investment to USD/EUR/CHF 25,000 after a limited offer that featured in Chris Mayer’s ‘Mayer’s Special Situations’ investment newsletter. This offer is limited to NAVs subscriptions that are received for January and February 2014. How to Invest in AFC Asia Frontier Fund and

|

||

| January 2014 – Europe Zurich 13th-17th London 20th-22nd Geneva 23rd-28th |

February 2014 – Asia Singapore 10th-14th Hong Kong 17th-21st |

To enquire about a meeting, please be in touch with our Vietnam team at:

AFC Asia Frontier Fund Manager Comment

AFC Asia Frontier Fund (AAFF) USD A-shares gained +3.2% in December 2013 outperforming the MSCI Frontier Markets Asia Index which was up +2.7%.

In December, the best performing indexes within the AAFF universe were Mongolia (+6.5%), Vietnam – Hanoi VH Index (+4.1%), and Pakistan (+4.0%). Interestingly, the Vietnam Ho Chi Minh VN Index lost 0.6% this month. The top-performing portfolio stocks were a Mongolian trading company (+47.0%), a Mongolian coal mine (+41.1%), a Pakistani brewery (+27.0%), and a Mongolian meat processor (+24.7%). In December we added to existing positions in Mongolia, Pakistan, Sri Lanka and Vietnam and reduced some positions in Mongolia. We sold a Pakistani ETF and three Mongolian stocks: a copper mine and two coal mines.

In Pakistan, Prime Minister Nawaz Sharif’s government continued with reforms in line with the conditions of the IMF assistance package. Whilst the markets saw a rally of 49.4% in 2013, the country's foreign reserves have continued to slide and fell 60% over the past year to reach a staggeringly low USD 3.7 billion as of the 2nd of January 2014. This period also saw a depreciation of Pakistan’s currency, which fell 8.4% over the last year. Though economic growth rebounded in the latter part of 2013 due to certain power sector reforms, investors will keep a close eye on further reform measures and expect more progress to be made in the near future. Pressure on foreign reserves is expected to continue as repayments of USD 1.3 billion are due to the IMF in 2014, which may lead to continued pressure on the local currency.

In Bangladesh, the benchmark DSE Broad Index was up +0.85% in December despite political violence and social unrest due to the parliamentary elections in which the main opposition parties boycotted elections. Sheikh Hasina’s Awami League won 232 parliamentary seats out of 300 after the main opposition leader, Khaleda Zia of the Bangladesh National Party, led a campaign of disruptive strikes and business shutdowns. There were approximately 71 days of potential production lost over the past year; well above the average of 46 days per year since 1991. These shutdowns have hampered business activities in large cities such as Dhaka and Chittagong and it is possible that companies could have a poor showing in their latest quarterly earnings and any panic in the market over the political process can be seen as an opportunity to buy good companies, which we like. Pressure from international governments could possibly lead to a compromise between the warring political parties, which may lead to fresh elections. A similar situation occurred in February 1996 when the current incumbent Awami League boycotted elections, which led to disruptions and thereafter fresh elections were held in June 1996. We believe that this short term pain does not dilute the potential that the Bangaldesh economy and its companies hold.

As of 31st December 2013, the portfolio was invested in 109 shares, 1 closed-end fund (with 36% discount to NAV) and 1 GDR (with 62.9% discount). The two biggest stock positions are a financial institution (4.4%) and power producer (4.2%) and in Laos. The countries with the largest asset allocation include Vietnam (19.1%), Bangladesh (14.9%) and Pakistan (14.2%). The sectors with the largest allocation of assets are consumer goods (43.2%) and financials (11.0%). The fund’s weighted average trailing Price/Earnings ratio (only companies with profit) was 12.67x, the weighted average Price/Book ratio 3.34x and the weighted average Dividend Yield 4.26%.

AFC Vietnam Fund Manager Comment

The AFC Vietnam Fund was launched on 11th December 2013 and started investing on 23rd December 2013. During the 7 trading days the fund invested approximately 66.2% of its assets. The fund gained +2.4% in December 2013, outperforming the Ho Chi Minh Stock Index “VN Index” (-0.8%) and Hanoi Stock Index “VH Index” (-0.7%) - performances as of 23rd December 2013. The fund portfolio is currently underweight large caps relative to the VN Index, VH Index and major ETFs due to favorable relative valuations in small to mid-cap stocks.

At the end of December 2013 the fund’s largest positions were: Cat Loi JSC, a materials/packaging company (2.9%), Bao Viet Securities (2.5%) and VN Direct Securities Corp (2.3%) which are both brokerage companies, Sam Cuong Material Electrical and Telecom Corp (2.3%) which is a manufacturer of electrical and telecom equipment and Sonadezi Long Thanh Shareholding Company (2.1%), a real estate company.

Retail investors in Vietnam have begun to search for alternative investments as returns from investing in gold and USD have declined. Local investors from Vietnam have historically invested heavily in these two assets so a shift to the stock market – which many see as also the only legal way to gamble to make quick profits – would certainly help small and mid-cap stocks. From a trading perspective it is possible to see heavy interest on many of our existing stocks when the market sees even modest gains which represents an excellent opportunity.

The technical situation is extremely interesting in the face of increasingly positive economic data from Vietnam. You can see from these two long term charts of the HOSE (Link) and HNX (Link) indices that they have seen a long consolidation phase. Hopefully a few more strong trading days will push the market into a new phase and long-lasting upward trend!

Next month’s trading looks to be positive as the time from New Year to the holiday period for Chinese New Year - called Tet in Vietnam - is usually very positive for the stock market which makes us quite optimistic. Please note that the stock market will be closed for Tet from 28th January until 5th February.

As of 31st December 2013, the portfolio was invested in 57 shares and held 33.8% in cash. The sectors with the largest allocation of assets were consumer goods (23.6%) and industrials (14.0%). The fund’s weighted average trailing Price/Earnings ratio (only companies with profit) was 6.15x, the weighted average Price/Book ratio was 0.93x and the weighted average Dividend Yield was 7.43%.

If you are interested in more information, please be in touch with our Vietnam team at:

Vietnam Market Update December 2013

"My sense is that at the present time, the US market is relatively expensive compared to foreign markets. On a cyclically-adjusted P/E basis, it is actually going to return very little over the next seven to 10 years". "I think the Vietnamese stock market, which in 2013 was up 22%, will continue to go up."

- Marc Faber, on CNBC 19th December 2013

In light of our recently launched 'AFC Vietnam Fund' we thought it would be a good idea to give our readers an update on Vietnam since we last wrote on the country in August 2013.

Our most recent trip to Vietnam was in August 2013 when Senior Investment Analyst Ruchir Desai spent a week in the country visiting Hanoi and Ho Chi Minh City. We liked what we saw then and mentioned that the economy was stabilising from the boom of 2008-09. Inflation had come down from high double digits in 2012, industrial production and GDP growth appeared to be improving and credit growth was stable.

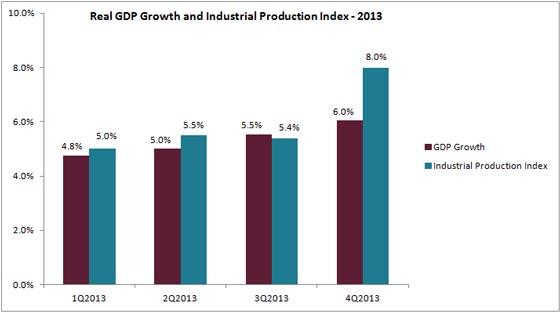

Just over a quarter later, the situation appears to be better and economic data points are improving. Real GDP growth in 2013 was estimated to be 5.42% compared to 5.25% in 2012. Further, GDP growth picked up over the past few quarters with 4Q2013 GDP growth at 6.0%. The Industrial Production Index reported growth of 5.9% in 2013 compared to 4.8% in 2012 while industrial growth picked up in the last quarter of 2013 to 8.0%.

Source: General Statistics Office of Vietnam

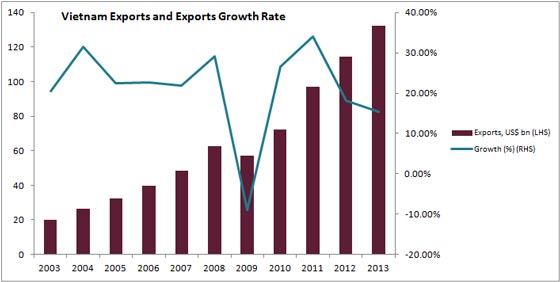

Exports grew by 15% in 2013 to USD 132 billion as Vietnam continues to be an attractive destination for foreign manufacturers. This is not surprising given its young and educated population with a median age of 28.5 and literacy rate of 93%. One of the major benefits of manufacturing in Vietnam is the lower wage rates relative to China, which is causing companies to tap Vietnam as a manufacturing base since it fits into their supply chain nicely due to the country's close proximity to China and Southeast Asia's shipping channels.

A recent HSBC report, "2014: the Year of Exporters," listed Vietnam as one of the countries that stands to gain the most from the recovering demand of the US and European economies, with exports projected to grow at 20% in 2014. Foreign direct investment, much of which was in manufacturing, grew sizeably in 2013 to USD 21.6 billion, helping Vietnam record a trade surplus of USD 900 million last year, bucking the country's trend of repeated trade deficits.

Samsung, which already has operations in Vietnam, is expected to begin production at its USD 2 billion manufacturing facility in February 2014. This facility will be manufacturing Samsung mobile phones and it is estimated that Vietnam will account for 40% of Samsung's mobile phone production by 2015.

Source: Asian Development Bank, General Statistics Office of Vietnam

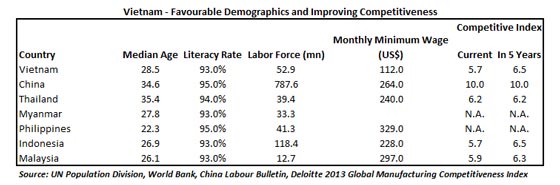

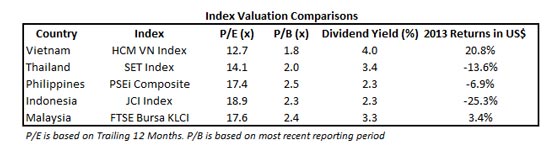

The table below illustrates why Vietnam is becoming an important manufacturing destination for many conglomerates. Vietnam is on par with its peers with respect to literacy rates and has a labour force of 52.9 million, which is higher than that of Thailand. More importantly, minimum wages are more than half of those in other neighbouring economies. In the 2013 Deloitte Manufacturing Competitiveness Index, Vietnam compares favourably with its peers such as Thailand, Indonesia and the Philippines. The country is also expected to increase its competitiveness in the next five years to put it on par with most of its peers in the region.

On the monetary front, credit growth has been stable and is expected to be between 9-10% in 2013 compared to 8.8% in 2012. This is not a surprise as the banking system is still grappling with the issue of NPLs (non-performing loans) but the market has been aware of this issue for a while. NPLs have picked up from 4.64% to 4.73% since we last wrote in August 2013 but it is quite a well-known fact that a more accurate approximation of NPLs is anywhere between 10-14%.

The NPL issue had given rise to the creation of the Vietnam Asset Management Company (VAMC) in July 2013. The VAMC is essentially like a bad bank and will be used to buy the banks' NPLs in exchange for bonds. It is estimated that the VAMC bought bad debts worth USD 1.8 billion in 2013 and these purchases are expected to reach USD 3.3 - USD 4.7 billion in 2014. Purchases of NPLs by the VAMC are expected to help loosen credit growth but we will have to wait and watch how that pans out.

As mentioned in our previous note which you can read here (link), in spite of issues surrounding banks and real estate, the economy continuous to stabilise and there are quite a few non-financial companies which continue to do well. We have researched both large cap as well as small-mid cap names which offer value, growth, and more importantly, are doing well fundamentally.

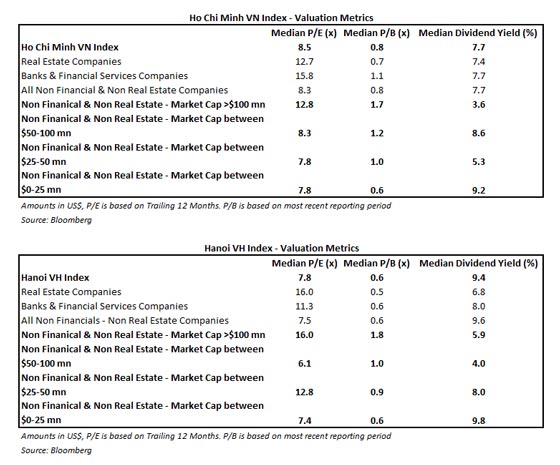

There continues to be a host of companies which are under-researched and we endeavour to capture those opportunities through both the AFC Vietnam Fund and the AFC Asia Frontier Fund. For instance, the VN Index has 302 stocks listed, of which 40 companies have a market capitalisation of over USD 100 million. The fact that most investors have so far focused primarily on the larger companies has left room to uncover opportunities in the small and mid-size space (there are 262 companies with a market cap below USD 100 million).

To take this a step forward, if we leave out banks, financial services and real estate companies on the VN Index, we have a sample of about 243 companies consisting of large cap and small/mid cap names, and the valuation gap between larger names and small/mid cap names is evident, as reflected in the table below. The same is the case for the Northern bourse in Hanoi, where the VH Index has many more companies below the USD 100 million market cap range which allows us to find value in this large sample.

The tables below indicate that there is enough juice in the small-mid cap names, as the sample companies trade at lower valuations than larger names and also offer attractive dividend yields. Our assertion is not that all the companies below a market cap of USD 100 million will be winners, as some may trade at a low valuation for a reason (poor fundamentals or poor business) but with consistent research we have found stocks that are fundamentally sound, are growing, offer value, and are overlooked by most institutional investors. This is where one can find an edge. We have used Median multiples instead of Mean in order to leave out the effects of outliers.

Small/Mid-Cap Names are Under-Researched and offer Value

The Vietnamese economy continues to stabilise and get back on its feet and the authorities appear to be committed to improving market sentiment and continuing reforms. Strategic foreign investors will now be able to buy up to a 20% equity stake in Vietnamese banks (previously 15%), which should help strengthen banks' capital needs. Furthermore, there is talk of raising foreign ownership limits in listed stocks of some sectors from the current 49% to 60%, as there are about 20 large cap companies whose foreign ownership limits have been reached.

Besides these policy moves, there appears to be a sound platform for Vietnamese equities to do well: favourable demographics, increasing consumption, attractive valuations, and under-researched companies. We expect to be on the ground in Vietnam again in 1Q2014 and will report back. In the meantime, we expect to continue reporting on the positive news flowing out of Vietnam!

Source: Bloomberg

With kind regards,

Thomas Hugger

CEO & Fund Manager

Disclaimer:

This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved.

The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative.

By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions.