Asia Frontier Capital (AFC) - October 2013 Newsletter

In this IssueRemittances: Quick Links |

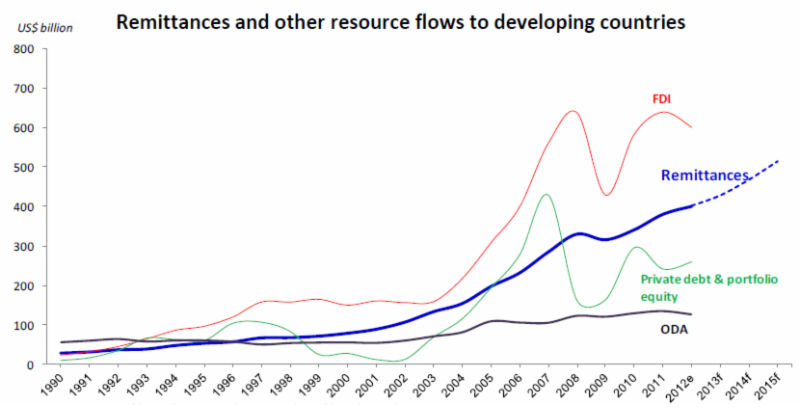

Welcome to the October edition of the Asia Frontier Capital Newsletter. This month's highlights include the return of our CEO from his trip to Switzerland and the UK, as well as the return of our Senior Investment Analyst from his research trip to Iraq. The AFC team will also be enlightening you about remittances, a major unsung driver of growth in frontier markets. As an Asian focused frontier markets fund with our head office in Hong Kong we have begun the process of providing greater access to our fund for investors based in Asia. As such we will be expanding our investor material to include publication in local Asian languages in the future. This month you will get a sneak peek into these upcoming changes as we have included a Chinese (traditional) language translation of our investor presentation. Watch this space for more in next month's edition! We would also like to take this opportunity to extend a personal welcome to all of our new clients who came on board in October. With the completion of our European roadshow, new investors looking to come on board at this month's NAV are encouraged to be in touch with Stephen Friel at We are also pleased to introduce two non-executive directors of Asia Frontier Capital Ltd: Hon. Andrew Fraser is the former CEO of Baring Securities in the UK, Chairman of Equity Partners Ltd., a Bangladesh investment bank, and Chairman of Bridge Securities amongst other posts. He is a graduate of St John's College, Oxford after which he held numerous posts in the financial sector both in London and around the world. At present he is based in London and is a globally focused investor. Kh. Asadul Islam is the Managing Director and CEO of City Brokerage Limited, a wholly-owned subsidiary of The City Bank Limited. Prior to his appointment as Managing Director and CEO, he held the position of Executive Vice President and Head of Brokerage of The City Bank since July 2009. Mr. Islam was former CEO of IDLC Securities Limited and played a key role in setting up the company. In his 16 years of work experience in Bangladesh capital market Mr. Islam has an excellent track record at generating growth in frontier market businesses as well as working with new clients to build investment opportunities! Fund PerformanceTwo main reasons why investors look to frontier markets for investment opportunities are the long-term opportunities these markets present and the lower correlation with global markets that provide a diversified portfolio buffer in case of economic turmoil. One of the benefits of managing a low-correlation portfolio is listening to investors discuss the resilience of returns when markets are down across the board. One of the downsides is that there are also comparisons of the same portfolio when other asset classes see a significant rally. A key focus of the AFC Asia Frontier Fund (AAFF) is to give investors exposure to the long-term growth prospects in frontier markets by holding a selection of stocks that can reduce volatility whilst capturing equity returns from increasing consumption. This strategy benefits investors by offering diversification opportunities across asset classes in markets which have economic cycles that remain largely independent of each other. In October 2013, AAFF USD A-shares returned -1.45% after outperforming the MSCI Frontier Asia Index over the past two months. The MSCI Frontier Asia Index (+4.8%), MSCI Frontier Markets Index (+2.4%) and the MSCI World Index USD (+3.8%) all gained with a positive shift in sentiment seeing a rally across emerging and frontier markets. There was a particularly strong performance by cyclical stocks, blue chip stocks, and the Pakistan index, all of which have a proportionally lower weight in the AAFF portfolio. AAFF has a structured long-term defensive allocation strategy with a lower weighting to big name index stocks, typically due to their valuations. Some of these stocks have their prices pushed up by foreign investors who look for shorter term exposure and are willing to pay a premium for liquidity. Should foreign investor sentiment move to become more negative in the short term, it is likely that these same stocks may face increased selling pressure. Whilst large-cap stocks make up some of the fund's holdings, a main part of the AAFF strategy is to hold stocks longer term that have been picked up at attractive valuations whist collecting dividends. It is not a new concept that all parts of the stock market do not move in the same direction at the same time, but the idiosyncrasies of this dynamic can be missed when simply tracking composite indices. AAFF also remains underweighted on Pakistan when compared to the MSCI Frontier Asia Index due to ongoing potential macro weakness which could lead to volatility in the future. This potential volatility was evident on the last day of this month's trading when the Pakistan index (KSE100) rallied +2.1% in a single day. As of 31st October 2013, the portfolio was invested in 109 shares, 2 closed-end funds (with 34% and 36% discount to NAV), 1 GDR (with 55.2% discount), and held 9.0% in cash. The two biggest stock positions are a power producer from Laos (4.2%) and a pharmaceutical company from Bangladesh (4.0%). The countries with the largest asset allocation are Vietnam (20.2%), Bangladesh (16.2%) and Pakistan (12.1%). The sectors with the largest allocation of assets are consumer goods (45.0%), materials (10.8%), and financials (10.4%). The fund's weighted average Price/Earnings ratio was 11.9x, the weighted Price/Book ratio was 2.7x, and the portfolio dividend yield was 4.52%. Remittances - Unsung Capital Flows to Frontier MarketsWhen people think about money flowing into frontier markets and developing countries, the first things that spring to mind are usually foreign direct investment (FDI) and foreign aid. Remittances, however, receive very little attention despite their monumental size. The world has approximately 232 million foreign workers who remitted US $401 billion in 2011. Remittance flows are expected to grow at 8.8% annually for the next two years to reach US $515 billion by 2015. Though these sums of money are staggering, the real value of remittances still remains drastically under reported as 25-50% of those who report sending sums of money home did so person-to-person rather than through formal channels such as banks or money transfer companies. The importance of this is drastically underemphasized even as international agencies such as the World Bank and IMF have begun to take the level of remittances into consideration when calculating sovereign creditworthiness in some countries (including Vietnam).

Sources: World Development Indicators and World Bank Development Prospects Group Increases in remittances sent to Pakistan and Bangladesh in recent years have pushed South Asia to become the largest regional recipient in the world, growing 12.3% to US $109 billion in 2012. Pakistan, Bangladesh, and Vietnam all receive at least US $1 billion per month in remittances and this will continue to increase. Private foreign workers from Bangladesh, Pakistan, Nepal, and Sri Lanka send home more money collectively each year than each of their countries hold in foreign reserves. Furthermore, the vast sums of money being transferred will continue to bolster the overall balance of payments in these markets as well as support the local currencies. Looking forward, the AFC universe is likely to see remittance growth continue in the future as the skilled foreign workers who are currently abroad begin to earn higher salaries as the result of human capital investment in previous generations. Tens of millions of increasingly educated, tech-savvy young persons are poised to enter the workforce in the coming years with skills that will be desired at the competitive wages they demand. Some frontier markets in Asia may have the potential to move towards the levels of more economically advanced remittance giants such as China and India, countries which sent home US $60 billion and US $69 billion respectively in 2012. Whilst it may be suggested that the large populations of India and China could diminish the importance of remittances in their current growth story, this does not detract from the importance of this factor in nearby frontier countries. Emerging market growth will be impacted by remittances from their own foreign workers and will benefit the frontier as the growth of wealth in these markets will see both an increased emigration by poorer neighboring countries as well as a growth destination for exports. There is in fact more migration between countries in the developing world than from developing to developed. In 2012, foreign workers in India remitted US $2.2 billion to Pakistan and US $6.6 billion to Bangladesh alone. In smaller, less-developed countries remittances do not just play a part in the growth story but are the dominant source of economic growth. In Nepal, these flows make up 25% of total GDP and as much as 48% of total GDP in other frontier countries such as Tajikistan. The continued rise of remittances around the world depends on two factors: the continued permission of nationals to work overseas and the employment situation in the host country. North America as well as Europe have seen economic upheaval in recent years and a surge in unemployment. In times of economic despair it is frequently the case that employment nationalism rears its head to the detriment of foreign labour participants. Many overseas workers, however, are skilled laborers, as it is primarily skilled individuals who emigrate and then send money home to their families. This trend will continue to support the returns on education in developing countries, which will support future growth in domestic human capital, whilst simultaneously increasing domestic consumption and investment in the near term as these funds are spent.

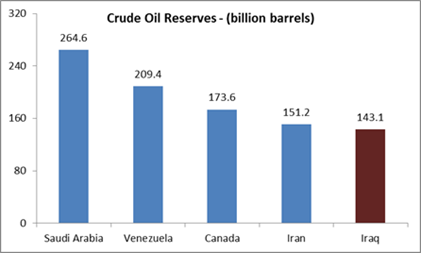

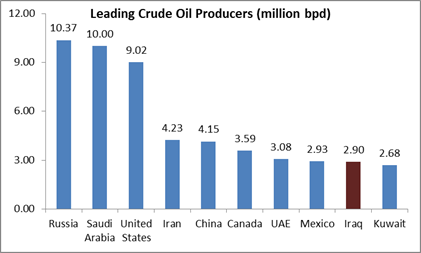

Country Snapshot: IraqEvery month we highlight economic developments in one country within the Asia Frontier Capital Universe. If I told you of a country that has tripled its oil production in the last decade, posted GDP growth rates of 8% in 2012 and 9% in 2011, and seen the market capitalization of its stock exchange grow by 40% in 2011, 23% in 2012, and over 100% in 2013, you would likely be bullish, and perhaps in disbelief. Generally portrayed by Western media as a "basket case" state, Iraq is quietly undergoing an economic revival thanks to its resurgent oil sector and growing interest in the country from foreign corporations. Crude oil production is driving Iraq's boom, and output has soared in the last five years as the security situation has improved and the country has signed drilling and exploration contracts with numerous international energy companies including Exxon-Mobil, BP, Shell, and Total. Last year, Iraq reached a 30-year high of 2.6 million barrels per day (bpd) of crude oil export and the country is forecasted to average 3.3 - 3.5 million bpd in 2013. This is a massive increase from only a decade ago - at the time of the Iraq War in 2003, production was merely 1.3 million bpd. Current production in the country is just scraping the surface. Iraq has the world's 5th largest reserves of crude oil and is now the 9th largest exporter of crude in the world. Iraq's aggressive ramp-up in output can be attributed to the country's new Integrated National Energy Strategy (INES), developed in cooperation with The World Bank and Booz & Company. The plan is targeting production of 4.5 million bpd by the end of next year, with an ambitious goal of 9 million bpd by 2020. The INES projects that to hit its output targets, Iraq will need a whopping $620 billion (equivalent to almost 3x Iraq's 2012 GDP of $210 billion) invested in its oil and gas-related industries through 2030. That is a formidable sum for a country in which oil revenues make up 95% of the government budget and post-war reconstruction, poor infrastructure, tumultuous regional neighbors, and ongoing security concerns remain daily challenges. Despite the magnitude of investment required, the INES also sees a huge potential payoff, forecasting that Iraq's oil and gas industries could generate roughly $6 trillion for the country before 2030 based on an estimated price of $100 per barrel. A looming question mark over Iraq's oil bonanza is the division of revenues between Baghdad and Iraqi Kurdistan, an autonomous oil-rich region in northern Iraq. Tensions have simmered as Erbil, Kurdistan's capital, has unilaterally signed agreements with large foreign oil companies without the approval of Baghdad. Thus far, no agreement has been reached between the two sides, although Turkey, which is forging increasingly close ties with Kurdistan, has stated that it will support an agreement in which 83% of oil revenues go to Baghdad and 17% of revenues go to Iraqi Kurdistan. A telling sign of the growing friendship between Turkey and Iraqi Kurdistan is the two pipelines that Kurdistan has planned to export crude via Turkey, bypassing Baghdad. Construction on the first pipeline, which will connect to an existing pipeline with a capacity of 1.5 - 1.6 million bpd, has now been completed and exports are scheduled to begin in Q1 2014. Additionally, Kurdistan recently announced plans to build a second oil pipeline to Turkey within the next two years with a capacity of 1 million bpd. Turkey, a regional heavyweight that depends on oil imports, has sought to strengthen its relations with Kurdistan and has supported the autonomous region's target of 3 million bpd. Foreign companies are increasingly signing agreements and exploring business opportunities in Kurdistan, and according to the Kurdistan Regional Government (KRG), there are nearly 2,700 foreign companies registered in Kurdistan, compared to just 900 foreign companies present in the rest of Iraq. Erbil's better security and more favorable ownership laws have made it more attractive to foreign businesses than Baghdad. In Kurdistan, a foreign investor can own a business and open a local office outright, while in the rest of Iraq, a foreign investor must partner with a local Iraqi company or businessman to set up shop. Kurdistan is eager to use its oil revenues to build a more diversified regional economy. Despite its large volume of oil exports, Kurdistan remains heavily dependent on cheap imports of foodstuffs, clothing, and basic consumer goods from Turkey and Iran, the region's two largest trading partners. The KRG is seeking to address this overreliance on crude with plans to build industrial zones to attract more private-sector investment in non-petroleum sectors. Apart from the skyrocketing oil production of the country, there has also been large growth in other sectors, reflected in the Iraq Stock Exchange (ISX), the sole bourse in Iraq. Launched in 2004 and opened to foreign investors in 2007, the ISX only began electronic trading in 2009. As of Q3 2013, the ISX had a market capitalization of $9.66 billion, with 82 listed companies in the banking, telecoms, hotels/tourism, industry, insurance, and consumer goods sectors. The bourse's market capitalization grew by 40% in 2011 and 23% in 2012, primarily due to the banking sector's growth, and then more than doubled in February when Qatar Telecom's Iraq subsidiary, AsiaCell, launched an IPO that floated a quarter of its stock. The $1.3 billion listing was the biggest IPO in the Middle East since 2008 and was heavily oversubscribed. AsiaCell's successful listing will soon be followed by IPOs from Kuwaiti giant Zain's Iraqi subsidiary, which may be bigger than AsiaCell's debut, and Korek Telecom, part-owned by France Telecom SA. All three firms are mandated to float 25% of their stock as part of their operating licenses. Foreign investor interest is growing, and foreigners comprised 70% of AsiaCell's February IPO. Through Q3 2013, foreigners' shares made up 32.9% of trading volume on the ISX, and this should continue to grow thanks to improved regulatory changes made this year. The ISX recently introduced a custody license to provide more security for foreign investors and to allow larger brokers to invest in Iraq. Most large institutional investors and emerging market mutual funds are required to have their shares held by custodians, and this development will encourage more foreign participation on the Iraq Stock Exchange. With growing oil revenues and an improving macroeconomic situation ($70billion of foreign reserves and very little debt), Iraq will need to take action to address some of the lingering problems that are holding the country back. Unemployment is high and private-sector investment outside of the oil and gas sector is low. The government should focus on liberalizing its economic policies to encourage both foreign and domestic investment, diversify its economy and revenue streams, and control inflation and the weakening of the Iraqi dinar. More alarming is the recent deterioration in Iraq's security situation. Baghdad has been hit by its worst wave of violence since 2008, with more than 5,500 people killed in attacks this year. The ongoing Syrian conflict has been blamed for sparking renewed al-Qaeda activity in Iraq and Iraq's simmering sectarian tensions are being exacerbated by the Syrian crisis. The al-Qaeda-affiliated Islamic State of Iraq and al-Sham (ISIS) claimed responsibility for a September suicide attack in Erbil that killed seven people. A number of ISIS fighters have reportedly entered Kirkuk province, which borders Iraqi Kurdistan, from Syria. Apart from the Erbil attack, however, Kurdistan has remained safe and Kurdish forces are tightening security in response to the recent threats. Even with the ongoing turmoil and pressing challenges, Iraq appears to have emerged from its darkest days and is making gradual progress on the long road to post-conflict recovery. If the country can manage its oil revenues prudently, the petrodollars could go a long way towards rebuilding a country that has suffered for far too long. Foreign investment in Iraq's private sector, whether from international oil corporations, enterprising regional businessmen, or the adventurous frontier market investor, is key to ensuring Iraq's continued economic growth and prosperity. Asia Frontier Capital is excited to take part in the compelling investment story of Iraq's recovery. Travel Report: IraqIn line with our process of being on the ground in the countries we invest in, Ruchir Desai, Senior Investment Analyst, recently travelled to Iraq to attend the 3rd annual Rabee Investor Conference held in Erbil, the capital of Iraq's Kurdistan region. It might seem surprising that Asia Frontier Capital recently attended an investor conference in Iraq, as news coming out of the country usually focuses on Iraq's turbulent security situation and ongoing sectarian violence. However, instability is just one side of the story. Crude oil production in Iraq has risen from 1.3 million barrels per day (bpd) in 2003 to an expected 3.3 million bpd this year, making Iraq now the 9th largest producer of crude oil in the world. Per capita GDP at the end of the Iraq War in 2003 was US $1,352/capita but is forecasted to hit US $6,377/capita in 2013, higher than many emerging economies. The post-war resurgence in oil production has helped build up the country's foreign reserves, now roughly US$ 70 billion, contributing to a stable macroeconomic environment for the country despite the security issues that it faces. Iraq has the fifth highest crude oil reserves but is the 9th largest producer (as of 2012) 2013 has witnessed an increase in violence in Iraq, which has been concentrated in and around Baghdad. Most people are not aware, however, that Iraqi Kurdistan, an autonomous region in the north, is far more stable and peaceful relative to other parts of Iraq and has experienced few security-related incidents in the past five years. Iraqi Kurdistan, located in the north-eastern part of Iraq, is recognized by the Iraqi constitution as an autonomous region with its own elected government. Though there are a number of competing political parties in Kurdistan, there appears to be consensus when it comes to maintaining stability in the region, as Kurdistan possesses much of Iraq's oil and gas reserves. This focus on stability is one reason why many foreign oil and gas companies have established operations in Kurdistan. Erbil, the capital, has seen a fair amount of development as many foreign companies have set up offices in the city. There are plans to launch the Erbil Stock Exchange next year, which would likely lead to heightened investor interest in Iraq and Iraqi Kurdistan going forward.

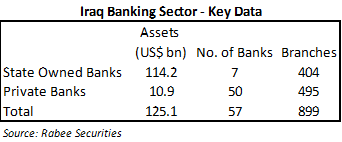

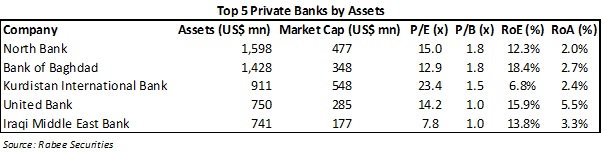

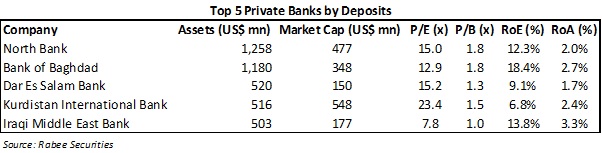

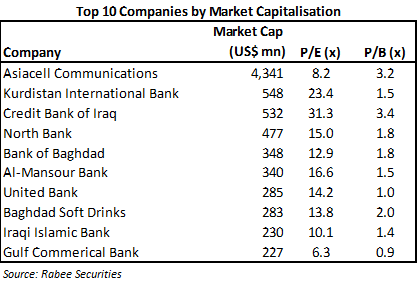

Erbil is well connected to the rest of the Middle East and parts of Europe, with flights to Doha, Dubai, Istanbul, Vienna, and Frankfurt. Foreign investor interest in Kurdistan has led to the development of various five star hotels in Erbil, but supply seems limited as room rates are still quite high (US$200-250 a night). I did notice a Hilton hotel under construction close to where I was staying. Despite all the issues and concerns surrounding security, it was a good sign to see that the conference was very well attended by various foreign institutional investors focusing on frontier markets. The companies that attended were a diverse mix from the banking, telecom, and non-financial sectors. The Iraqi ISX index is skewed towards banks and telecom, as these sectors make up about 90% of the stock market capitalization due to the large market cap of the telecom giant Asiacell Communication (the Iraqi business of Ooredoo Telecom of Qatar). Going forward, Kuwait-based Zain Telecom plans to list their Iraq business in 2014. On a macro front, the under-penetration of private banks in Iraq was striking. At present, the banking industry in Iraq is dominated by state-run banks, namely Rashid Bank and Rafidan Bank. Private banks make up just 9% of total banking assets! The primary reasons for this are that the Iraqi economy is still dominated by the state and that private banks are not on a level playing field, as they cannot lend to state institutions. Any change in these regulations would make private banks a good way to play the Iraq story, as credit to the private sector is estimated to be about 15% of GDP, much lower than in the region and also globally. If the private banks are able to increase their penetration into the economy, we could possibly see an improvement in RoEs as most private banks are not heavily levered leading to lower RoEs for the industry. On the last evening of my stay a group of us went into town to check out the historic "Erbil Citadel Town" which is a UN World Heritage Site. The citadel town is regarded as the oldest continuously inhabited settlement in the world and is believed to have been in existence for around 7,000 years. Pretty historic! We took a cab from outside the hotel and because one of our group members spoke Arabic, communication was not an issue. Getting out of the hotel was a good way to get a feel of the Erbil way of life. The area next to the citadel was bustling - it seemed to be a meeting point for the local population. The area outside the citadel has been developed with parks and water fountains and is also lined with various shops and restaurants, making it the preferred hang-out place for locals. I did notice a few security officers walking around with AK-47s, which didn't surprise me, but the security situation seemed relatively calm. Unfortunately, the citadel was closed to public viewing at that time of the day so hopefully I can check it out from the inside next time! The Erbil Citadel Though there are some sticky issues between the Kurdish and Central Iraqi governments with respect to oil and gas contracts, the development of Iraqi Kurdistan provides the country with a solid platform to fulfill its potential. Hopefully, oil revenues will help Iraq emulate its peers in the region with respect to economic development. I look forward to returning to Iraqi Kurdistan next year to witness the developments the various companies have made! Please do not reply to this email address. This is a pure outgoing mailbox and your replies will not be read. If you have any questions or comments, please write an email to Kind Regards, Disclaimer:This document does not constitute an offer to sell, or a solicitation of an offer to invest in AFC Asia Frontier Fund, AFC Asia Frontier Fund (non-US), AFC Vietnam Fund or any other funds sponsored by Asia Frontier Capital Ltd. or its affiliates. We will not make such offer or solicitation prior to the delivery of a definitive offering memorandum and other materials relating to the matters herein. Before making an investment decision with respect to our Funds, we advise potential investors to read carefully the respective offering memorandum, the limited partnership agreement or operating agreement, and the related subscription documents, and to consult with their tax, legal, and financial advisors. We have compiled this information from sources we believe to be reliable, but we cannot guarantee its correctness. We present our opinions without warranty. Past performance is no guarantee of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|

|

GO TOP |