Asia Frontier Capital (AFC) - April 2017 Newsletter |

|||||

In this IssueAFC Asia AFC Iraq AFC Vietnam Fund

|

"The developing world is full of entrepreneurs and visionaries, who with access to education, equity and credit would play a key role in developing the economic situations in their countries." AFC Funds Performance Summary

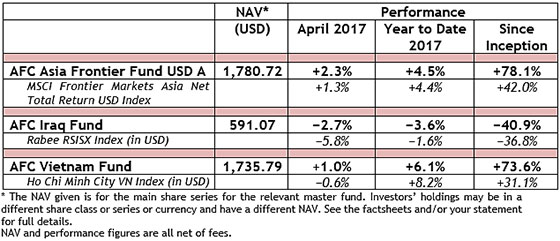

During April 2017, most major equity markets rallied, with the Dow Jones Index gaining +1.3%, the Nikkei 225 Index up +1.5%, the Euro Stoxx 50 Index up +1.7%, and the MSCI Emerging Markets Index up by +2.0%. On the downside, the Shanghai Composite Index lost −0.6% while the UK’s FTSE Index dropped −1.6%. The AFC Asia Frontier Fund gained +2.3% in April, outperforming all indexes mentioned above, and in particular the MSCI Frontier Markets Asia Net Total Return USD Index, which increased by +1.3%. The fund is now up +78.1% since inception, which corresponds to an annualised return of +12.0% p.a. The AFC Iraq Fund returned −2.7% in April and its performance year-to-date is −3.6%. The AFC Vietnam Fund rose +1.0% in April, outperforming the VN-Index in USD which fell −0.6%. The fund is now up +73.6% since inception, which corresponds to an annualised return of +17.9% p.a. Ahmed Tabaqchali, the CIO of the AFC Iraq Fund, presented at the Iraq Stock Exchange Forum on the 8th and 9th of May 2017 at the Mövenpick Hotel in Beirut, Lebanon. The event, titled “Investment Prospects and Trading Technology”, hosted some 30 speakers from Iraq and around the world involved in investing in Iraqi equities. For more information, please see: http://isxforum.com/. After the event, Ahmed commented: “The ISX's forum takes place this year as the Iraqi equity market is emerging from a brutal multi-year bear market. At the same time, the economy is about to emerge from a severe economic decline caused by the triple whammy of losing a third of the country to ISIS, escalating costs of war, and collapsing oil prices. The anticipated end of the ISIS conflict should be the catalyst for capital spending and with it FDI and fund flows to the country. The forum's participants discussed the challenges and solutions for the ISX as it gears up to increase local participation and attract foreign capital to the Iraqi equity market.“ Launch of an AFC Asia Frontier “Parallel Fund” in LuxembourgIn order to provide better and easier access for our European investors, Asia Frontier Capital has decided to launch a “Parallel Fund” of the AFC Asia Frontier Fund in Luxembourg. The launch of AFC Asia Frontier Fund (Lux) is slated for the end of June 2017. The Luxembourg-based fund will invest up to 84% in the existing AFC Asia Frontier Fund and the balance will be invested directly in stocks that the Cayman Islands fund is also holding. We expect that the performance of the Luxembourg fund will be very similar compared to the existing Cayman Islands-based fund. If you have any questions about our funds or would like any additional information, please be in touch with our team at AFC in the Press

Upcoming AFC TravelIf you have an interest in meeting with our team during their travels, please contact Peter de Vries at

AFC Asia Frontier Fund - Manager Comment [MYON]

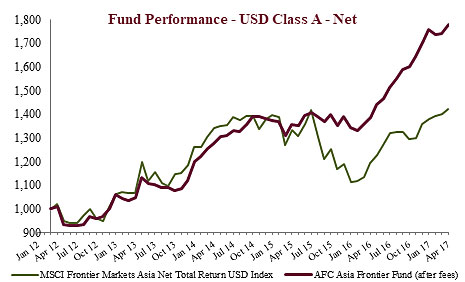

AFC Asia Frontier Fund (AAFF) USD A-shares gained +2.3% in April 2017. The fund outperformed the MSCI Frontier Markets Asia Net Total Return USD Index (+1.3%), the MSCI Frontier Markets Net Total Return USD Index (+1.2%), and the MSCI World Net Total Return USD Index, which was up +1.5%. The USD A shares achieved a NAV of USD 1,780.72 which is a new all-time high (the previous high was in January 2017 at USD 1,757.74). The performance of the AFC Asia Frontier Fund A-shares since inception on 31st March 2012 now stands at +78.1% versus the MSCI Frontier Markets Asia Net Total Return USD Index, which is up +42.0%, and the MSCI Frontier Markets Net Total Return USD Index (+34.3%) during the same time period. The fund’s annualised performance since inception is +12.0% p.a., while its YTD performance stands at +4.5%. The broad diversification of the fund’s portfolio has resulted in lower risk with an annualised volatility of 9.01%, a Sharpe ratio of 1.32, and a correlation of the fund versus the MSCI World Net Total Return USD Index of 0.33, all based on monthly observations since inception. This was a better month for the fund with a well-rounded performance led by Pakistan, where the fund’s consumer discretionary holdings did particularly well on the back of good quarterly results by the automobile and consumer appliance names that the fund holds. We continue to be positive on the consumer discretionary sector in Pakistan due to the underpenetrated consumer market in the country. Automobile sales continue to grow at double digits and the fund holds two passenger car companies, one motorcycle company, and one truck manufacturer, and additionally one consumer appliance company. The bigger event this month in Pakistan was the decision by the Supreme Court not to disqualify the Prime Minister over the Panama Papers issue. The market had been weak due to this uncertainty but rallied by ~2,800 points (+6.0%) between 19th April and 21st April with the decision being announced on 20th April. However, the issue has not died down yet as there will be a Joint Investigation Team probe into the matter, which is expected to be completed within 60 days. With the election expected in May 2018 we would not be surprised by further political noise, but the growth outlook for Pakistan remains positive on the back of a pick-up in economic activity with most industries going through a capacity expansion cycle and this is reflected in the loan growth numbers over the past few quarters with double digit loan growth for fixed capital investments. Further, the China Pakistan Economic Corridor “CPEC” continues to be executed and the expected increase in power capacity can help improve GDP growth rates to greater than 5-5.5%. Consumer discretionary demand remains strong on the back of low interest rates and an improving security situation. Though the Bangladeshi market corrected by 3% during the month over currency depreciation fears, the fund’s largest holding, the GDR of a Bangladeshi pharmaceutical company, was up by 20% during the month, thus helping the fund’s performance. Lower remittances and a slight current account deficit has led to currency depreciation of ~3% over the past two months. However, the macro situation in Bangladesh is still stable with foreign exchange reserves covering 9-10 months of imports. The Sri Lankan market rallied by 9% this month on the back of low valuations as well as possibly some frontier funds rebalancing from Pakistan to other frontier markets as Pakistan moves to emerging market status by the end of May 2017 (though AFC Asia Frontier Fund will continue to invest in Pakistan after its inclusion in the MSCI Emerging Market Index). The fund has increased its exposure to Sri Lanka over the past month as written in last month’s comment as we saw value in some of the names. Within Sri Lanka, a conglomerate, a consumer beverage company, and a tobacco company all helped with performance during the month. Mongolia continues to be a turnaround story and did well for the fund this month, with good gains from a cashmere producer and a coal producer. With the IMF’s backing, FDI picking up, coal exports increasing and currency appreciation, the macro situation in Mongolia seems to be turning around. Vietnam had a negative month as the heavily-weighted banking sector saw a slight correction. Nevertheless, the story continues to be positive, as this was backed by the latest FDI commitments of USD 10.95 billion so far this year, a growth of 40% YoY. The best performing indexes in the AAFF universe in April were Sri Lanka (+9.0%), Mongolia (+4.7%), and Pakistan (+2.4%). The poorest performing markets were Laos (-5.0%) and Cambodia (-4.3%). The top-performing portfolio stocks this month were a Mongolian fire equipment producer (+81.5%), a Pakistani car assembler (+39.4%), a Mongolian gold exploration company (+30.7%), and another Pakistani car assembler, which was up 28.4%. In April, we added to existing positions in Laos, Mongolia, Sri Lanka, and Vietnam and reduced our exposure in Mongolian, Pakistani, and Vietnamese holdings and completely exited two Vietnamese companies: a food producing company and a property developer. We newly added a Pakistani petroleum marketing company, a bank in Sri Lanka, a Sri Lankan household good producer, a Cambodian port, and two new holdings in Vietnam: a producer of plastic bags and a property developer. As of 30th April 2017, the portfolio was invested in 116 companies, 1 fund and held 5.4% in cash. The two biggest stock positions were a pharmaceutical company in Bangladesh (9.2%) and a Pakistani pharmaceutical company (3.5%). The countries with the largest asset allocation include Pakistan (26.1%), Vietnam (24.7%), and Bangladesh (17.8%). The sectors with the largest allocation of assets are consumer goods (29.6%) and healthcare (18.2%). The estimated weighted average trailing portfolio P/E ratio (only companies with profit) was 19.8x, the estimated weighted average P/B ratio was 3.26x, and the estimated portfolio dividend yield was 3.51%. For more information about Asia Frontier Capital’s Asia Frontier Fund please click the following links: AFC Iraq Fund - Manager Comment [MYON]

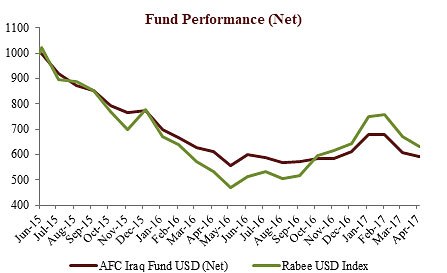

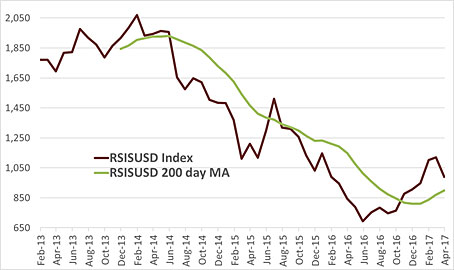

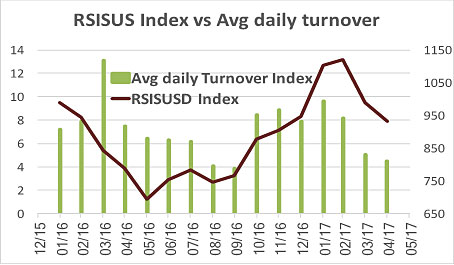

AFC Iraq Fund Class D shares returned −2.7% in April as the market continued the process of correction and profit-taking after the strong upside momentum that began in late summer of last year and ran into February. Rabee Securities’ RSISUSD Index (red), 200 day moving average (green) While at first glance the declines of the last two months look like they have reversed the spectacular gains seen early in the year, they should be viewed within the context of a market emerging from a severe multi-year decline of -68%, with the January move confirming the start of the bull market. The volatility of the monthly returns of the year so far are a function of constrained overall liquidity in the economy. Supporting this reasoning is that turnover expanded significantly during the market’s rise and contracted meaningfully during its decline with last month’s turnover at about half the January level and almost at the all-time lows seen in the summer, as the chart below demonstrates.

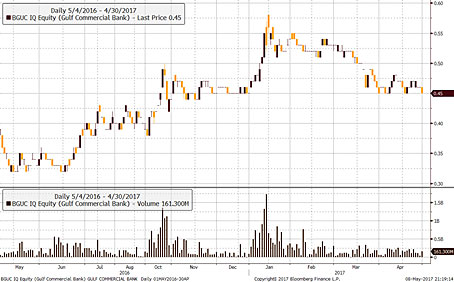

Focusing on percentage changes masks and overlooks the misleading effects of the phenomena of low stock prices, in which seemingly big percentage moves occur as a stock trades between the bid and offer. The price action of Gulf Commercial Bank (BGUC) illustrates this perfectly: with the bid-offer at IQD 0.44 to IQD 0.45, the stock moves about 2.3% either up or down as it trades on either offer or bid, and with the incredibly low volumes, a few small sell orders can send the stock down 3-4 ticks over a few days or down 6.9-9.2% which, at an index weighting of over 10.5%, would translate to about -0.7 to -0.9% decline in the index. With 8 banks accounting for 73% of the index by weight, and most trading at IQD 0.37 to IQD 0.98, it is easy to see that as prices drift lower on lower turnover, seemingly large yet misleading percentage changes can occur. The two charts below put the price action of BGUC in context. The short-term chart illustrates the fits and starts nature of the recovery, while the turnover picture highlights the observation of sideways action on low turnover, followed by price rises on high turnover, in which current price action is seen to mirror that during the summer of last year. The long-term chart puts the overall price action in the context of the multi-year decline from peak to bottom. From a technical analysis perspective, the price pattern from late 2015 to the current time could be seen as a classic inverse head and shoulders bottoming pattern. But it should be noted that technical analysis tends to be more valid in deep and liquid markets than in markets such as Iraq. Gulf Commercial Bank (BGUC)

Foreigners were net sellers for the month, with selling mostly concentrated in two names which were absorbed by local buying but, given the continued lack of overall liquidity, resulted in diverting liquidity from other names in the market with the effect that most other stocks drifted lower. Finally, both the market price of the Iraqi Dinar (IQD) vs the USD and the price of Iraq’s Eurobond were almost unchanged over the last few weeks with the Eurobond at 2 year highs which seem to be consistent with the bottoming process in the equity market. Last month it was argued that the decline of Iraq’s risk premium as expressed in the narrowing of the yield spread between Iraq’s Eurobond and the US 10-year bond was a sign of the rehabilitation of Iraq in the eyes of foreign investors. It seemed logical to conclude that this implied favourable interest in Iraq and that it would likely be followed by FDI and eventually by equity inflows. The rationale for equity inflows would be based on the arguments made in the outlook for 2017 but the trigger would likely be a gradual strong performance of the RSISUSD vs the MSCI World Index (see chart below). The relative performance line (orange line) since September puts the market’s absolute performance since then in perspective, i.e. a basing of relative performance that could translate into a relative out-performance of the MSCI World Index as the market begins to discount a sustainable post-conflict economic recovery. It’s reasonable to argue that inflows would start into the Iraqi equity market as this relative performance builds up and the risk-reward criteria shifts towards the reward aspect. RSISUD Index (brown), RSISUSD Index relative to MSCI World Index (green) Given the changed nature of the market from what we saw during the multi-year correction, it can be argued that it is primed for another multi-month up move as current conditions (prices drifting lower on lower turnover) are almost identical to those seen throughout the summer of last year. The timing, however, is unknown, as turnover is not expected to recover for the next few weeks with Ramadan starting in late May and ending in late June, to be followed by the Eid holidays. Nevertheless, the opportunity continues to be to acquire high-quality companies whose earnings power/assets/franchises held up well during the brutal economic decline of the last two years while the growth in their earnings/asset values is expected to outpace the economic recovery post-conflict. As the known risks of the last two years are still present, this recovery will continue to be in fits and starts. The liberation of the remaining districts in the western side of Mosul continues at the slow grinding pace of house-to-house fighting. Reports indicate that the days of ISIS there are numbered but that the group is intent on inflicting maximum civilian loss of life in the process. However, life in the liberated parts of Mosul is quickly returning to normal, driven by local businesses and residents keen to claim their lives back. Crucially, this is happening without much sectarian conflict or a new wave of terror atrocities as had been feared. As of 30th April 2017, the AFC Iraq Fund was invested in 14 names and held 1.8% in cash. The fund invests in both local and foreign listed companies that have the majority of their business activities in Iraq. The countries with the largest asset allocation were Iraq (98.0%), Norway (1.7%), and the UK (0.3%). The sectors with the largest allocation of assets were financials (57.3%) and consumer staples (21.2%). The estimated trailing median portfolio P/E ratio was 10.95x, the estimated trailing weighted average P/B ratio was 0.90x, and the estimated portfolio dividend yield was 2.87%. For more information about Asia Frontier Capital’s Iraq Fund, please click the following links: AFC Vietnam Fund - Manager Comment [MYON]

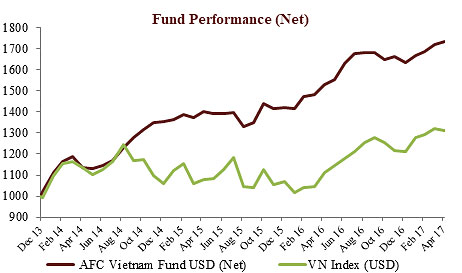

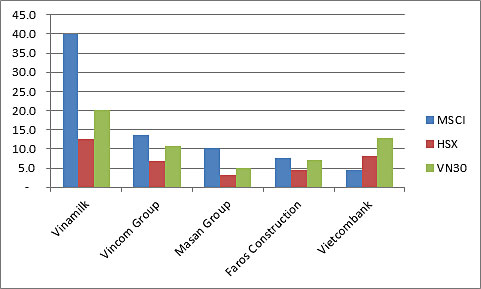

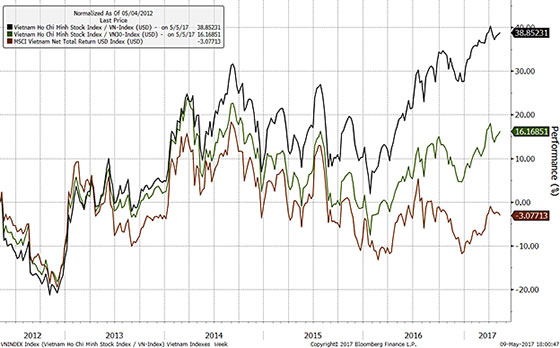

The AFC Vietnam Fund returned +1.0% in April with an NAV of USD 1,735.79, a new all-time high, bringing the net return since inception to +73.6%. This represents an annualised return of +17.9% p.a. The April performance of the Ho Chi Minh City VN Index in USD was −0.6% while the Hanoi VH Index lost −1.4% (in USD terms). Since inception, the AFC Vietnam Fund has outperformed the VN and VH Indices by +42.6% and +51.8% respectively (in USD terms). The broad diversification of the fund’s portfolio resulted in a low annualised volatility of 8.96%, a high Sharpe ratio of 1.97, and a low correlation of the fund versus the MSCI World Index USD of 0.30, all based on monthly observations since inception. The broader market was slightly lower in the first two weeks of April, awaiting first quarter 2017 company results, causing stocks to consolidate across the board with both indices declining slightly: HCMC dropped -0.6% and Hanoi went down by -1.4% in local currency terms. With most earnings announcements in the fund’s holdings already out, the NAV of the AFC Vietnam Fund increased by +1.0%. Market developments People who invest in Vietnam usually follow the so-called benchmark index HOSE (Ho Chi Minh City index), but we are always surprised about how many new and potential investors are considering buying ETFs in Vietnam. As we have tried to explain many times before, ETFs aren’t well-suited for Vietnam since they are unable to track the index and hence vastly underperform the market. This is mainly due to an already fully used foreign ownership quota in some of the blue chips, but also a result of the inability to add newly listed index stocks right from the listing day because they often trade “limit-up” for the first few days without any meaningful turnover. Some ETF investment managers are creating their own benchmarks which they are then able to track, but this of course doesn’t make sense if their benchmark isn’t reflecting the market. Other well respected companies, such as MSCI for example, are defining their Vietnam index in a more realistic manner, but given their extreme overweight in a few stocks, it wouldn’t be ideal to use this index as a benchmark. Vietnamese Indexes Weightings For those reasons, there are many different Vietnam indices which are trying to paint an accurate picture of the Vietnamese market, but given that their long-term performance is poorly correlated with the HOSE Index, it doesn’t make much sense to focus on them. 5-year performance: MSCI Vietnam – VN Index - VN30 Due to significant differences in the weightings of the largest blue chips in these various indices, the index performance is of course also widely different. We are therefore not attempting to track any of these indices and are instead focused on investing in stocks which we consider undervalued, while their market capitalisations play only a minor role. The only index which we moderately follow is the Hanoi Index (HNX) since more than 50% of our holdings are listed there. Unfortunately, this index is also flawed because of its high weighting of only a handful of stocks, and hence doesn’t provide a broad enough representative view of the market. For example, the strong performance of banking stocks earlier this year followed by a sharp correction in recent weeks was clearly visible in the overall performance of the index. 5 year Hanoi Index Nevertheless, from a technical point of view, there is a good chance that the broader market will finally break out on the upside of its long-lasting sideways movement. This view is supported by the already published earnings announcements for the first quarter of 2017. With over two thirds of the fund’s companies having reported their earnings, conviction in our stock selection process is higher than ever. We see many of our companies trading at 4-8 times earnings based on the first estimates for this year. The majority of our stocks are now trading on single digit earnings multiples which can be explained by the weakness of the market breadth over the past 12 months. Some of the fund’s holdings performed very well in the first 4 months of this year and hence we exited them partially or completely. These profits outweighed the weakness in some of our other holdings. Despite generating returns of over 70% since the launch of our fund, we are still very bullish with regards to the outlook of our stock portfolio since it is as attractively valued as it was in the early days, when we first started investing in Vietnam. With the recent announcement from Moody’s to lift Vietnam’s credit rating outlook to positive, the country is slowly appearing on the radar of more and more investors, something which has also had a positive impact on our assets under management, as we have experienced strong inflows in recent months. On a personal note, such positive news has led our CEO to increase his holdings in the AFC Vietnam Fund substantially during the month of April. Economy

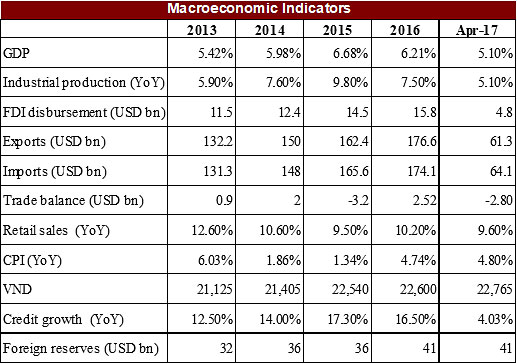

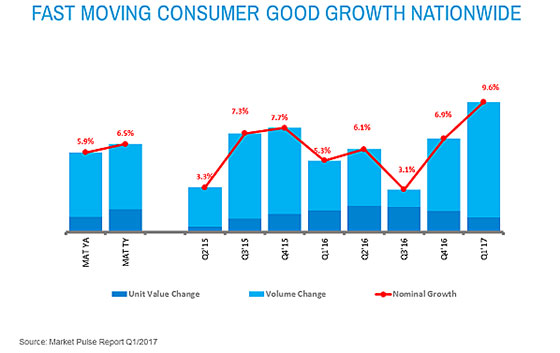

New and additional FDI reached USD 9.24 billion in the first 4 months of 2017. Indirect investment by foreigners also increased to USD 1.35 billion. In total, direct and indirect investment into Vietnam expanded by 40.5% compared to the same period last year, reaching USD 10.59 billion. South Korea continues to be the largest investor into Vietnam with USD 4.05 billion, accounting for 38.25% of total FDI, and the second largest is Japan with USD 1.85 billion. Total exports from Vietnam increased slightly to USD 61.7 billion in the first 4 month of this year. Meanwhile, total imports reached USD 63.8 billion. Other developments Fast moving consumer goods (FMCG) experienced record growth in the first quarter of 2017, and were up +9.6% versus +5.3% over the same period last year. This reflects the highest growth in the past three years, according to Nielsen’s Market Pulse Report. Robust FMCG consumption reflects Vietnam’s consumer optimism with its consumer confidence index currently ranking fifth in the world. The positive sentiment over Vietnam’s Lunar New Year helped to drive FMCG growth as consumers were willing to spend money. Rural areas have become a new source of growth for many manufacturers over the past few years and now account for 51% of total FMCG sales. Over 60% of Vietnam’s population live in rural areas and there are excellent opportunities for companies in this sector.

For more information about Asia Frontier Capital’s Vietnam Fund please click the following links: AFC Travel Report – CambodiaIn line with our process of being on the ground in the countries we invest in, Scott Osheroff, Analyst at Asia Frontier Capital, travelled to Cambodia to visit portfolio companies and other companies on our shortlist. The photos in this article are all by AFC. It took nine hours to reach Banlung, the provincial capital of Ratanakiri, from Cambodia’s capital, Phnom Penh. Banlung is tucked up into the northeast pocket of Cambodia in an area referred to by some as the Dragon’s Tail, an area which in some ways resembles the wild west. Recently built roads, courtesy of Chinese investment, have transformed a once pothole-ridden two-day journey into a smooth two-lane road which traverses the province to the Vietnamese border. The area, once lush with virgin forest has given way to heavy logging (which has only accelerated with improved infrastructure) and then rubber plantations, planted at the peak of the rubber market between 2010 and 2012 and which now struggle for survival. However, I was not here to sightsee, but rather to visit the country’s first foreign-owned mining operation, a small-scale gold deposit.

An underexplored country, Cambodia hosts several international quality resource assets including a 907,000oz gold deposit measuring ~2g/ton, which is owned by Australian-listed Emerald Resources and both onshore and offshore oil & gas reserves. I was on my way to visit a gold asset owned by India’s Mesco Steel had been recently acquired from Canadian-listed Angkor Gold. The morning after we arrived in Banlung, a modest town built on logging and gem trading which you could easily pass through without a second thought, we headed east towards the Vietnamese border. About forty-five minutes into our drive we flanked right, turning off the main road and into the jungle. Passing by an ethnic minority group village which has seen its quality of life markedly improve through CSR projects related to development of the gold asset, we kept on deeper into the jungle. For about one kilometre the area was beautifully lush as we bounced up and down along the potholed, hard-packed earthen road towards the mine site. Sadly, further on it was unfortunate to see the stark reality of Cambodian deforestation in full swing as the jungle had been clear cut, except for that on several knolls, while the entire area was being slashed and burned in preparation for planting cassava. It felt outer worldly. This is the unfortunate truth about many developing countries—lack of infrastructure keeps the environment intact, while primitive logging roads pave the way for real roads and eventual habitation. Passing through the newly planted cassava fields and traditional Khmer houses, we came upon the mine license boundary. Through the bush, I was shown where a storehouse for explosives was being built, and where electricity and other infrastructure was being planned. This was followed by a tour of the two mine shafts, one of which is a steep incline and the other vertical. A small mine with 30,000oz to 40,000oz respectively, it is believed the mine is open at depth which will likely allow it to operate past its expected seven to eight-year life span.

Having arrived at the mine site around noon, the outside temperature was well above 40 degrees Celsius. Therefore, after an hour touring the property it was time to retreat back to the air-conditioning in the car. Having left the mine site and back on the main road to town, I was told by my driver that we were to make a detour before heading to town. Not long after we turned off the main road and onto a country road passing through a local village which clearly didn’t have much exposure to the outside world. Not far past the village we came to a crawl as my driver was trying to find a road camouflaged by head high grasses. Once identified, we turned into the field cutting a new path. Once through the grass we had arrived on a privately owned rubber plantation which I was told measured ~1,000ha. Row after row, the plantation was tranquil and cool under the thick canopy of rubber trees. Deep into the plantation we came to a stop and put the car in park. As we got out a large group of people approached us. In ragged clothes with hands in front of them I thought maybe the zombie apocalypse was real. However, as they got closer it became apparent their hands were full of lush gems. We had driven into a small-scale gem mining operation. Two foreigners must have seemed like easy targets for a sale as we were handed gem after gem to be inspected. After buying a few for souvenirs, a group of what looked like moles came walking towards us. Covered in a thick layer of dirt from head to toe these were the miners who had come out of their holes to also attempt a sale. It was a surreal experience.

After having enough of stones being shown to us, we walked around to explore the mine site. It is important to note that you had to walk carefully, for on the other side of every mound of dirt was a shaft, some of which go to depths of thirty meters. I did not want to trip! It was remarkable to see such a primitive operation in the middle of a rubber plantation providing employment for several dozen people. On the drive back to Banlung, I better understood why there were so many gem shops in the centre of town. The following day we concluded our trip with a 7 hour drive to Siem Reap, home of Angkor Wat. The trip was gruelling due to the heat and the distance, though the newly constructed Chinese highway was pleasantly smooth. We passed over several gorgeous rivers whose bridges we stopped on to take photos as there wasn’t much in the way of traffic. We also passed by an ominously large structure which we had thought was a Chinese financed power plant. However, on its back side stood what we learned was 10,000 hectares of sugarcane to feed what, upon completion, would be the largest sugar mill in Cambodia.

In the late afternoon, with our petrol tank light flashing red, we limped into Siem Reap. Enjoying some fresh Siem Reap sweet sausages and a cold Angkor beer was the appropriate way to end the day. The following morning, before flying back to Phnom Penh, I decided to revisit the Angkor Wat complex, which frankly you cannot visit enough. With so many temples spread throughout the complex the atmosphere is second to none.

I hope you have enjoyed reading this newsletter. If you would like any further information, please get in touch with me or my colleagues. |

||||

|

With kind regards, Thomas Hugger |

|||||

|

Asia Frontier Capital Limited |

|||||

Disclaimer:This Newsletter is not intended as an offer or solicitation with respect to the purchase or sale of any security. No such offer or solicitation will be made prior to the delivery of the Offering Documents. Before making an investment decision, potential investors should review the Offering Documents and inform themselves as to the legal requirements and tax consequences within the countries of their citizenship, residence, domicile and place of business with respect to the acquisition, holding or disposal of shares, and any foreign exchange restrictions that may be relevant thereto. This newsletter is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law and regulation, and is intended solely for the use of the person to whom it is intended. The information and opinions contained in this Newsletter have been compiled from or arrived at in good faith from sources deemed reliable. Opinions expressed are current as of the date appearing in this Newsletter only. Neither Asia Frontier Capital Ltd (AFCL), nor any of its subsidiaries or affiliates will make any representation or warranty to the accuracy or completeness of the information contained herein. Certain information contained herein constitutes “forward-looking statements”, which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of Funds managed by AFCL or its subsidiaries and affiliates may differ materially from those reflected or contemplated in such forward-looking statements. Past performance is not necessarily indicative of future results. © Asia Frontier Capital Ltd. All rights reserved. The representative of the funds in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative. AFC Asia Frontier Fund is registered for sale to qualified /professional investors in Japan, Singapore, Switzerland, the United Kingdom and the United States. AFC Iraq Fund in Singapore, Switzerland, the United Kingdom and the United States. AFC Vietnam Fund in Japan, Singapore, Switzerland and the United Kingdom. By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their relevant jurisdictions. |

|||||

GO TOP |

|||||